Tax cuts for the rich will help South Africa

A new study has revealed that when taxes are raised on the wealthy in South Africa, tax income declines at a higher rate than this tax increase. Therefore, lower rates for the rich could bolster the country’s tax revenue.

This was revealed in a study by the organisation Southern Africa—Towards Inclusive Economic Development (SA-TIED), which analysed a phenomenon called “tax elasticity” in South Africa.

Tax elasticity refers to changes in tax revenue in response to changes in tax rates. In other words, it is the degree to which an increase in the tax rate causes a change in the tax base.

A 2021 study published in The Economic Journal performed a meta-analysis of this phenomenon by looking at the elasticity of taxable income (ETI).

ETI measures the relative change in reported taxable income in response to a 1% change in the marginal net-of-tax rate.

The study performed a meta-analysis of 61 studies and more than 1,700 ETI estimates, which puts ETI at 0.4. It implies that if the net-of-tax rate decreases by 10%, the reported taxable income drops by 4%.

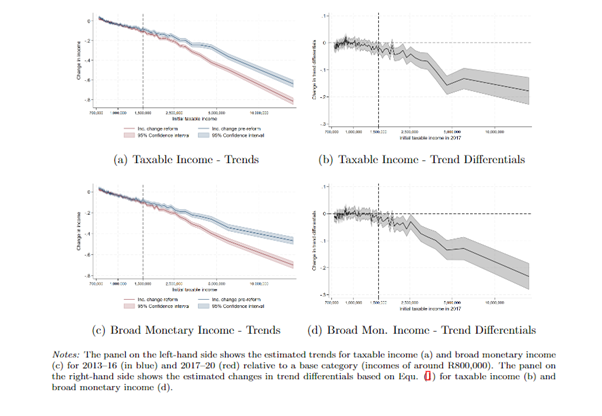

However, SA-TIED examined South Africa’s ETI by looking at the effect of the country’s personal income tax increase a few years ago.

In 2017, South Africa raised the top marginal tax rate for annual incomes exceeding R1.5 million from 41% to 45%. This change affected the country’s top 0.6% of earners.

“Based on the relatively strong implementation of the reform and the received wisdom about how the tax base influences taxpayer behaviour, one might have been optimistic that the South African income tax increase would help the country improve revenues and reduce income inequality,” they said.

However, they found that, after the reform, the income reported by top-income earners above the threshold dropped sharply.

It declined so much that revenues collected on personal incomes above the R1.5 million threshold were less than they would have been without the reform.

“Our estimates for South Africa translate into high tax elasticities, both before and after deductions, well above 1,” the organisation said.

These findings can be seen in the graph below, courtesy of SA-TIED.

They explained that these ETIs are substantially higher than the ‘consensus’ estimates derived from existing work, i.e., the mean estimates of earlier research focusing on higher-income countries.

“In fact, these ETIs are so large that they put the South African top tax rate on the wrong side of the so-called Laffer curve maximum,” they said.

“This means that tax revenues collected from the high-earner group declined when top tax rates increased.”

The Laffer curve is an economic principle that illustrates a theoretical relationship between the taxation rates in a country and how that affects a government’s tax revenue.

Simply put, the Laffer curve suggests that if tax rates are increased above a certain level, tax revenue can fall.

This is because taxes above a certain level could discourage people from working, resulting in lower consumption expenditure levels and encouraging companies to move to other countries.

Efficient Group chief economist Dawie Roodt has also explained that higher tax rates incentivize people to find ways to minimise their tax bill, especially higher income earners who have the resources to reduce their tax burden.

“How rate increases influence revenues depends on how taxpayers’ behaviour responds and, of course, also on how broad the tax base is,” SA-TIED explained.

“In South Africa, it is very broad. It lacks many common international deductions like those for children, student loan interest, or mortgage interest, which people may exploit to reduce their tax bill.”

“Public finance analysts commonly expect that, in income tax systems with broad tax bases, opportunities for tax avoidance are kept at bay, and rate increases should therefore increase revenue.”

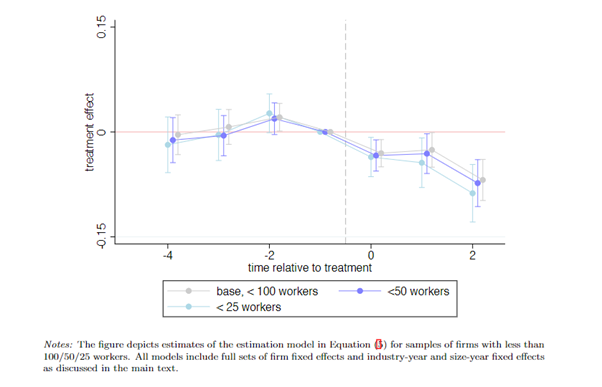

SA-TIED also analysed what drove the drastic reductions in reported income following the tax hike by examining which income components saw the largest reductions.

They found that while normal monthly earnings did not decline, bonus payments, fringe benefits, investment income, and allowances – significant for high earners – sank strongly.

They also checked whether top earners completely disappeared from the tax net after the reform – by emigrating, for example – but found no indication of this.

“To understand the broader implications for the South African economy, we were curious to know if these impacts were due to tax evasion, reduced work effort by high-income earners, or other factors,” they said.

“We looked at the output of companies with employees affected by the tax increase. Compared to similar non-affected companies, the affected companies saw reduced sales and value added.”

“This suggests that the reform impacted companies’ economic performance and that tax reporting behaviour alone does not fully explain the response.”

This effect can be seen in the graph below, courtesy of SA-TIED.

“Our research shows that when you tax the incomes of the rich in lower-income countries, like South Africa, this can be counterproductive even when design and implementation are done well,” the organisation said.

“We found that while some wealthy individuals may use tax planning to reduce their tax burden, this isn’t the only issue.”

They explained that high income taxes could also negatively impact the performance of companies.

“These findings highlight the need for tax authorities to carefully analyse the impact of tax reforms and continue to calibrate tax policy,” they said.

Comments