Three interest rate hikes on the cards for South Africa

The South African Reserve Bank (SARB) is expected to keep interest rates elevated in response to price pressures resulting from the Middle East war.

While forward-rate agreements initially priced in two interest rate cuts by early 2027, they now forecast three hikes over the same period.

Momentum Investments economists Sanisha Packirisamy and Tshiamo Masike believe this would be too aggressive and would severely impact South Africa’s economic growth.

Even prior to the outbreak of the US/Israel war against Iran, the SARB had been cautious, even in its cutting cycle.

Following a lengthy hiking cycle, which saw interest rates reach a 15-year high, the Reserve Bank’s Monetary Policy Committee (MPC) started cutting interest rates in September 2024.

Since then, it has cut rates six times, leading to a cumulative 150 basis points worth of cuts and bringing the repo rate down to 6.75% and the prime lending rate to 10.25%.

While providing significant relief to consumers, this is still far less than the 475 basis points of hikes seen in the preceding cycle.

At its January 2026 meeting, the MPC maintained its cautious, restrictive approach to monetary policy, keeping interest rates unchanged.

This decision came amid concerns about higher-than-preferred services inflation and caution over rising food inflation due to the foot-and-mouth disease outbreak.

Therefore, Packirisamy and Masike explained that the SARB had already been telegraphing a cautious interest rate cutting cycle before its March meeting and the outbreak of the Middle East war.

However, they said the petrol-pump pinch resulting from the conflict has now effectively moved the goalposts.

South Africa now faces potentially severe inflationary pressures for the next few months due to the US/Israel-Iran war, with interest rates expected to react in kind.

Packirisamy and Masike explained that this is largely due to the fact that South Africa is a price-taker in the global oil market, with higher oil prices now set to filter through the local economy, affecting far more than just fuel prices.

The charts below, courtesy of Momentum Investments, show the sources of South Africa’s fuel imports.

From fuel to food

Packirisamy and Masike said South Africa is heavily reliant on fuel imports, as its domestic refining capacity has been severely diminished over the past decade.

Currently, only around a quarter of South Africa’s crude oil imports originate directly from the Persian Gulf, with a majority coming from other African nations like Nigeria, Angola and Ghana.

Therefore, one may think that the effective closure of the Strait of Hormuz due to the Middle East war would not impact South Africa’s oil prices and supply as much.

However, the economists explained that the country has become increasingly reliant on diesel and petrol shipped from Gulf refining hubs, particularly following the shutdown of several domestic refineries.

“As a result, any disruption to shipping through the Strait of Hormuz could still have meaningful knock-on effects for fuel availability and prices in South Africa,” they said.

“As a price-taker in the global oil market, the upward pressure on local fuel prices acts as a significant drag on consumer confidence and raises local transport costs.”

Now, the risk is that the energy-led inflation spike, due to higher oil and fuel prices, becomes broad-based.

This essentially means energy prices will filter into food prices and transport costs, which will hit the lower-income deciles in South Africa the hardest.

“While fuel only accounts for 3.8% of the consumer inflation basket, food contributes 16.8%,” Packirisamy and Masike said.

“With the Agricultural Business Chamber estimating that 80% of maize is moved by road transport, higher fuel prices bode ill for food inflation in the near term.”

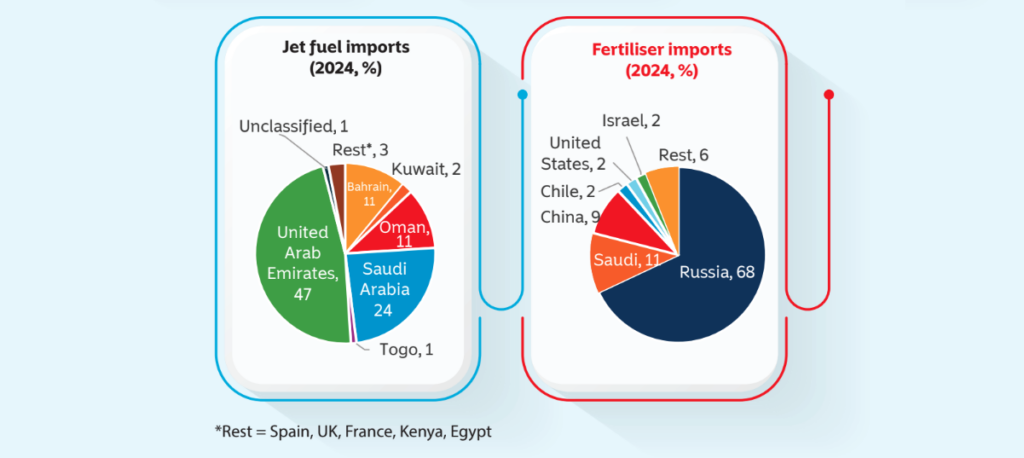

In addition, they pointed out that 80% of South Africa’s fertiliser is imported, providing further pressure on food inflation, as farmers can only absorb higher costs for so long, or may need to adjust how much they plant.

The charts below, courtesy of Momentum Investments, show the sources of South Africa’s jet fuel and fertiliser imports.

Interest rate response

Faced with these inflationary pressures, Packirisamy and Masike said the SARB is likely to keep interest rates elevated to protect its new inflation target from geopolitically driven price pressures.

“Forward-rate agreements have moved from pricing in two interest rate cuts by early 2027, to forecasting three hikes in the same period,” they said.

However, they said this could be too aggressive of a response, given the likely negative impact such high interest rates would have on growth.

At the MPC’s March 2026 meeting, SARB Governor Lesetja Kganyago said the ongoing Middle East conflict is a clear instance of a supply shock, which raises prices while weakening demand.

“The standard response to a supply shock is to look through first-round effects, which are unavoidable and cannot be stopped by interest rate changes,” he said.

“At the same time, central banks should be alert to second-round effects, where an initial shock triggers broad price increases.”

He explained that getting policy “right” means ensuring that the price response to supply shocks is transitory, and not persistent.

“It is always difficult to assess second-round effects in time. Waiting for clear evidence risks leaving the policy response too late,” he said.

“We therefore rely on forecasts, as well as indicators like wages and inflation expectations, to judge if there is a broader build-up of inflation pressure.”

“In previous meetings, we warned of elevated risks, and we have been proceeding cautiously in our rate setting. Now a crisis has hit, this prudent approach is proving appropriate.”

Kganyago explained that, until recently, conditions were favourable for the SARB to achieve its new 3% inflation target, and it appeared that South Africa would reach the target quickly.

“Now, there has been a negative shock, and it could take a bit longer. Nonetheless, all our forecasts show inflation reverting to 3% during the next two years,” he said.

“We are committed to delivering that outcome, and stand ready to act as needed to fulfil our mandate.”

Comments