South Africa going from junk to darling

South Africa is on the path to regaining its status as an investment-grade country, with the National Treasury imposing fiscal discipline and economic growth that is expected to pick up.

However, there are significant risks to this, and it will take years of continued improvement for South Africa to emerge from junk status.

Nedbank economist Isaac Matshego outlined what it would take for the country to get rating agencies to shift their outlook on South Africa while previewing the Medium-Term Budget Policy Statement (MTBPS) next week.

Matshego said this MTBPS is the first in a long time to take place amid an improving macroeconomic outlook for South Africa.

Load-shedding has seemingly ended, with the country not experiencing any power cuts for over six months.

Investors have been widely optimistic about the formation of the Government of National Unity (GNU), and the National Treasury’s fiscal discipline appears to be paying off.

However, just as it took nearly a decade of mismanagement of the government’s finances to get South Africa downgraded to ‘junk’ status, it will take many years for the country to reach investment grade again.

Matshego outlined some of the reasons why South Africa’s credit ratings steadily declined in the 2010s to give an idea of the scale of the problem.

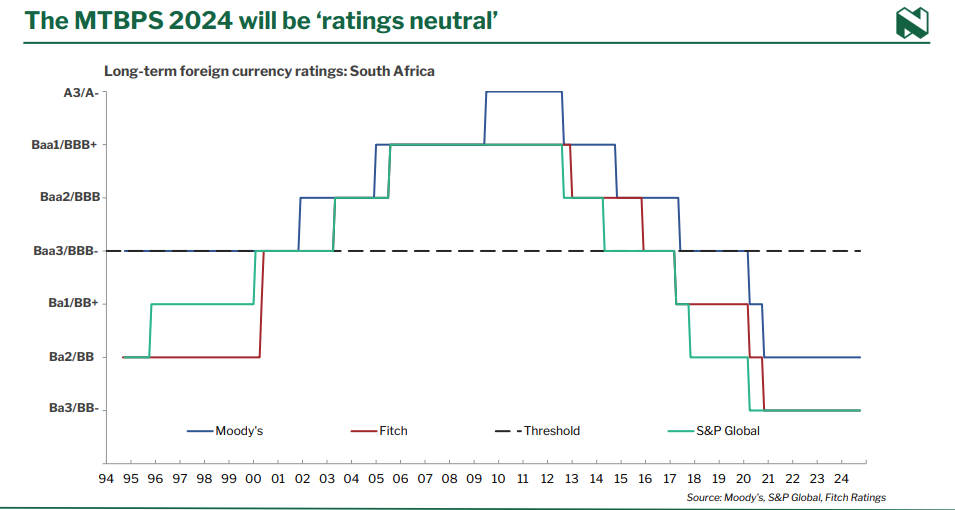

South Africa’s credit ratings have undergone a decades-long slide from international sweetheart in the mid-2000s to junk status in 2016.

He explained that the main problem is a lack of economic growth. South Africa’s economy has largely stagnated in the past decade, growing at less than 1% annually.

At the same time, government spending spiked sharply in response to the Great Financial Crisis (GFC in 2008/09) and then due to financial mismanagement.

Crucially, increased government spending during this period did not improve economic output, with much of it going towards consumption.

Without a corresponding rise in GDP, the government’s debt-to-GDP ratio surged and global rating agencies began to take notice in the mid-2010s.

The emergence of widespread corruption, termed state capture, added to South Africa’s woes, with key institutions gutted and mismanaged.

As a result, S&P Ratings began reviewing South Africa’s credit ratings and changed its outlook to negative in 2012. This kicked off a steady decline into junk status, which South Africa entered in 2016.

The initial rise in South Africa’s credit rating under the Mandela and Mbeki administrations, followed by its decline in the last decade, is shown in the graph below. The second graph shows the steady rise in government debt.

Entering junk status, below investment grade, severely impacted the South African economy and effectively halted foreign investment in local assets.

Matshego explained that since entering junk status, foreign ownership of local government bonds as a share of the total has declined from 44% to around 25%.

This has forced local institutions to pick up the slack, increasing the risk of contagion in the financial sector as all companies are exposed to a common risk – government debt.

However, South Africa is on the right path to getting out of junk status, but it will take many years for the country to fully recover.

National Treasury’s fiscal discipline, along with key reforms in network industries such as electricity, logistics, and water, is set to greatly improve South Africa’s attractiveness as an investment destination.

However, it is vital that increased optimism and healthier state finances translate into better growth outcomes, as that can kick off a virtuous cycle.

As growth picks up, all other things being equal, the government’s debt-to-GDP ratio should decline. Furthermore, tax revenue should pick up and enable the state to pay down its debt.

This will reduce its debt-servicing costs, freeing up additional capital to invest in growing the economy or paying down its debt further.

Matshego said South Africa is on track to kickstart this virtuous cycle, with Nedbank forecasting the government’s deficit should continue to narrow towards 3% in 2027/28.

Importantly, the government should continue to run a primary budget surplus, which means that its income from tax revenue can cover its expenses, excluding debt-servicing costs.

This will slow down the rate of growth of its debt burden and enable it to begin paying down its debt.

If this trajectory continues and growth outcomes improve, Matshego said it is entirely possible rating agencies shift their outlook for South African from neutral to positive in May or November 2025.

This is the beginning of the journey out of junk status. Provided the trajectory remains positive, the agencies will likely move South Africa a notch closer to investment grade in 2026.

Comments