High stakes for Enoch Godongwana

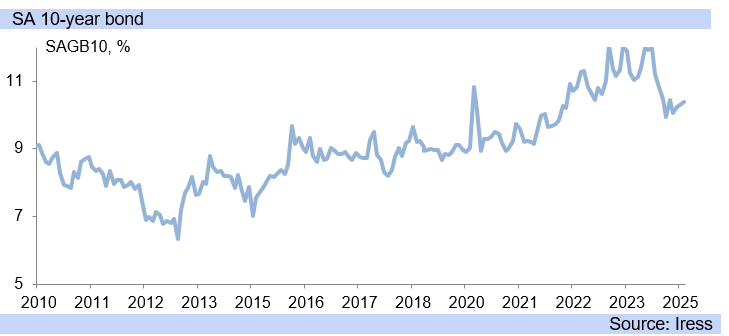

Recent weakness in South Africa’s bond yields could point to fiscal slippage in the country’s upcoming February Budget.

Therefore, Finance Minister Enoch Godongwana faces the challenge of funding government initiatives to invest in economic development and structural reforms while maintaining fiscal discipline.

In 2024, Godongwana announced the government’s plan to tap into the Reserve Bank’s Gold and Foreign Exchange Contingency Reserve Account (GFECRA).

The government drew R150 billion from this account to bolster its ailing finances and curb its debt burden.

Over R100 billion has already been transferred to the National Treasury, with R25 billion to be handed over in the next two financial years.

At the time, this move was praised as a way to slow down the growth rate of the government’s debt and thus provide relief in the form of reduced debt-servicing costs in the future.

However, Investec chief economist Annabel Bishop said in a recent Budget Preview that fiscal slippage has become a general trend in South Africa.

“In most cases, the fiscal metrics deteriorate, with only very occasional improved outlooks, as occurred when savings in the GFECRA account were earmarked last year,” she said.

A worrying sign is that South Africa’s ten-year benchmark government bond yield recently increased from 10.17% in January to 10.42% ahead of the government’s Budget speech.

Bishop explained that South Africa’s bond yields have been historically sensitive to fiscal slippage and increased government borrowing.

The 2023 Medium-Term Budget Policy Statement projected the government’s gross debt to peak at 77.7% of GDP in 2025/26, leading to higher bond yields.

However, the February 2024 budget projections were more optimistic, leading to a recovery in bond yields.

“Projected higher borrowings on weaker GDP really matters, as does an improvement, with the substantial drop in February 2024’s budget projections causing a swift recovery in the ten-year bond yield as forecast supply dropped off,” she explained.

The February 2024 Budget saw gross debt drop back to peak at 75.3% of GDP in 2025/26 and fall to below 70% of GDP by 2030/31, using profits in the GFECRA.

These numbers went up slightly again in the 2024 MTBPS, with gross debt projected to peak at 75.5% of GDP in 2025/26.

Bishop noted that this is still well above a debt ratio of 60% of GDP, considered the maximum sustainable debt ratio for an emerging market economy.

The 2024 MTBPS also showed other signs of fiscal slippage, including higher expenditure and weaker GDP and inflation outcomes.

“With similar occurring for the 2025 Budget on the GDP and inflation front, further fiscal slippage is possible,” Bishop said.

She explained that this would account for the recent weakness in South Africa’s bond yields despite lower inflation and recent interest rate cuts.

“Budget projections matter, particularly gross loan debt, and have a substantial impact on bond yields,” she said.

However, she said there are some signs of recovery, as inflation has fallen significantly, and the Reserve Bank is currently in a cutting cycle that has seen it cut rates by a cumulative 75 basis points so far.

In addition, the World Bank has raised South Africa’s GDP growth forecast for 2025 to 1.8% and forecasts 1.9% for 2026.

This is largely due to improving energy availability and further reforms in the transport sector.

“During this period, inflation is expected to remain under control, allowing a further easing of monetary policy that will encourage banks’ credits to businesses and households and, thus, stimulate economic growth,” the World Bank said.

“Such recovery, albeit modest, will be driven by improved infrastructure services and a relatively favourable external environment”.

The bank said South Africa’s fiscal policy is anticipated to remain prudent, with the government aiming to stabilise the public debt-to-GDP ratio by 2026.

“This requires the containment of pressures to raise expenditures, such as those related to the government wage bill, support for state-owned enterprises, and unfunded healthcare reforms,” it said.

However, it also warned that a 1% increase in GDP growth is expected to generate only 30,000 to 50,000 jobs due to the low employment elasticity to GDP growth in South Africa.

Therefore, the country’s poverty and unemployment rates are projected to remain high over the next few years.

The bank said economic growth of 5% to 6% a year is needed to fix these problems, but difficult to achieve in the short term.

“The structural constraints that continue to impede the development of the private sector and the need for fiscal consolidation,” it said.

Comments