South Africa can go from junk to darling

South Africa is on the path to escape ‘junk’ status in the coming years, with some rating agency upgrades expected as soon as this year.

This is on the back of improved government financial health as fiscal consolidation begins to bear fruit with consecutive primary budget surpluses.

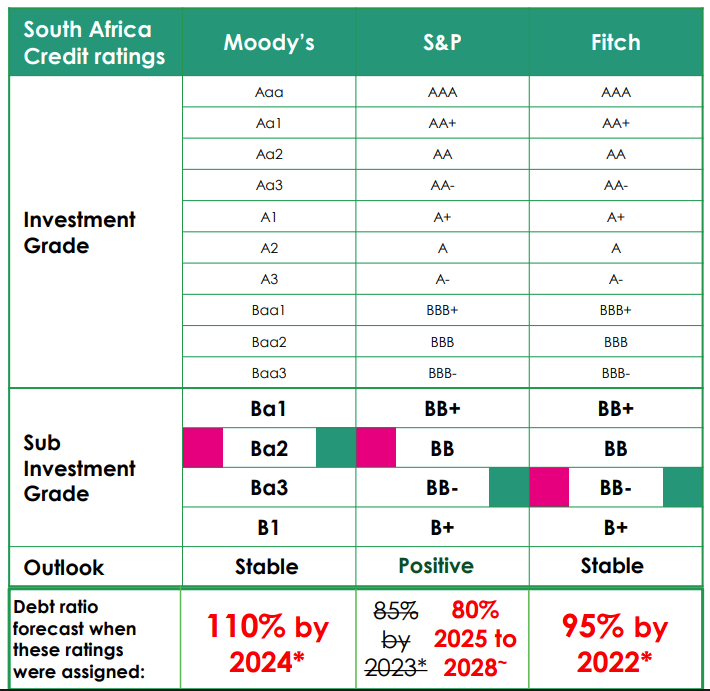

Currently, South Africa is deep in sub-investment-grade territory, with all three major ratings agencies – Moody’s, S&P Global Ratings, and Fitch.

While these institutions were relatively quick to downgrade South Africa to sub-investment grade, or junk status, improvements in the country’s credit ratings have been much slower.

Old Mutual’s chief economist, Johann Els, believes they are behind the curve and are failing to reflect improving growth prospects and easing financial risks.

When these institutions downgraded South Africa to its current ratings level, they forecasted a significantly higher debt-to-GDP ratio for the country.

This was essentially an extrapolation based on the government’s accelerating spending in the 2010s, which was coupled with poor economic growth.

As a result, the country’s debt burden began to balloon due to the repeated budget deficits, with ratings agencies taking note and downgrading the country’s credit rating.

Being placed into junk status prohibits many global pension funds and investment schemes from investing in South African assets, as they are considered ‘below investment grade’.

This resulted in significant outflows from South African assets over the past few years, significantly weakening the rand and further limiting economic growth.

In turn, this creates a vicious cycle where declining investment further weakens economic growth, negatively impacting the government’s finances and increasing the risk of investing in the country.

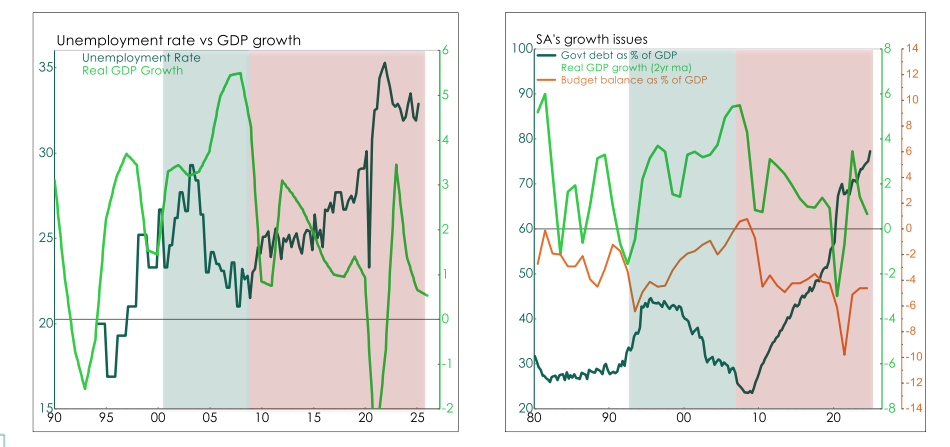

South Africa has been in this cycle for the past 15 years, with the government running its last budget surplus in the 2007/08 financial year. Since then, it has consistently run deficits while economic growth has slowed.

This pattern is evident in the two graphs below, which illustrate the relationship between economic growth and unemployment, as well as the relationship between growth and the state’s budget balance and government debt.

Things are looking up

Els explained that after 15 years of this vicious cycle, things are beginning to look up for South Africa, and it may enter a virtuous cycle.

While economic growth has remained lacklustre, the National Treasury has been implementing a policy of fiscal consolidation.

In effect, such a policy tries to contain spending growth below inflation and tax revenue growth, to create a primary budget surplus.

This has been the case for the past two years, with the government recording primary budget surpluses, which are expected to widen.

A primary budget surplus means the government is spending less than it earns from tax revenue, allowing it to limit the growth in debt.

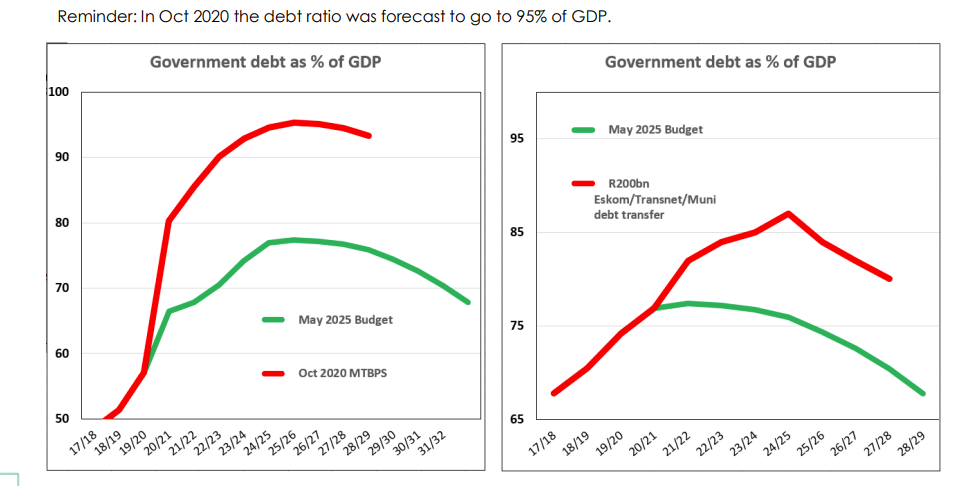

As a result, the government’s debt burden is expected to peak in the coming financial year and begin to trend downward as funds are freed up to start paying down the principal owed.

A crucial part of this has been the National Treasury’s hard stance on financial assistance to state-owned enterprises (SOEs), which have been a drain on the government’s resources.

If the government had been more freely assisting Eskom, Transnet, and other SOEs, as well as municipalities, the country’s debt-to-GDP would have continued to rise and peaked at over 85% rather than the current forecast of 76%.

Alongside improved economic prospects, this should be enough for South Africa’s credit ratings to improve in the coming months and years, Els said.

Ratings agencies are behind the curve, failing to reflect improving growth prospects and fiscal risks, as shown by rising primary budget surpluses and the peaking debt-to-GDP ratio.

These metrics look far better than what was anticipated by the three ratings agencies when they assigned South Africa’s latest ratings.

Moody’s anticipated the debt-to-GDP ratio to hit 110% by 2024, S&P saw it reaching 80% after 2025, and Fitch forecast it to hit 95% by 2022.

South Africa’s finances are in a far better position at the end of the 2024 financial year than any of those forecasts, pushing Els to say that they are behind the curve.

With improved state finances and enhanced economic growth, improvements in the country’s credit rating could push South Africa into a virtuous cycle.

In this cycle, improvements in the country’s credit rating result in additional investment into the country, accelerating economic growth and further improving the state’s finances, leading to further credit rating improvements.

The graphs below show South Africa’s improved financial metrics and the current investment grades assigned by the three ratings agencies.

Comments