South Africa’s double-edged sword

The lowering of South Africa’s inflation target poses both opportunities and challenges for the country, with the long-term benefits clear but the short-term filled with jeopardy.

A lower inflation target is likely to lead to a more accommodative monetary policy, boosting economic growth and easing pressure on households.

It will also reduce the government’s cost of borrowing and free up billions for the state to invest in infrastructure or other areas of the economy.

However, in the short term, a lower inflation target may mean higher interest rates and slower economic growth as the Reserve Bank works to maintain its targeting credibility.

This is feedback from Melville Douglas’ chief investment officer, Bernard Drotschie, who outlined the wealth manager’s outlook at the end of the second quarter of 2025.

The National Treasury and the Reserve Bank have confirmed their intention to lower the country’s inflation target from the current 3% to 6% range.

This lowering is vital for future price stability and the strength of the rand and aligns South Africa with global monetary policy standards.

Drotschie explained that this change has important implications for the direction of interest rates, which means it will impact the country’s economic growth.

With headline inflation currently at 3% and core inflation near the lower end of the existing target range, the Reserve Bank sees an opportunity to reinforce low inflation expectations.

According to modelling presented at the recent Monetary Policy Committee (MPC) meeting, a 3% target could accelerate the decline in inflation expectations, potentially allowing for a more accommodative interest rate stance over the medium term.

This will boost economic growth and ease the government’s debt-servicing burden, promising to be almost a silver bullet for its current challenges.

The Reserve Bank’s research points to increased economic growth of over 0.25% per year within five years and 0.4% within a decade from a lower inflation target of 3%.

These estimates are conservative, with the benefit set to be greater as lower interest rates ease the government’s debt-servicing costs and increase productive investment.

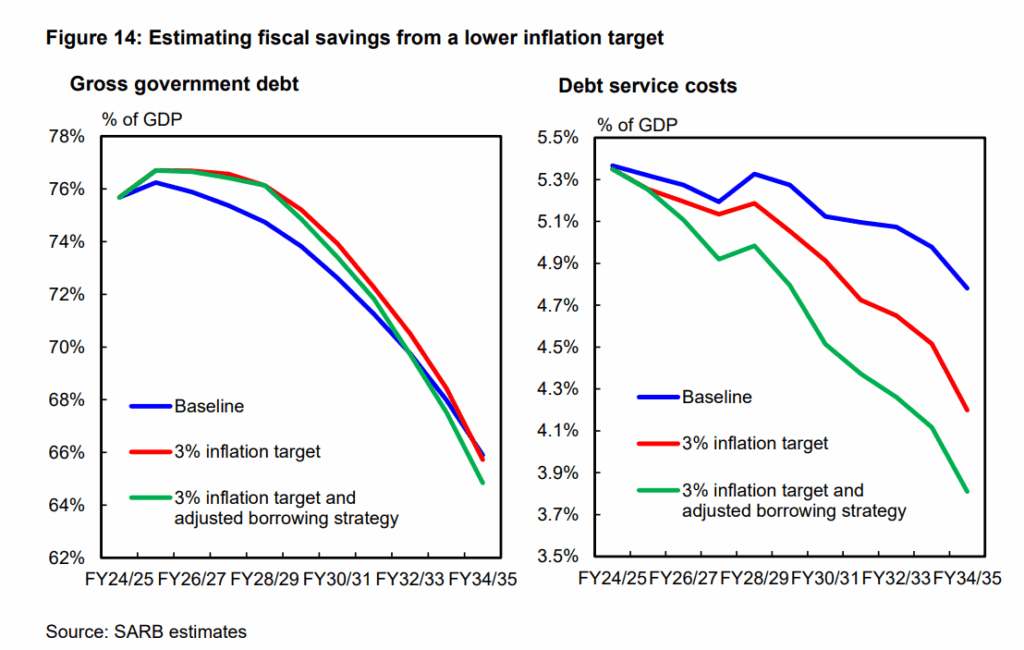

In terms of the state’s debt-servicing costs, a lower inflation target will bring slight relief in the immediate future but gather momentum over time to reduce interest expenditure by billions of rands.

A lower inflation target could see debt-servicing costs fall from 5.4% of GDP to 5.1% by 2030 and 4.2% in 2034/35. This should translate into around R130 billion of nominal fiscal savings that would be realised in the first five years, rising to R600 billion by the end of the next decade.

This can be seen in the graphs below.

Short-term challenges

The longer-term benefits of a lower inflation target are expected to come with short-term trade-offs, resulting in lower economic growth – something South Africa cannot afford.

The potential lowering of the target range is already impacting the Reserve Bank’s approach to monetary policy, with it looking to keep inflation as close to 3% as possible.

This will reduce the short-term costs associated with the transition to a lower target and help bring inflation expectations in line.

As a result, the Reserve Bank is expected to remain cautious in the short term, with the MPC emphasising the need to anchor expectations before considering any easing in interest rates.

Over time, as credibility in the new target builds, Drotshie anticipates a gradual reduction in policy rates.

This would support investment and consumption, particularly in interest-sensitive sectors such as housing, durable goods, and capital-intensive industries.

That said, the transition may involve some short-term trade-offs, requiring a more restrictive monetary stance initially, which may weigh on growth. This is particularly relevant given South Africa’s modest growth outlook.

Old Mutual portfolio manager Jason Swartz emphasised this risk, saying that if the move to a lower target rate does not come at a time when inflation is already low and expectations are moving downwards, there could be trouble.

“The Reserve Bank believes that it has quite a lot of credibility around managing inflation, which should help push down expectations,” he said.

“Inflation expectations should adjust, but the risk for us is that if they do not adjust, then the sacrifice in terms of growth that they have to give up to reach the lower target could be substantial.”

However, the long-term benefits could be substantial if the new inflation framework is supported by credible fiscal consolidation and meaningful structural reforms.

From a market perspective, the implications are broadly constructive, with fixed-income markets benefitting from a decline in long-term yields as inflation risk premia compress.

Equities, particularly in consumer-facing and interest-sensitive sectors, could see improved valuations if lower rates stimulate demand.

While the exact timing of implementation remains uncertain, this policy shift represents a proactive step toward building a more stable and competitive economic environment.

Drotschie said that if executed effectively, it could lay the foundation for stronger, more sustainable growth in the years ahead.

Comments