Old Mutual pumping money into these three companies

Old Mutual Investment Group believes that Naspers/Prosus, Bidcorp, and AB InBev are set to outperform in 2025 as investors search for diversified, resilient companies at attractive valuations.

The asset manager’s chief investment officer, Siboniso Nxumalo, and head of equities research, Meryl Pick, revealed this at its Q1 investment update.

Nxumalo explained that the asset manager’s outlook has changed dramatically over the past year. It now looks to rotate out of United States equities.

This rotation was spurred by concerns around the lofty valuations of US equities, with high expectations setting investors up for disappointment.

The second driver was Donald Trump’s re-election to the US Presidency, with his stated policies bringing fresh uncertainty to global markets.

This has pushed investors to look to ‘Trump proof’ their investments by finding companies that are well-diversified geographically and have minimal debt.

The rise of artificial intelligence (AI) has also pushed investors to look for companies exposed to the technology and pick winners likely to benefit from it.

Nxumalo explained that the obvious way to get exposure to these companies is to buy US tech giants such as Google, Amazon, Meta, and Nvidia.

Most investors would seek exposure to all of these companies through an S&P 500 index tracker or a Nasdaq 100 fund.

However, these indices are heavily concentrated in a handful of stocks benefiting from the AI boom. Their returns have been driven mainly by the Magnificent 7 – Apple, Microsoft, Google, Amazon, Meta, Nvidia, and Tesla.

The relative outperformance of these companies has created the most concentrated stock market in US history, with the top 10 stocks making up nearly 39% of the entire S&P 500.

These companies are beginning to underperform their lofty valuations, with their year-on-year growth slowing throughout 2024.

As a result, the US equity market has had a poor start to 2025, underperforming many of its peers as investors look elsewhere for returns.

Where Old Mutual is investing

In this environment, Nxumalo explained that Old Mutual is looking outside of the US for returns as the asset manager believes the world’s largest stock market will underperform its peers.

Given the elevated uncertainty regarding Trump’s trade policies, Nxumalo explained that well-diversified companies are also very attractive.

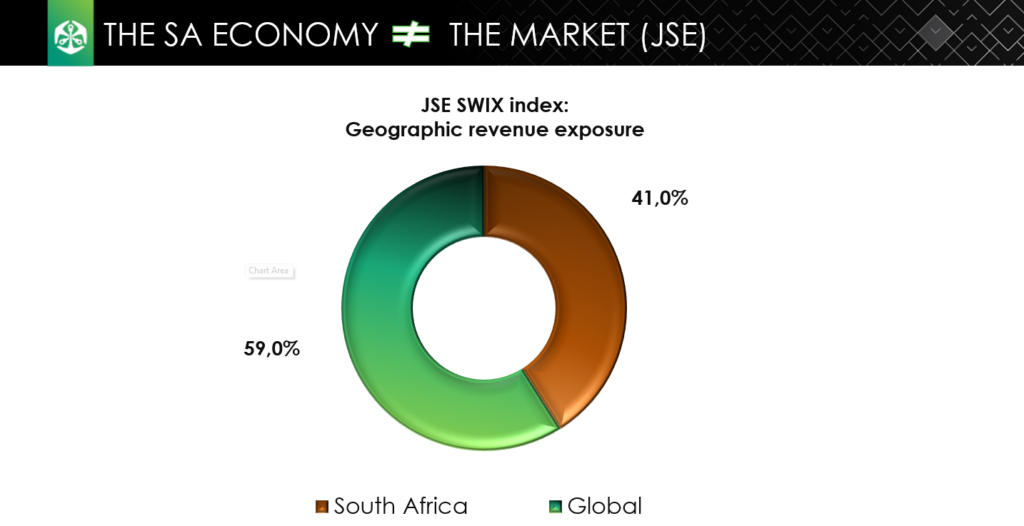

Pick said that South Africans do not have to look beyond the JSE for these kinds of companies, with the local stock exchange being more diversified than many think.

The majority of the earnings of the top 40 largest companies on the JSE come from outside of South Africa, so investors should not confuse the returns from these companies with the local economy.

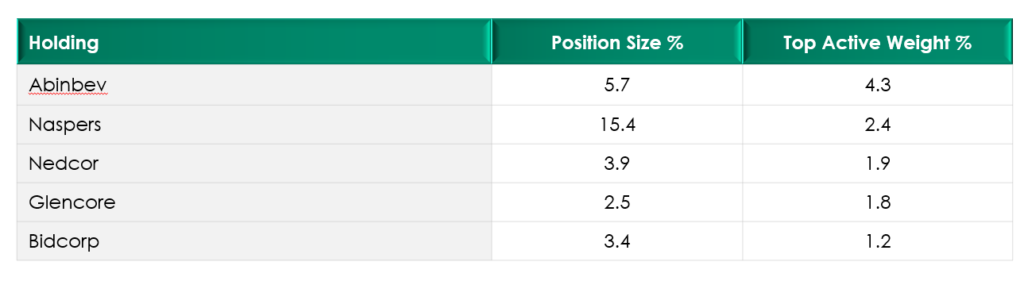

Nxumalo and Pick used Old Mutual’s flagship equity fund, the Investors Fund, as an example of how they allocate clients’ money in this environment.

The fund is overweight resources companies, defensive stocks, and global technology companies compared to its peers.

It has been steadily trimming its positions in South African banks and gold miners as it believes that these companies are set to experience more headwinds than tailwinds for the rest of 2025.

Nxumalo and Pick highlighted three JSE-listed companies they are particularly attracted by in more detail. Their investment theses around these stocks are outlined in more detail below.

Naspers/Prosus

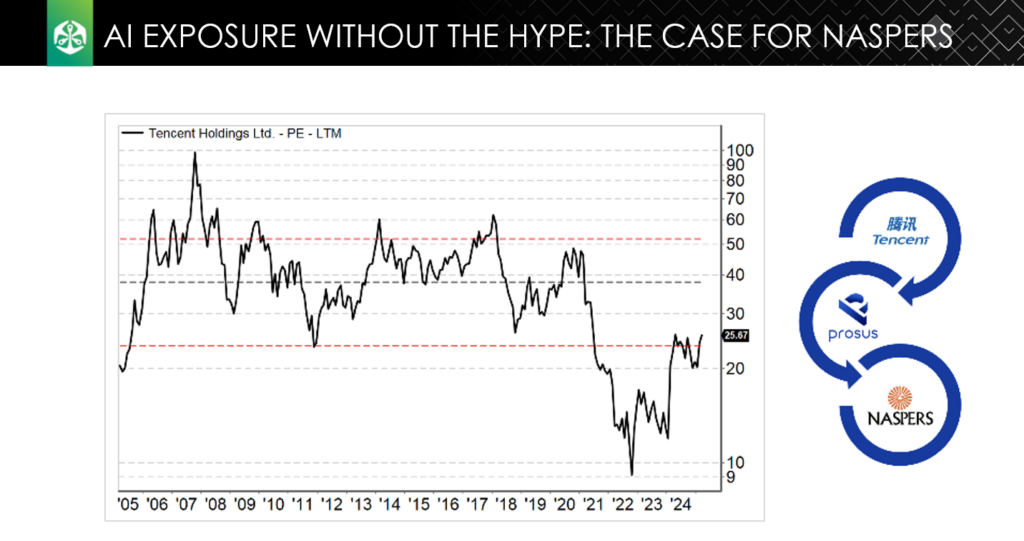

One of the best ways for investors to be exposed to the AI boom is through Naspers and Prosus due to their investment in Chinese tech giant Tencent.

Nxumalo explained that this is essentially AI exposure without the lofty valuations seen in the US and the industry’s overhyped nature.

The investment can also come at a significant discount, through Naspers/Prosus, and at an attractive valuation, as Chinese stocks have been under pressure for the past few years.

Crucially, Nxumalo said that Chinese tech stocks remain attractively valued because their heavy investments in AI and advances in the sector are underappreciated.

He noted that Chinese companies actually dominated the number of patents issued for AI-related technologies in 2024, pointing to DeepSeek’s R1 model as an example.

“This is something that nobody talks about and thinks about, yet it is fundamentally important because these Chinese companies are very much at the bleeding edge of AI,” Nxumalo said.

To invest in an American company with a similar level of AI capability as Tencent, you would pay, on average, 50% more in terms of price-to-earnings.

“This, for us, is AI exposure without the hype of the US and has the potential to be a great investment.”

Nxumalo explained further that Nasper/Prosus might be the best way to be exposed to Tencent rather than buying it directly because they trade at a discount to the value of their investment in the Chinese giant.

This may compound the potential return on the investment.

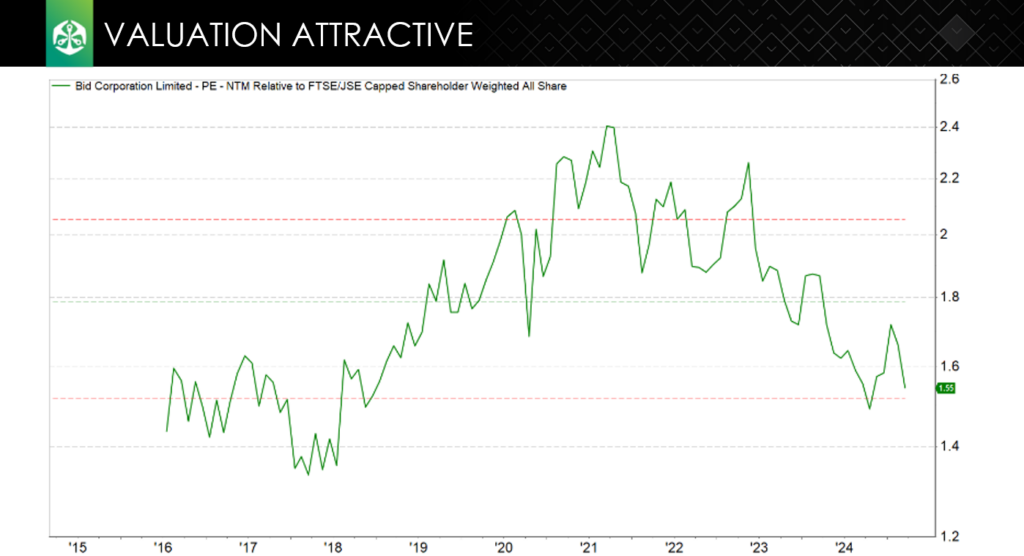

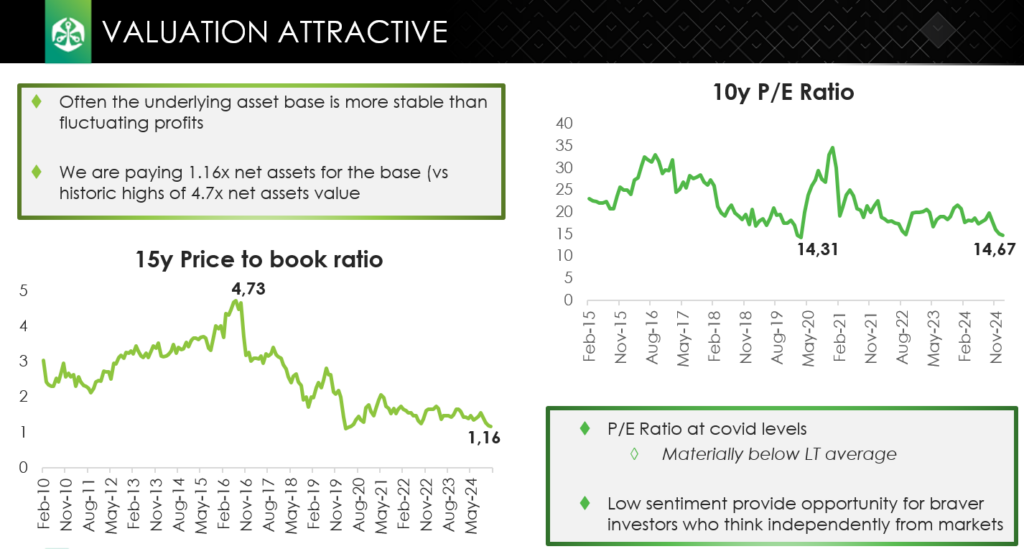

Bidcorp

Bidcorp is an extremely attractive investment almost purely because of the current geopolitical environment, Pick explained.

The company is exceptionally well-diversified geographically, making it resilient against any targeted tariffs from the US, and is not overly exposed to a single sector.

Bidcorp is an international broad-line food service group that has operations in developed and developing economies on five continents.

It also has a dominant position in many of these markets, giving it significant pricing power – which is the ability to pass costs on to customers without losing market share.

“By virtue of this, in particular its decentralisation, Bidcorp is relatively insulated from all the global supply chain issues that many companies face,” Pick explained.

These issues are only set to intensify in 2025, with a potential trade war throwing supply chains into disarray.

Pick also said the company has no exposure to the US, meaning it can avoid any direct impact from a slowdown in the world’s largest economy.

The company also has a high-quality management team with a track record of efficient capital allocation through small, bolt-on acquisitions to grow market share.

“They have been on this journey for more than ten years, and we think there is a significant runway for future growth.”

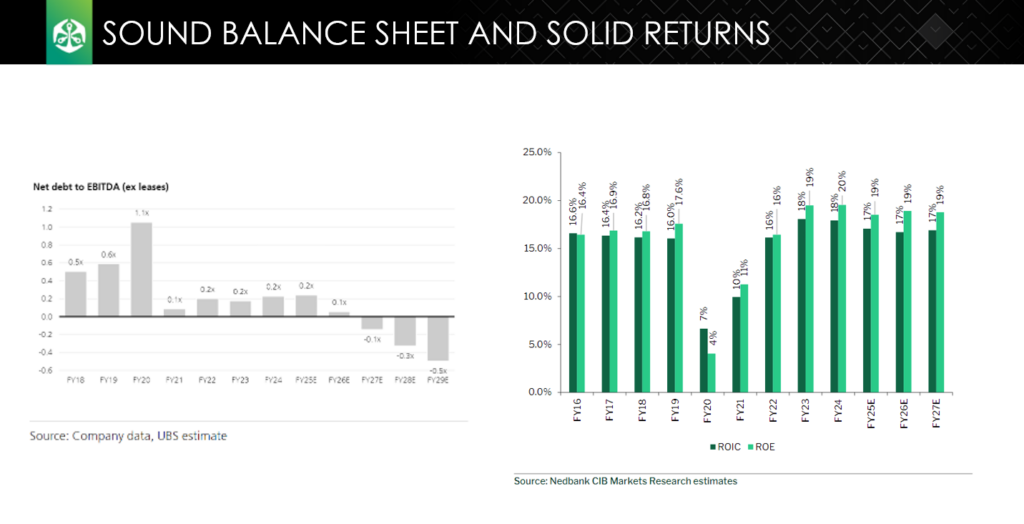

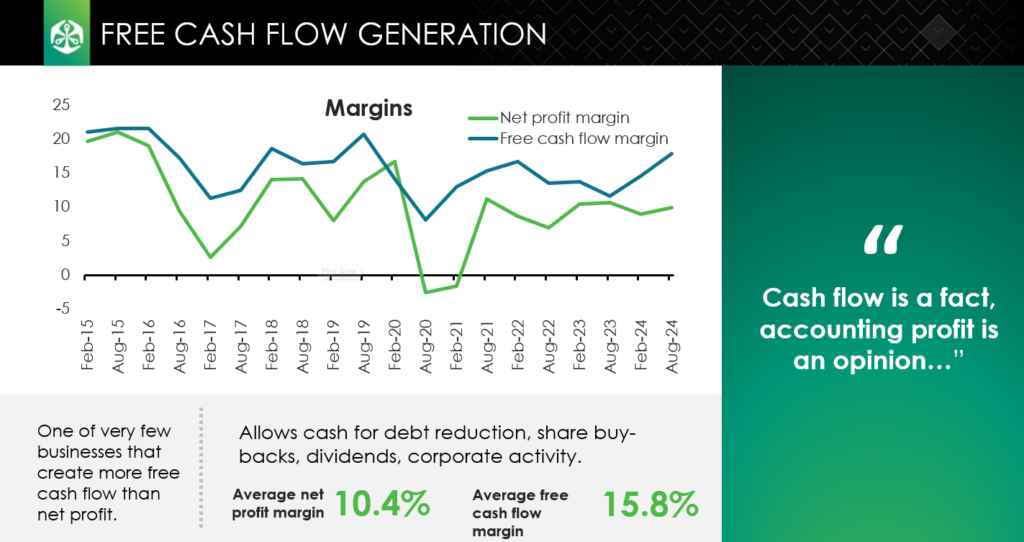

Amid elevated uncertainty, Bidcorp also provides stability, with its earnings outside of the COVID-19 period being very consistent and in excess of the cost of capital.

Crucially, the company also has a very strong balance sheet, ensuring it can weather any external shock and potentially acquire other businesses if needed.

“So, we think we are getting a great global company that is well-diversified, not overly exposed to the US and disrupted supply chains, at a price-to-earnings multiple that is relatively cheap.”

AB InBev

The third company that caught the attention of Old Mutual is beer producer AB InBev, which acquired SABMiller in 2016.

Similarly to Bidcorp, the company is heavily diversified and not reliant on a single market for the majority of its returns.

While the US does make up a large share of the brewer’s revenue, it has seen strong growth in emerging markets in recent years that are not significant contributors to revenue and profits.

More importantly, the company has pricing power in all of its markets, with its brands being dominant players around the world.

This enables it to absorb shocks and pass costs on to consumers, if needed, to protect margins and ensure stable returns.

As with Bidcorp, amid an uncertain environment, AB InBev has proven itself to generate predictable returns that steadily grow over time.

However, Pick is concerned that AB InBev has a significant amount of debt on its balance sheet.

While this is a concern, Pick does not think it is a risk to the company as the debt is exceptionally well structured, with no concentrations of repayments in the short-term and much of it being non-bank debt.

Much of this debt came from the purchase of SABMiller in 2016, with Pick saying that AB InBev probably overpaid for the company.

“Previous investors have paid that price and we do not have to pay it now, with the company having digested the acquisition and beginning to drive operational efficiencies.”

Furthermore, the company tends to outperform in difficult times, with its products well spread across the price range.

“We think that people will always drink beer, no matter how tough times are,” Pick said.

“We think over time they can trade their way out of the commodity spikes and also out of the debt, with its cashflow generation remaining strong.”

“Compared to history, where it has traded at three times the value of its book, it is not trading only at one time its book value, so it is very underappreciated by the market.”

Comments