The R1.5 trillion goldmine that will save South Africa

South Africa’s economy continues to be hampered by a lack of fixed capital formation, which is vital for sustained growth.

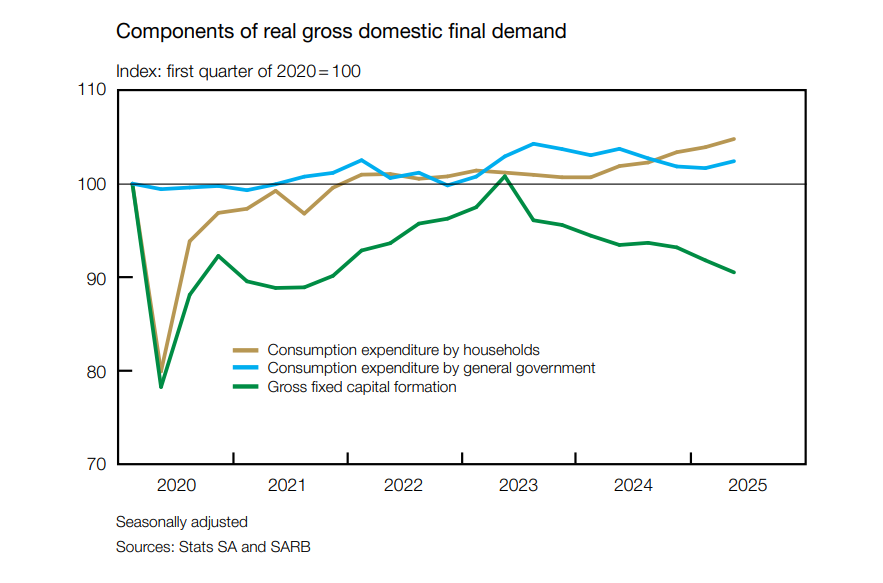

Currently, the uptick in household spending is too narrow and fragile to drive an economic recovery, with much of it based on temporary factors such as low inflation and early withdrawals from retirement savings.

The good news is that South Africa has the capital sitting on private sector balance sheets to drive much faster economic growth. Corporates currently have around R1.5 trillion sitting in cash.

The difficulty lies in creating an environment where companies are willing to take cash out of money market funds or call accounts and invest it in growing their operations.

Real gross fixed capital formation decreased further by 1.4% in the second quarter of 2025, following a decrease of 1.5% in the first quarter, the Reserve Bank revealed in its latest Quarterly Bulletin.

Fixed capital formation refers to spending by businesses on tangible assets that are expected to remain in use for a relatively long period, typically in the form of land, machinery, and buildings, to drive growth in their operations.

The decrease in fixed investment stemmed from reduced capital spending by general government and public corporations, which outweighed the increased investment by private business enterprises.

As a result, the level of real gross fixed capital spending in the first half of 2025 was 3.1% lower than in the corresponding period of 2024.

Real fixed investment by private business enterprises expanded by 5.6% in the second quarter of 2025 and contributed 3.9 percentage points to the overall growth in total real gross fixed capital formation.

The increase was led by higher investment in machinery and other equipment, as well as construction works, which outweighed the reduced spending on transport equipment.

Consequently, the private sector’s share of total nominal gross fixed capital formation edged up to 73.7% in the second quarter of 2025 from 69.5% in the first quarter.

Real gross fixed capital outlays by the public sector decreased by 16.7% in the second quarter of 2025, following an increase of 10.9% in the first quarter.

The contraction stemmed from reduced capital investment by both public corporations and the general government.

There was a significant reduction of 33.5% in capital spending by public corporations, reversing the robust 27.2% growth recorded in the first quarter.

The decline was largely attributable to reduced investment in non-residential buildings, transport equipment and computer equipment.

As a result, as a share of GDP, South Africa’s fixed capital formation remains roughly half of the level seen in faster-growing emerging markets.

South Africa’s lacklustre fixed capital formation over the past five years can be seen in the graph below.

R1.5 trillion goldmine

South Africa’s poor fixed capital formation rate is the main reason why the country’s economy remains stagnant, as businesses are unwilling to commit cash towards growth.

Instead, many invest to simply keep their doors open through “maintenance investment” to replace old equipment or alternative energy sources and backup water supply.

This investment does not result in a business growing its operations and increasing employment, but rather keeps it roughly where it is in terms of physical size.

The unwillingness to invest has resulted in South African corporates accumulating a cash pile of R1.5 trillion that sits in money market funds or call accounts, accruing interest.

Stanlib chief economist Kevin Lings said this cash pile is a result of a lack of confidence in the local economy and not a function of elevated interest rates.

He has gone as far as to say that interest rates could be cut in half, and there would not be a meaningful shift in cash out of these accounts and into fixed investments.

South Africa’s government has to create an enabling environment to foster confidence in the local economy and encourage businesses to invest in fixed assets.

For Lings, the state has simply run out of options due to its deteriorating financial health and the collapse of public companies. It cannot afford to invest by itself, as shown in the Reserve Bank’s data.

“We would have to up the investment considerably more to result in capacity building or job creation in South Africa,” Lings said.

“The current investment level is mainly maintenance capex and kind of treading water, with companies waiting for a better environment.”

“Instead of deploying capital into growth or hiring, corporates are parking it in money market funds or call accounts.”

This capital is desperately needed in South Africa to help build and maintain infrastructure vital to the proper functioning of a modern economy.

To get this capital off the sidelines and invested in the economy, the government has to create an enabling environment for companies. This begins with deregulation.

“I would say that deregulation is your only option now. It is your only choice, and while you may not like it ideologically, it is your only option,” Lings said.

“You are out of options, and those options have been taken away because you took government debt from 26% to 76% of GDP. That increase meant you have taken away your option to use your own balance sheet.”

For Lings, tapping into private capital in South Africa is a far better alternative than looking towards international lenders such as the World Bank and the International Monetary Fund.

“Your only options are international agencies. Or, talk to the local private sector and ask them under what conditions they would begin to invest in local industry,” Lings said.

“That is happening. That discussion is happening, and it turns out that companies and asset managers are interested.”

Comments