End of an era for the US dollar

The US dollar’s inexorable strengthening for the past 15 years appears to be coming to an end as investors are increasingly concerned about America’s financial health and whether its outperformance will continue.

This means that the rand’s steady weakening against the US dollar may be coming to an end, not necessarily because of the South African currency’s strength but because the greenback is losing ground.

So far in 2025, investors have shied away from investing in the traditional safe haven of US Treasury bonds, looking to Europe, Japan, and Switzerland for enhanced stability.

This is largely a result of the increased uncertainty created by US President Donald Trump’s imposition of tariffs on the country’s trading partners and increased scepticism of the financial health of the US government.

The United States continues to run record deficits out of wartime, increasing its debt load to over $36 trillion, and resulting in it spending more on servicing its debt than on its renowned military.

As a result, emerging market currencies, such as the rand, will likely strengthen against the dollar over a sustained period for the first time in a decade.

Coupled with a potential commodity boom, the rand could strengthen significantly, helping to contain inflation and attract investment.

This is feedback from Old Mutual Wealth’s chief investment strategist, Izak Odendaal, who outlined some reasons why the US dollar is expected to underperform in the future.

Odendaal explained that it has little to do with the dollar potentially losing its status as the world’s reserve currency. It remains dominant in that sphere without much change over time.

Furthermore, the dollar remains the primary currency used for global financial flows, making it indispensable for global trade.

The most important factor for investors and South Africa, however, is the dollar’s value in foreign exchange markets. In other words, how many rands, euros, or yen does it cost to buy a dollar?

The market sets the exchange value of currency as a result of millions of daily transactions, each with a slightly different motivation. Some are linked to imports and exports, some to capital flows, and a lot to speculation and trading.

Interest rate differences matter since higher current or expected future relative interest rates will pull in money, and vice versa. Since a currency pair always involves two countries, what is happening in the other country matters.

The dollar’s strength over the past 15 years largely reflects stronger economic growth in the United States, and consequently higher interest rates, as this attracts capital, Odendaal said.

For a time, Europe and Japan had negative nominal interest rates, practically begging investors to go elsewhere.

Moreover, the stunning outperformance of its large technology shares made the United States equity market a must-own for investors worldwide.

As the dollar gained, it boosted the value of US investments for non-US investors and similarly made international investments unattractive for Americans.

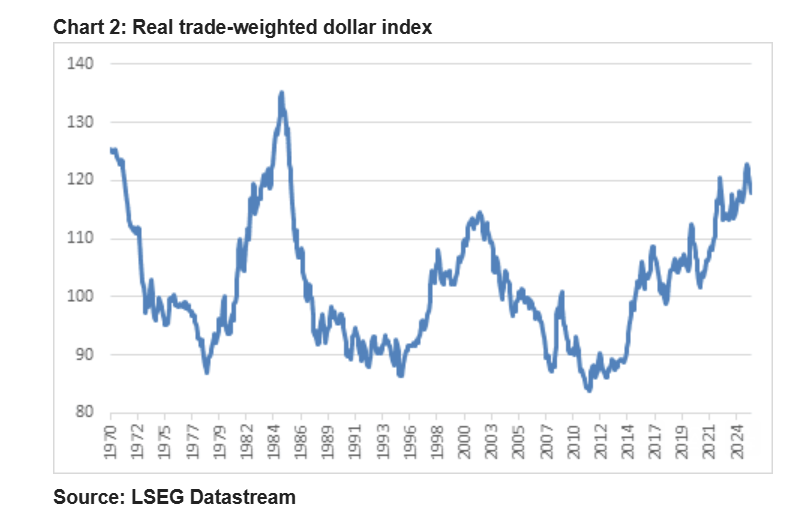

Add in geopolitical risk, such as Russia’s war in Ukraine, and at the start of the year, the real trade-weighted dollar index shown was near its highest level since 1970.

In 50 years, it was only stronger 5% of the time. From this elevated level, there is naturally little upside and plenty of room to decline, Odendaal said. This can be seen in the graph below.

Dollar set to decline

Apart from the dollar declining to revert towards fair value, the currency is also likely to come under pressure from the United States’ declining financial health and uncertainty surrounding its trade policy.

This will benefit emerging market economies and currencies, such as the rand, as it will become relatively cheaper to import goods into these countries.

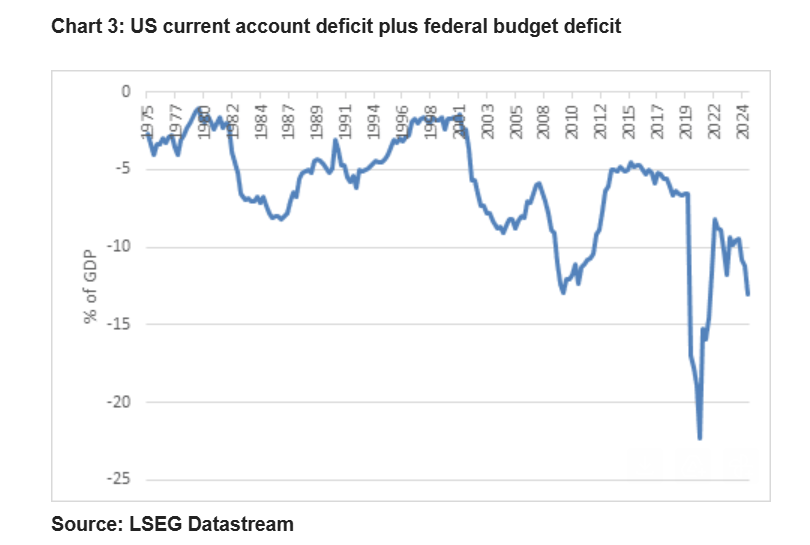

If it were any other currency, the dollar would have fallen much further, much earlier, given the rapidly growing “twin” deficit, the combined shortfall on its current account and budget balances, Odendaal said.

The catalyst for the decline so far this year was President Trump’s trade and fiscal policies. Initially, the dollar rallied on his election, on the expectation that US growth outperformance would be given a boost.

However, since he has taken office, there is a lot about the Trump administration that has made investors nervous.

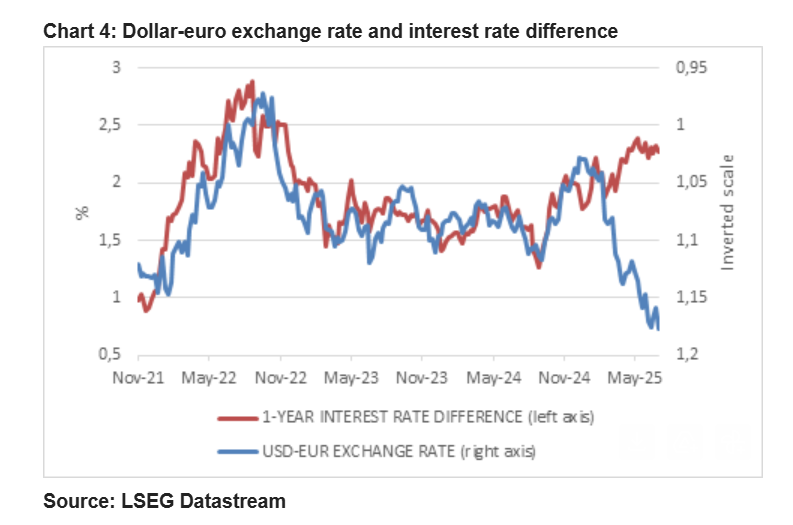

This can be seen in the decoupling of the dollar from interest rate differentials. Normally, elevated US interest rates would have resulted in a stronger dollar. Instead, it has fallen 13% against the euro this year.

Apart from the tariff uncertainty, investors’ biggest concerns include the inexorable rise in US government debt levels and the independence of the Federal Reserve.

Trump’s visit to the Fed’s headquarters last week was clearly designed to renew pressure on the Fed to cut rates, following weeks of speculation about whether he would fire Jerome Powell as the central bank’s chairman.

Even when Trump departs the scene, deep political divisions in the United States mean these issues will not go away anytime soon. Therefore, Odendaal said, the world’s overexposure to US assets no longer seems a sure bet.

Recklessness in Washington can do much more for de-dollarisation than scheming in Beijing or Moscow, and international investors are rethinking their overweight allocations.

This does not imply a mass exit from US positions, but more likely reduced inflows. It doesn’t mean people will stop using the dollar or accepting it as payment.

This is not the death of the dollar by any stretch of the imagination, but probably the end of a 15-year run of appreciation.

Nothing happens in straight lines, however, and if this is the start of a down cycle – as seems to be the case – there will still be dollar rallies.

The extent of the cycle will also be limited by the fact that all other major currencies have problems of their own.

A weaker dollar would benefit the world economy precisely because businesses across the world so widely use it.

If it is cheaper to get hold of dollars to pay suppliers or to service debt, it is helpful. It also usually implies lower interest rates in other countries.

Periods of strong performance in emerging markets, such as South Africa, typically coincide with a weaker dollar and boost the value of their currencies. This has the potential to create a virtuous cycle for emerging economies.

The graphs below show the deterioration in the United States’ financial health and its decoupling from interest rate differentials, indicating a shift in investor perception of US assets.

Comments