The US dollar going from hero to zero

The US dollar’s extended bull run since the end of the Global Financial Crisis appears to be coming to an end, as slower economic growth, elevated fiscal deficits and extreme policy uncertainty weigh on investor sentiment towards American assets.

This should translate into stronger emerging market currencies and faster growth in developing economies, including South Africa.

While this era appears to be coming to an end, it does not mean the US dollar will lose its privileged status, as it is likely to remain the dominant global currency.

Investec Investment Management portfolio manager Paul McKeaveney recently explained the shift rippling through global markets and how investors can adapt in a recent research note.

The US dollar has been the world’s primary reserve currency for decades and is still the most-used currency in financial transactions and flows across borders by some distance.

It makes up over half of the global foreign exchange reserves, with other currencies and assets such as gold making up the rest.

However, this share has steadily fallen over the years, with recent weakness in the dollar and developments in the United States leading some to argue the world should reduce its reliance on the greenback, McKeaveney said.

These concerns could mark the end of an 18-year bull run for the dollar, with the currency typically moving in long, mult-year cycles of strength and weakness.

Most notably, the dollar has been in a prolonged bull market since 2007, one of the longest on record, as American assets soaked up global liquidity.

McKeaveney said there are various signs that this cycle could be turning, including –

- A deteriorating US growth outlook: There have recently been downward revisions to US GDP forecasts and emerging signs of a slowdown.

- Fiscal and debt concerns: The US fiscal outlook has worsened, and high government deficits and rising interest costs are undermining confidence in the dollar. Of greatest concern is perhaps the recently passed One Big Beautiful Bill Act, which is set to increase the US debt-to-GDP ratio to about 107% by 2027.

- Policy unpredictability: Uncertainty in US policy and geopolitical moves can erode trust. Policies such as inconsistent tax, tariff or regulatory changes make the US a relatively less attractive place to invest at the margin, leading investors to explore other currencies.

- A changing world order: We are seeing a shift to a multipolar world, in which countries like China look to challenge US hegemony in many spheres, including payment systems and the use of the dollar as the world’s reserve currency.

These factors have led some investors and most notably central banks to consider alternatives to the dollar, including other currencies, but most significantly gold.

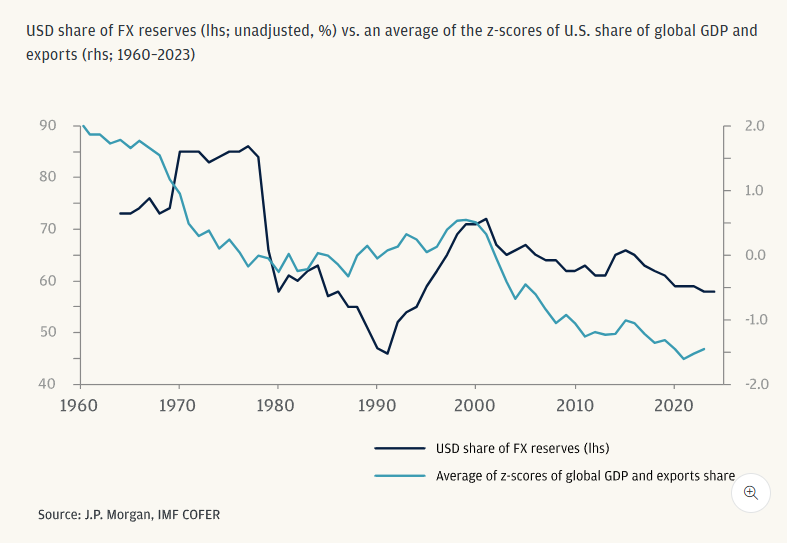

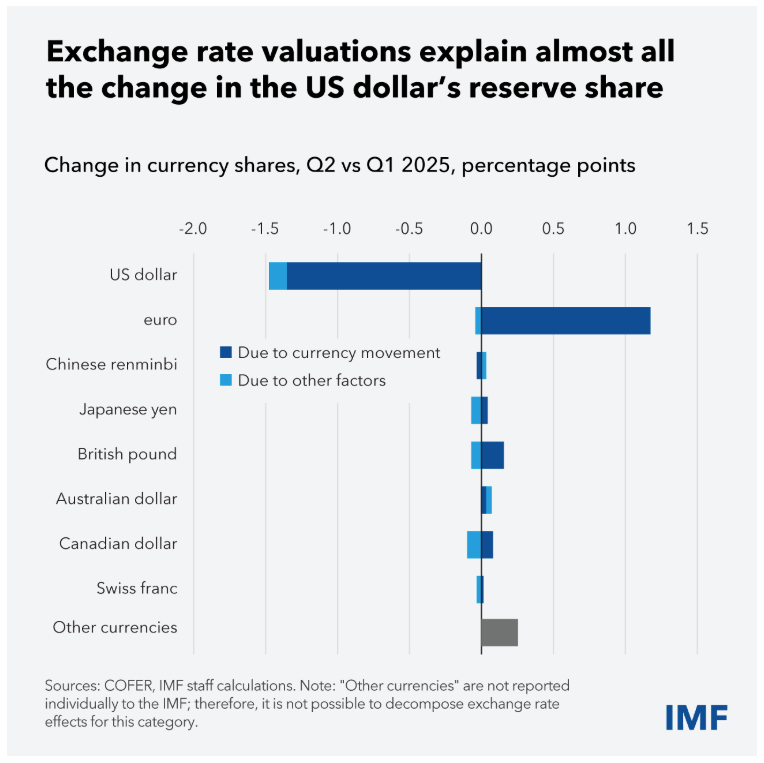

The steady decline in the US dollar’s share of global forex reserves in the graph below from JP Morgan, followed by the dollar’s more recent decline in the second quarter of 2025, according to International Monetary Fund data.

These graphs exclude the most significant beneficiary of this shift – gold prices.

Dollar is overvalued

The case for the end of the dollar’s era of inexorable strength is boosted by the fact that it is widely considered to be overvalued.

McKeaveney explained that valuation is key when assessing a currency, with the dollar being about 17% above fair value when compared to its long-term purchasing power parity (PPP).

This level of overvaluation has rarely been sustained for a long period of time, indicating that something has to give, and it is likely to be dollar weakness.

Indeed, every time in the past 50 years that the dollar has been this far above its PPP trend, it has eventually moved back into line.

Historically, when the dollar has been about 20% overvalued, it has tended to underperform by about 4% per year on average over the subsequent decade.

This historical valuation precedent thus supports the argument that the dollar’s recent peak will be followed by a secular weakening.

However, while it may seem prudent not to be over-exposed to the US dollar from now on, it’s important to note that timing such moves can be tricky, and a more responsible approach may be to diversify gradually, especially when the dollar is an investor’s base currency.

The decline of the dollar is unlikely to occur in a straight line, with rallies to be expected and problems with other currencies to limit its weakness.

For countries and investors, holding a diversified basket of currencies, or assets like gold, is a way to mitigate the risks of a declining dollar.

An added benefit is that when the dollar weakens, assets outside the US like other currencies, commodities, and non-US equities often perform well, so diversification can help to capture those gains.

For example, a softer dollar typically boosts commodity-producing emerging markets like South Africa.

De-dollarisation is already visible in the way central banks and investors allocate assets. Central banks worldwide have gradually rebalanced their reserve portfolios away from US dollars in recent years.

About 25 years ago, the US dollar accounted for approximately 70% of central bank reserves; today, it’s roughly 50% on average.

The euro has risen to about 20%, and many central banks have boosted their gold holdings to roughly 15% of reserves. Other currencies like the Japanese yen and British pound each make up around 5%.

Comments