Rand on a slippery slope as it hits R17 to the US dollar

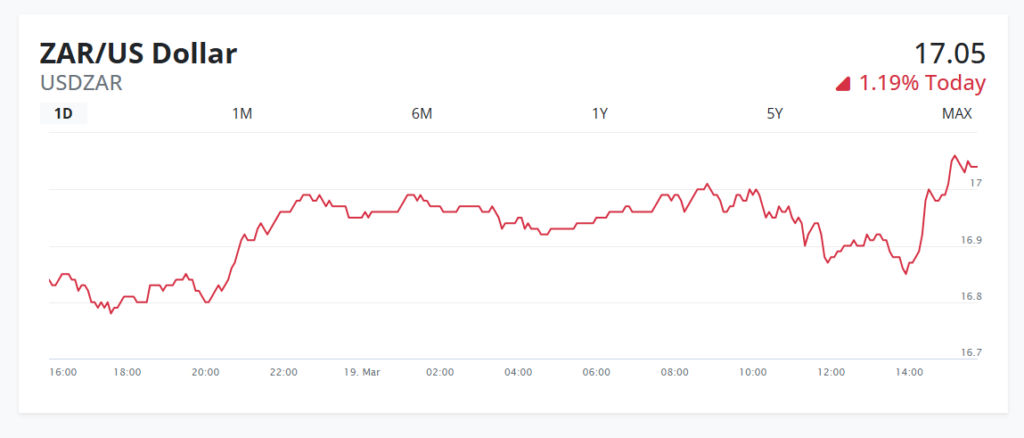

The South African rand has weakened above R17 to the US dollar for the first time since 9 December 2025, as the currency continues to be impacted by the ongoing conflict in the Middle East.

US-Israeli strikes on Iran and the country’s response by attacking nations across the Middle East have sent shockwaves through financial markets.

In the main, investors have rushed towards traditional safe-haven assets such denominated in US dollars and Swiss francs.

Money managers have abandoned emerging market assets, which are typically seen as more vulnerable to global shocks and more volatile.

The rand is particularly vulnerable in these scenarios as, given South Africa’s relatively deep capital markets for an emerging economy, it is traded as a proxy for sentiment to emerging markets more broadly.

It is also weakened by the fact that South Africa is an oil importer and will suffer the consequences of surging oil prices without benefiting.

Other economies that are major oil producers, such as the United States and some emerging markets, including Nigeria and Angola, will benefit from soaring prices.

Rising oil prices will see these countries rake in billions of dollars more in export earnings, boosting their local economies and state finances. As a result, their currencies will benefit.

The rand has weakened against a basket of emerging market currencies as well, reversing a years-long trend that pointed to South Africa’s rising relative attractiveness to investors.

In contrast, the minerals and metals in South Africa’s basket of commodities have seen their prices fall amid fears of a global economic slowdown, weakening the currency further.

As a result, the rand has trended weaker towards R17 to the US dollar from R15.74 at the end of January. On 27 February, the day before the first US-Israeli strikes on Iran, the rand was trading at R15.94 to the greenback.

On 19 March, the rand weakened to above R17 to the US dollar on reports that Israel targeted Iran’s lucrative South Pars gas field, the largest facility of its kind in the world.

Iran retaliated with strikes on energy infrastructure around the region, including Qatar’s main gas facility, sending oil and gas prices soaring. Gas futures in Europe jumped by 20% on the news.

This indicates that the war is only intensifying, with its impact on oil and gas infrastructure only becoming increasingly severe.

Damage of the kind from strikes on energy infrastructure indicates that the shock oil and gas markets will be prolonged, even if the war ends.

Some experts have estimated that, before the strike on its main facility, Qatar could take up to two weeks to restart liquefied natural gas production.

This has serious implications for South Africa as an oil importer, with it set to translate into record petrol and diesel price increases.

“This is going to be a huge shock to South Africa’s household and business sectors in April, and there is not a lot we can do about it,” Lings said.

The government does not have the ability to limit the impact on consumers, as the country does not have much of a strategic oil reserve, and it does not have the financial capacity to provide a subsidy or reverse tax hikes.

With interest rate changes, timing is key once again, with the resolution of the conflict in the near term potentially reversing these projected increases.

“A lot of this depends hugely on how long the conflict lasts. It does not look to us as though there is a huge amount of discussion regarding how this ends,” Lings said.

Comments