Rand set for a comeback

The rand is set to strengthen against the dollar throughout the rest of 2025 as investors look to diversify their holdings outside of the United States amid its fiscal fragility and extreme valuations.

Emerging markets are also well-poised to benefit from elevated commodity prices, particularly gold exporters, as ongoing geopolitical uncertainty drives demand for relative safe havens.

Old Mutual Investment Group chief investment officer Siboniso Nxumalo outlined what the asset manager is watching in 2025 at its Q1 investment update.

Nxumalo explained that investors have been closely watching the US market as they look for cues on what the fallout of Trump’s trade policy may be.

Eyes are also on the United States due to its outsized influence on financial markets as the holder of the world’s reserve currency and it having the world’s deepest capital markets.

However, for the first time in over a decade, investors may have to contend with a temporary pause in US exceptionalism, with returns being driven by other equity markets.

Nxumalo explained that lofty valuations of United States-based companies have been a major problem for investors since March 2024, with companies being saddled with extremely high expectations for earnings growth.

He said that high expectations often come with disappointment, with large United States companies already beginning to underperform their elevated expectations as growth slows.

These high expectations have come on the back of a decade of United States exceptionalism, with its equity markets outperforming the rest by a significant margin.

“The US equity market being around an all-time high in terms of valuation implies that the US dollar has been strong as any excess liquidity has flowed into US-based assets,” Nxumalo explained.

As money flows into United States assets, demand for the dollar rises, and so does its value compared to other currencies.

In particular, emerging market currencies are hard hit as investors would rather invest in assets in the United States that generate better risk-adjusted returns.

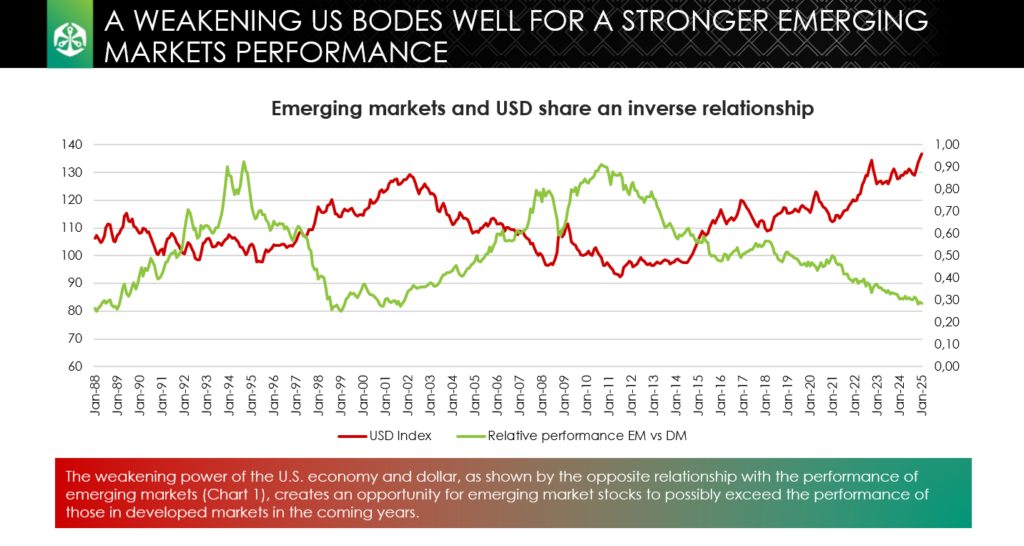

“You have got to pay attention when you look at global returns to the fact that over the last 15 years, not only has the US stock market beaten everything, but the US dollar has also beaten every other currency,” Nxumalo said.

“At the same time, every other currency, particularly emerging market currencies, have underperformed versus the dollar, and emerging market stocks have underperformed.”

This can be seen in the graph below, which shows the US dollar index strengthening versus emerging market currencies over the past decade.

Dollar pullback on the cards

Nxumalo said the trend is likely to shift significantly in 2025 as the gap between the US dollar index and emerging market currencies is far wider than its historical average.

This implies that the dollar has overextended and will eventually pull back, with emerging market currencies strengthening against the greenback.

Nxumalo was clear that this does not mean the script would completely flip – it just means that the gap between the dollar and emerging market currencies should narrow to its historic average.

“At this level, the US dollar feels a bit too high, which means that every other currency in the world feels a little too cheap,” Nxumalo said.

This shift could be accelerated by investors pumping money into emerging market assets as they are attractively priced.

In contrast, US assets are trading at a near all-time high, with Donald Trump ascending to the White House with the second-highest ever price-to-sales ratio in the S&P 500 of any presidential term.

“This really concerns us. Whoever starts in the market at these levels generally ends up disappointing investors as assets are priced for perfection,” Nxumalo said.

The only other two times a US President began their term in office with such a high price-to-sales ratio, the market provided negative overall returns for their four-year term.

Nxumalo explained that these lofty valuations, combined with geopolitical uncertainty, elevated inflation, and fiscal fragility in the US, are likely to disappoint investors.

Adding to the concern is that the returns of the US equity market have been driven by a handful of companies, the Magnificent 7 – Apple, Microsoft, Google, Amazon, Meta, Nvidia, and Tesla.

The relative outperformance of these companies has created the most concentrated stock market in US history, with the top 10 stocks making up nearly 39% of the entire S&P 500.

These companies are beginning to underperform their lofty valuations, with their year-on-year growth slowing throughout 2024.

As a result, the US equity market has had a poor start to 2025, underperforming many of its peers as investors look elsewhere for returns.

Comments