Remgro executives under siege

Shane Watkins from All Weather Capital blamed Remgro’s management for the poor share price performance, saying they lack energy and do not act in shareholders’ interest.

Watkins made these comments during a Business Day TV interview following Remgro’s annual general meeting (AGM).

Remgro has performed poorly over the last decade. Its share price has been down 40% over 10 years, which has caused widespread shareholder unhappiness.

Investors showed their discontent with the Remgro management team at the AGM, with 34% of ordinary shareholders voting against the remuneration implementation report.

Many shareholders also voted against the remuneration policy, and placing unissued ordinary shares under the control of the directors.

The unhappiness was so striking that Remgro said it would like to engage its shareholders on its remuneration implementation report.

This engagement aims to understand why shareholders voted against the report and enable the committee to consider these concerns on behalf of the Remgro board.

Watkins, the chief investment officer at All Weather Capital, said Remgro offers a good investment because it has great assets and poor management.

“I am not talking about the management of the operating level. I am talking about the management at Remgro’s executive level,” he said.

He said Remgro’s big stake in OUTsurance, a fantastic company, and Discovery, a fabulous business, are great assets.

Their shareholding in Maziv, through CIVH, Mediclinic, and Heineken, are equally very good assets.

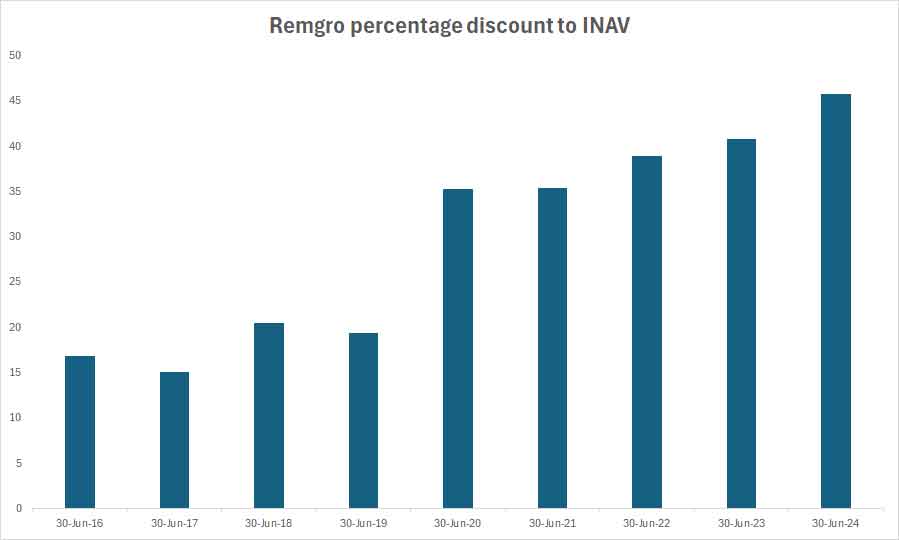

Remgro’s latest financial results stated that its intrinsic net asset value per share is R251. However, it only trades at R150 per share.

Between 30 June 2023 and 30 June 2024, the percentage discount to intrinsic net asset value increased from 40.8% to 45.8%.

Watkins said there are two reasons why Remgro’s share price is underperforming:

- The underlying operations in Remgro’s portfolio have underperformed.

- Remgro’s management is unenergised, and they have not acted in the best interest of shareholders.

“There is a sufficient margin of error, notwithstanding the misgivings of management, for it to be a good investment,” he said.

Remgro excuses

Remgro chief executive Jannie Durand had many excuses for the big trading discount, including its higher ratio of unlisted investments.

He highlighted that Remgro recently completed corporate transactions relating to its investments in Mediclinic and Distell and unbundled its interest in RMH on 8 June 2020.

Before these transactions, 23% of the value of Remgro’s investment portfolio was represented by unlisted investments.

Before these transactions, the share price traded at a discount to intrinsic net asset value of less than 30%.

“While the subsequent widening of the discount was not anticipated, it highlights the importance of demonstrating the veracity of the intrinsic net asset valuations,” he said.

It was difficult to find any mention of where the Remgro management team took responsibility for the company’s poor performance.

Instead, Durandt mentioned load-shedding, negative sentiment, economic headwinds, high inflation, and whatever else he could find to explain the poor performance.

However, it was clear that shareholders saw it differently. They wanted to see action to address the difference between NAV and the share price.

The discount has become so concerning that Remgro’s remuneration committee changed the performance measures of management’s long-term incentives.

It includes two new financial measures – total shareholder return (TSR) and headline earnings per share (HEPS).

The addition of the TSR measure aims to focus management strategies and efforts on growing the share price, narrowing the discount to INAV.

Remgro believes that the revised performance measures represent a strong alignment with shareholders, which motivates executives to address their discount concerns.

Over the last eighteen months, Remgro has also engaged in a share repurchase programme to add value to shareholders.

This did not significantly help to bolster the share price and narrow the discount, which shows the company’s challenge.

Percentage discount to INAV

The chart below shows Remgro’s percentage discount to intrinsic net asset value (INAV) over the last eight years.

Comments