Pick n Pay’s Achilles’ Heel

Pick n Pay’s so-called ‘Achilles’ Heel’ is that its store network remains ill-suited to modern shopping trends.

This will make it difficult for the company to compete against the likes of Checkers and Woolworths, even if the retailer can solve its financial and other woes.

Concerningly, there is little the company can do to address this problem at the moment, as years of self-inflicted financial struggles have forced the company to reduce its store base.

However, with its store estate reset programme now concluded, Pick n Pay’s future store rollouts will focus on smaller stores, both to suit modern shopping trends and to keep the company’s lease-related expenses in check.

Otto1890 senior equity analyst Alec Abraham recently told Daily Investor that Pick n Pay’s ongoing turnaround is seemingly proving more difficult than initially expected.

Pick n Pay’s turnaround was ignited when stalwart Sean Summers was asked to return to the retailer’s helm and tasked with restoring the company to its former glory.

Prior to Summers’ return in October 2023 – he was also Pick n Pay’s CEO from 1999 to 2007 – the retailer found itself in a worrying position.

The retailer had been in decline for years, and following the disastrous Ekuseni Strategy, which was aimed at modernising the brand, it fell into an even deeper hole.

By the time Summers took over, Pick n Pay was technically insolvent, meaning its liabilities outweighed its assets, and the core Pick n Pay segment was running at a trading loss.

Thus began Pick n Pay’s turnaround under Summers’ leadership, with the CEO having hit the ground running from day one.

The first order of business was to address the company’s mounting liabilities, with the retailer’s gross debt having hit R11.4 billion in the 2024 financial year.

Summers’ solution was a two-step recapitalisation plan: a R4 billion Rights Offer and the listing of its subsidiary Boxer, which raised R8.5 billion.

This strategy allowed Pick n Pay to significantly reduce its debt and restored the retailer to a net cash position.

Since then, the company has also focused on improving its like-for-like sales, with some progress made in the 2025 financial year, though momentum seems to have slowed for FY26.

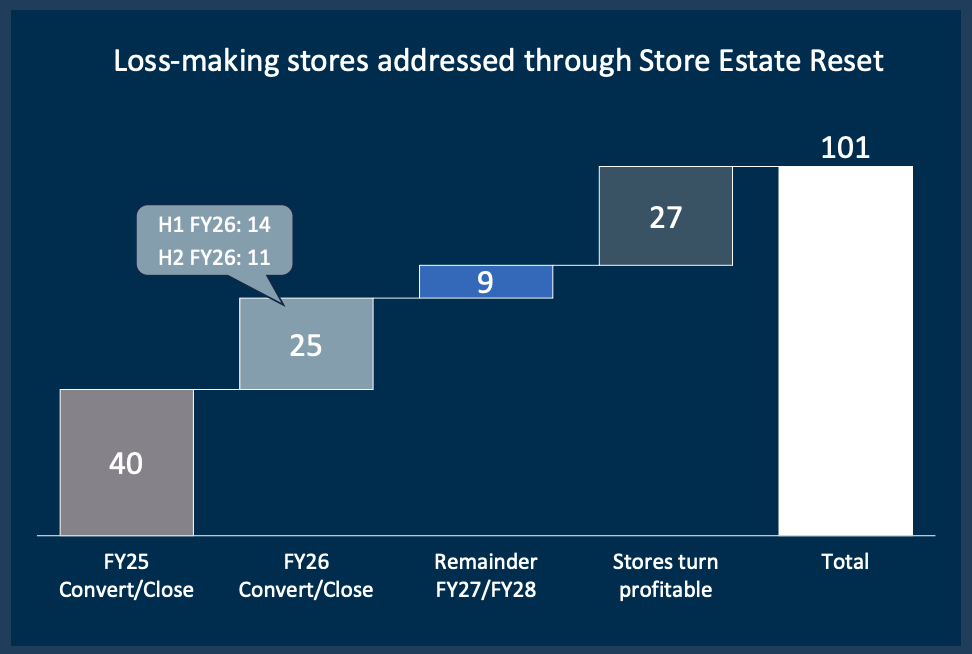

Pick n Pay has also undertaken a reset of its store estate, which involved closing numerous loss-making stores and converting others to different formats or Boxer stores.

As part of its turnaround, the company announced in early May 2026 that it had initiated a Section 189A consultation process, which is expected to affect store-based employees in the non-management bargaining unit.

Most recently, Pick n Pay announced plans to sell an 11.5% stake in Boxer, with the aim to raise R4.7 billion to further fund its turnaround.

The Achilles’ Heel

While Pick n Pay has made notable progress in its turnaround, Abraham told Daily Investor that the retailer’s “Achilles’ heel” will arguably be more difficult to resolve than other challenges, including its expense base and staff issues.

This Achilles’ heel, he said, is that Pick n Pay’s fleet of stores remains ill-suited to modern shopping trends.

“Gone are the days of large homes with pantries that can accommodate a large monthly shop,” Abraham explained.

“Consumers today tend to shop smaller baskets and much more frequently, often picking up on the way from work, or hailing Sixty60, for only what’s needed for that night’s cooking.”

This shift in consumer behaviour can clearly be seen in Discovery Bank and Visa’s latest SpendTrend26 report, which was built on data from 2.6 billion transactions.

According to the report, since 2021, grocery shopping frequency has increased by nearly 40%, while the average spend per basket has declined by 8%.

“This suggests that households are making more frequent trips to the store but buying smaller baskets each time,” it explained.

Abraham said Pick n Pay’s current store base does not align with this shift in consumer behaviour, as the retailer has fewer, larger stores in mainly middle- to upper-income areas.

Pick n Pay’s other challenges, which Abraham described as largely “self-inflicted”, also mean that the retailer will struggle to take advantage of the few opportunities it may have left to open more, smaller, conveniently located stores.

He explained that there is little the company can do to address this, with Pick n Pay’s competitors, Woolworths and Checkers, already having grabbed many of the viable locations that are left to “flood the zone”.

In an interview with Daily Investor following the release of Pick n Pay’s 2026 financial year results, Summers said that with the company’s store reset programme concluded, it is “looking to get back onto the expansion trail again”.

Future store rollouts, he said, will focus on adding more compact stores (around 2,300 to 2,500 m²), with an eye on keeping rents and rates contained.

In addition, Pick n Pay will now be able to focus on optimising its existing store network, with many refurbishments planned for the current financial year.

In the retailer’s 2026 results presentation, Summers also acknowledged the self-inflicted nature of many of Pick n Pay’s struggles, saying much damage was done to the company “from within”, with the ongoing turnaround aimed at fixing those mistakes.

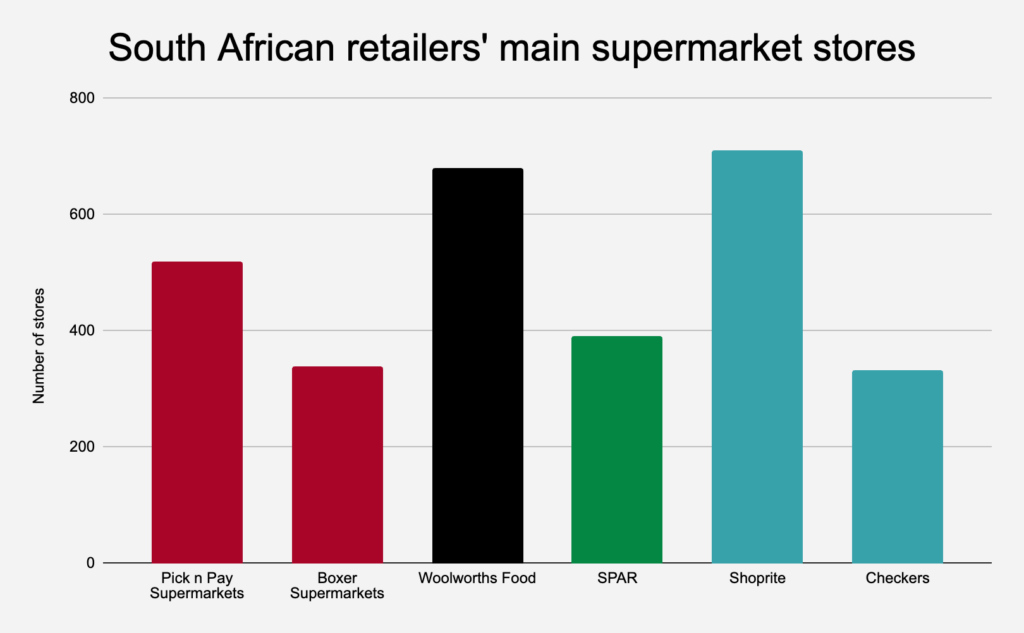

The first graph below shows the breakdown of store networks across South Africa’s major food retailers, with only their main/flagship supermarket brands included.

This reveals that Pick n Pay is relatively on par with some of its competitors in terms of the number of supermarket stores.

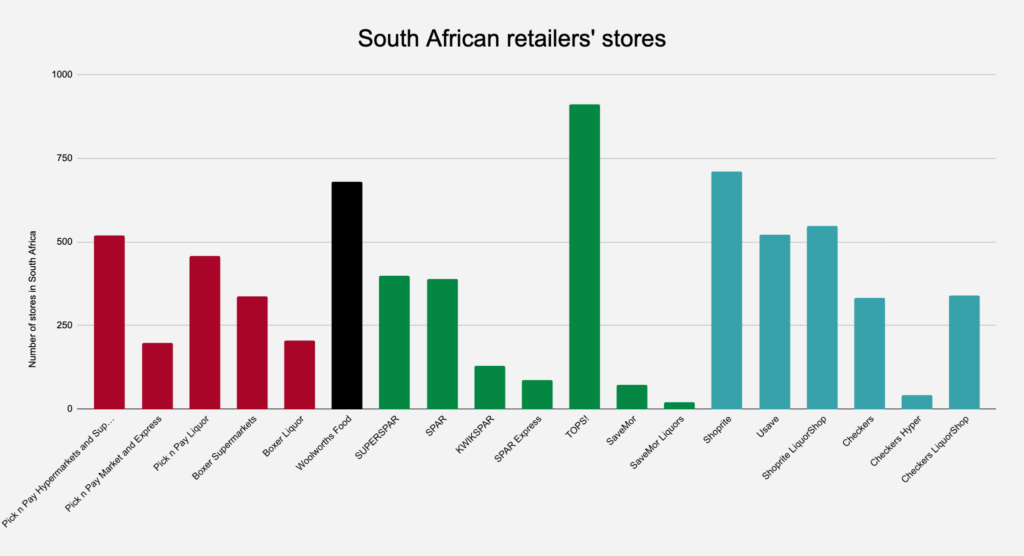

However, this picture changes when considering other retailers’ various food- and alcohol-related brands, shown in the second graph.

Graph 2

| Retailer | Number of food- and alochol-related stores in South Africa |

| Pick n Pay | 1,719 |

| Woolworths | 680 |

| SPAR | 2,011 |

| Shoprite | 2,493 |

Comments