How South Africans should invest with a Trump presidency

Donald Trump’s presidency will likely introduce significant volatility into financial markets, with some assets being declared winners and others losers.

However, overall, the US and global stock markets are generally unaffected by who sits in the Oval Office, with the value of assets being largely determined by fundamental factors such as a company’s earnings and interest rates.

This is feedback from Old Mutual Wealth investment strategist Izak Odendaal, who said the worst potential outcome – months of uncertainty – was avoided.

The initial market response was for the dollar to rally, US bonds to sell off, bond yields to rise, and equities to jump.

Unlike in 2016, this election outcome did not come as a complete surprise and markets were broadly positioned for a Republican win.

Odendaal said the speed with which the results were finalised was also positive. Markets hate uncertainty, and a drawn-out or contested result would have weighed on sentiment.

While there were some notable market moves, the past week did not stand out as unusually volatile. In the immediate term, Trump, most importantly, favours lower taxes and deregulation.

His 2017 tax cuts were due to expire in 2025 and are now likely to be extended, while corporate tax rates might be lowered even further.

Lower tax rates and deregulation are positive for company profitability, at least in the short run, and are therefore good for the stock market.

Bank shares, in particular, surged last week in anticipation of an easement of onerous capital requirements and the approval of more mergers and acquisitions.

Any additional tax cuts will have to be funded by additional borrowing unless there are spending cuts, which seem unlikely.

Therefore, the federal government’s debt will continue to rise, possibly by several trillion more on top of the pre-Trump estimated trajectory.

Then again, we should also remember that markets have a way of disciplining wayward politicians and moving in bond yields, and/or the dollar could rein in Trump’s ambitions.

Overall, a Trump presidency is likely to be not entirely good or bad for investment portfolios. There will be winners and losers across different sectors of the global economy and across different asset classes.

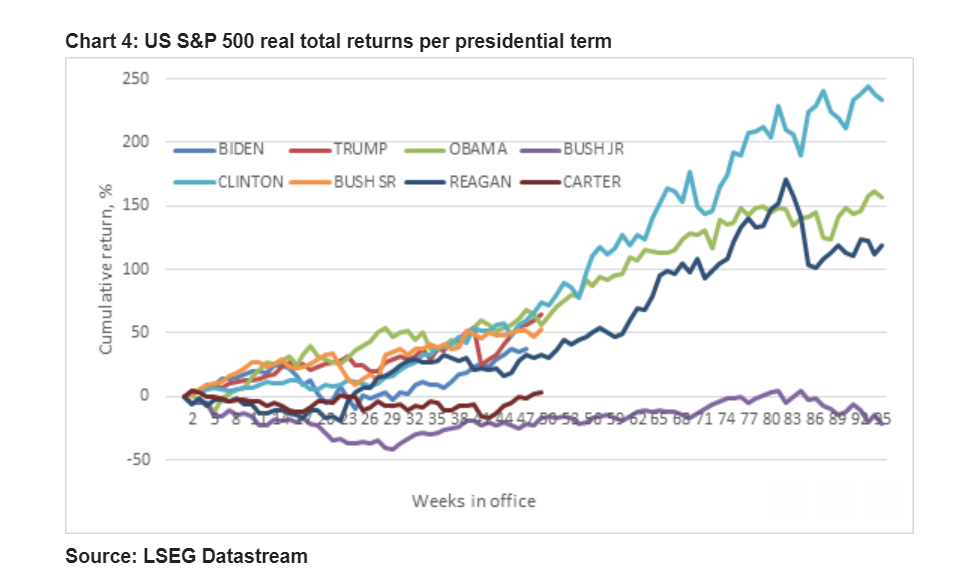

Historically, the US stock market has performed well irrespective of which party controlled the White House, as the graph below shows.

The two terms of George W. Bush were an exception, given that they coincided with the dotcom crash at the start and the financial crisis at the end.

One thing that is guaranteed for South African assets is that Trump will bring renewed volatility, with policies changing at short notice.

This will require more patience on the part of investors and focus to not try to second guess everything Trump says or does, but rather on appropriate diversification and sticking to the investment plan for the four years.

Another certainty is that the outlook for the Reserve Bank’s interest rate-cutting cycle has not changed, and it will continue to proceed with caution, as it has done for the past few years.

It helps that the rand has been remarkably resilient, only experiencing brief volatility on the day the election results were released.

Odendaal said South Africa should remain on the path of economic reform so that it can become more reliant on internal growth drivers in an uncertain global environment.

For instance, if there is to be further upward pressure on global bond yields, we should expect spillover to domestic markets with higher local bond yields.

This makes it important to continue fiscal consolidation efforts and improve our relative standing in the eyes of investors.

Securing credit rating upgrades could help get off the Financial Action Task Force’s grey list. Doing so is fully in South Africa’s hands, not in Trump’s.

However, one major threat a Trump presidency poses is the potential for tariffs on imports from South Africa.

Attempts to retain duty-free access under the African Growth and Opportunity Act (AGOA) will almost certainly be complicated.

AGOA allows South Africa duty-free access to the US for certain exports, which play an important role in supporting the South African economy.

Trump has in the past questioned the benefits of AGOA for their economy and might consider revising or even restricting South Africa’s access.

Any loss of AGOA privileges would likely disrupt South African exports, affect growth projections, and place further pressure on the rand.

Another major issue for South Africa is Trump’s adversarial approach to China, with the promise of tariffs and trade restrictions significantly hampering the world’s second-largest economy and its demand for commodities.

Should he resume tariffs or restrict imports broadly, it could slow global trade, diminish demand for South Africa’s exports and weaken the rand due to reduced foreign exchange inflows.

As global commodity demand fluctuates, so does the rand, which is highly sensitive to shifts in export volumes and prices.

Comments