State-owned enterprises like Eskom and Transnet have crushed South Africa’s economy

The lack of investment in infrastructure by South Africa’s public corporations has significantly limited economic growth over the past decade.

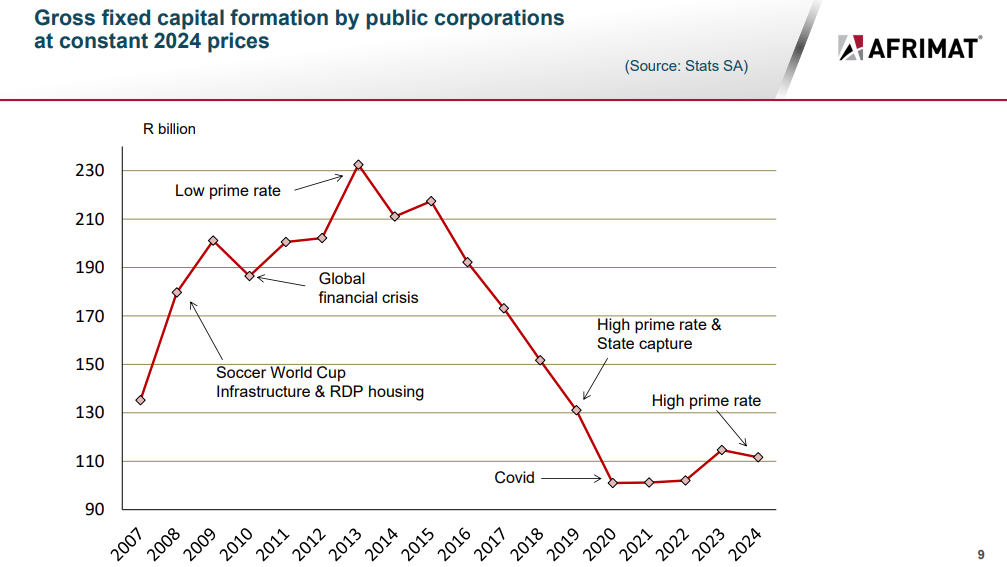

Gross fixed capital formation, a metric used to track investment in fixed assets such as infrastructure from public corporations, is less than half of what it was just a decade ago.

These companies, including giants such as Eskom and Transnet, allocated only R110 billion to fixed capital formation in 2024, compared to a peak of R230 billion in 2013.

This is one of the main reasons why South Africa’s infrastructure, from electricity to logistics, has deteriorated over the past decade.

As a result, the country has experienced periods of intense power cuts, water outages, and logistics bottlenecks over the past few years.

The deterioration of this infrastructure has led the Reserve Bank to list it as one of the major risks to the local financial system.

It has become a concern that the decay of South Africa’s state-owned enterprises (SOEs) may result in them or industries heavily reliant on them becoming unable to repay their debts.

Critical infrastructure failure also increases the operational costs of financial institutions by requiring additional redundancy services and contingency plans.

The bank pointed to the decline in Transnet’s rail tonnage over the past few years as an example, with the utility transporting only 150 million tonnes last year, compared to 226 million in 2017.

Its ports have also become synonymous with inefficiency, routinely ranking among the worst in the world according to the World Bank.

On the other hand, Eskom has made substantial progress in turning around its operational performance, with load-shedding declining significantly in 2024 and so far in 2025.

However, electricity supply in South Africa remains constrained and on edge due to a lack of historical investment in maintenance and new capacity.

This effectively limits economic growth, with any meaningful uptick in economic activity likely to result in power cuts due to increased demand.

All of this is essentially a result of inadequate historical maintenance, the development of new capacity, and the upgrading of equipment.

The capital expenditure of public corporations over the past decade has steadily shifted away from maintenance and constructing new infrastructure towards consumption and staff salaries.

This can be seen in the graph below, which shows the rise and fall of gross fixed capital formation by public corporations since 2007, courtesy of the Afrimat Construction Index.

South Africa is falling behind

The lacklustre gross fixed capital formation from public corporations is a major driver of South Africa’s poor economic growth.

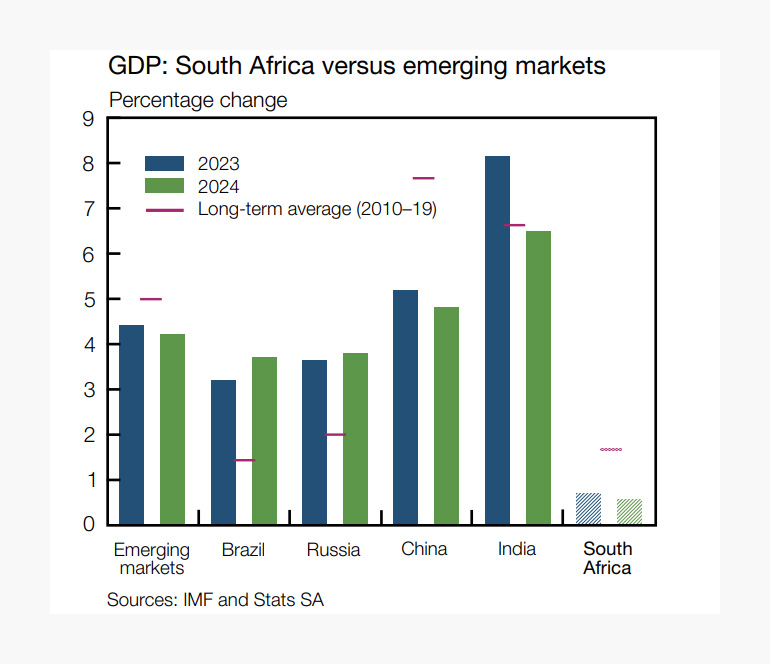

A common characteristic of fast-growing emerging markets is a high level of gross fixed capital formation, from both the public and private sectors.

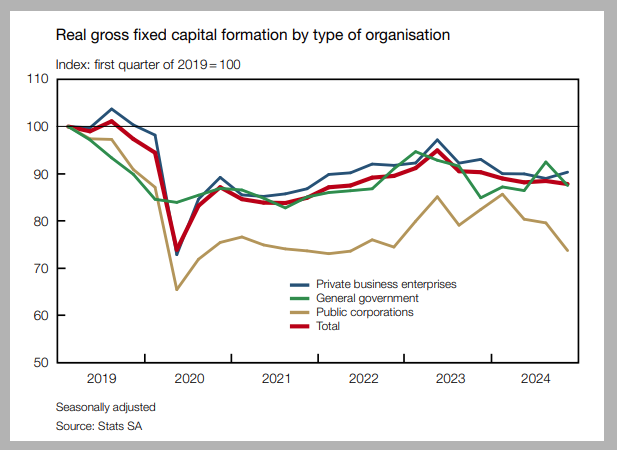

South Africa’s real gross fixed capital formation remains poor, with all components being below their 2019 levels.

This is largely due to businesses being hesitant to invest heavily in a stagnant economy, and the government coming under financial pressure, which limits its ability to invest.

Gross fixed capital formation is crucial for economic growth, as it is highly productive, adding to economic activity and tends to be sustained over a long-term horizon, meaning it remains within the country.

Other types of investment, such as portfolio investments in equities and bonds, are often termed ‘hot money’ because they can be withdrawn at the touch of a button.

However, fixed investment has steadily declined in South Africa, with the capital deployed by businesses and the government failing to recover post-pandemic.

This should improve in the coming years, partly because it is coming off a low base and also because of Eskom’s significantly improved performance.

Ongoing port and rail reforms, along with Eskom’s maintenance and transmission system development, should gradually ease supply bottlenecks and spur investment.

After contracting by 3.7% in 2024, investment growth is expected to rebound to 2.1% this year and rise to 3.6% by the end of the forecast period, underpinned by both the public and private sectors.

However, this will not be enough to drive meaningful economic growth in South Africa, with the International Monetary Fund (IMF) expecting the gap between it and other emerging markets to widen in the future.

South Africa’s poor gross fixed capital formation is evident in the graph below, with the following chart illustrating the country’s dismal performance compared to other emerging markets.

Comments