Big South African miner taking pain

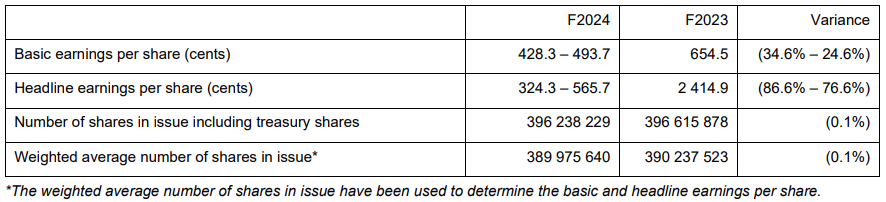

Northam Platinum is set to report poor financial results for its latest financial year. Due to lower platinum prices, headline earnings are expected to drop by up to 86%.

In a trading update for the year through June 2024, Northam informed shareholders that its sales revenue decreased by 22.2% compared to a 7.6% increase in cost of sales.

This resulted in a gross profit of R4.8 billion, compared to R15.4 billion in 2023. The miner’s gross profit margin fell to 15.7% from 39.1% the year prior.

“We operate a largely fixed-cost business and consider increasing our production, and doing so efficiently and sustainably, to be our best defence against current global inflationary pressures and fluctuating metal prices,” the miner explained.

“Our capital allocation and treasury decisions have been guided by our growth strategy and our results have benefitted from our consistent approach to growing our production base down the industry cost curve on a sustainable basis.”

The miner’s EBITDA, which excludes the loss on the sale of Impala Platinum shares, amounted to R6.3 billion for the financial year, compared to R16.5 billion in 2023.

Northam’s operations generated cash to the value of R3.5 billion before cash capital expenditure of R4.7 billion.

Its cash generation was impacted by negative working capital movements amounting to R2.4 billion relating to a build-up of inventory to the value of R1.2 billion and the settlement of trade and other payables of R1.0 billion.

This included the payout of profit share schemes across the group.

In addition, Northam paid R2.7 billion in dividends, and settled Domestic Medium-Term Notes to the value of R4.3 billion.

At year-end, the cash balance amounted to R7.5 billion.

However, the sale of Northam’s non-core investment in Implats shares contributed to a reduction in net debt to R3.1 billion, compared to R9.4 billion the year prior.

Northam said its financial results for the year are underpinned by a solid performance from all operations within the group, particularly from a cost containment and increased production perspective.

However, notwithstanding these contributors, Northam expects to report a significant decrease in earnings per share compared to the previous financial year, mainly as a result of a 35.5% decrease in the 4E ZAR basket price.

Northam expects its earnings to fall within the following ranges:

Comments