South Africans are gambling away their retirement savings

In a recent survey, 50% of respondents reported spending money on gambling, betting, or lottery activities in the last three months.

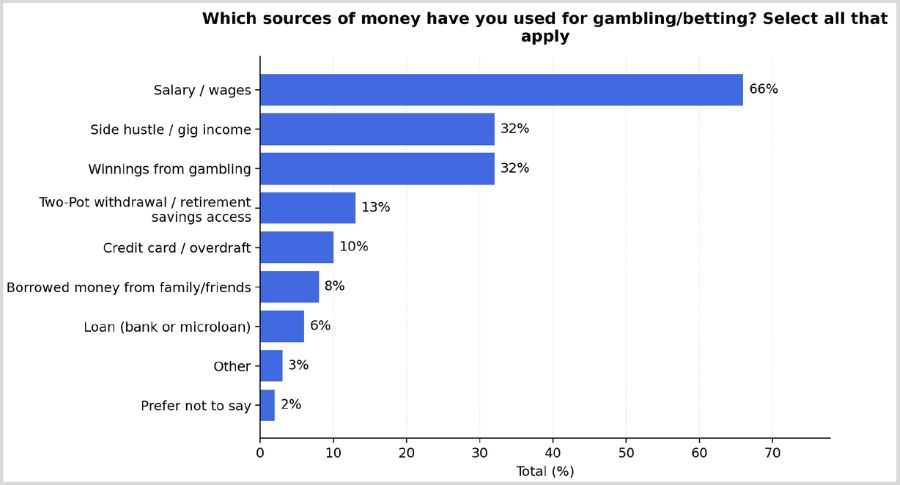

Of these, 66% reported using their salary and wages to fund these activities, with 13% saying they accessed retirement savings to fund their gambling and betting activities.

This was revealed in the 2026 Sanlam Benchmark Survey, which shed light on South Africa’s growing gambling problem.

The Sanlam Benchmark is the country’s most comprehensive retirement fund industry research.

For this study, Sanlam surveyed 76 standalone funds, 130 umbrella fund employers, 30 pensioners who retired four to five years ago, and 600 consumers who are nearing or in retirement.

This year, part of the survey focused on how South Africans spend money on gambling and other related activities.

This comes amid a boom in online betting. According to the National Gambling Board, South Africa saw R1.5 trillion gambling turnover in the 2024/25 financial year, up from R1.1 trillion the prior year.

Betting, which includes online betting, generated R52.3 billion of this total, while casinos contributed R16.6 billion, or 22% of the total.

Sanlam’s survey showed how this data plays out in practice, with 50% of respondents in the online consumer portion of the study having spent money on gambling, betting, or lottery activities in the last three months.

Sanlam Umbrella Solutions managing executive Nzwa Shoniwa explained that participation in these activities is notably higher among those still economically active.

This is especially the case for the more frequent, more digital, and potentially riskier forms of gambling.

“Retirees are not untouched, but the intensity is lower. The bigger risk is the pre-retirement habit that chips away at financial resilience over time,” he said.

He explained that, among working South Africans, gambling is more closely tied to cash-flow pressure. In contrast, among retirees, it is more often seen as a possible income top-up.

“In both cases, gambling starts to move away from recreation and closer to coping,” Shoniwa said.

South Africans gambling frequently

Sanlam’s survey found that roughly 72% of those who gamble spend money on the lotto and scratch cards.

However, online gambling is becoming a growing concern, with online sports betting and casino gambling now accounting for more than a third of activity each.

“That matters because these formats make repeated spending easier, quicker, and less visible,” Shoniwa explained.

“Working South Africans are more likely to be in the higher- frequency online space, where small, regular spending can quietly crowd out saving over time.”

A third of survey respondents reported gambling a few times a month, with weekly or near-weekly participation also significant among people who are not yet retired.

Shoniwa warned that, in a low-savings environment like South Africa, modest but repeated spending can do real damage over time.

He said the real financial risk lies in “small regular leaks”, which refer to modest but consistent spending that gradually crowds out savings.

“In an environment where many households already face budget pressure, repeated discretionary spend, even at low levels, can accumulate into meaningful long-term financial erosion,” he said.

Shoniwa said the source of gambling funds is “perhaps the most sobering” part of the survey’s findings.

Two-thirds of respondents said they use their salary or wages to gamble, with some also drawing on side-hustle income, credit, borrowed money, and even two-pot retirement withdrawals.

“That should immediately reframe the conversation: this is not only leisure spend, but money that might otherwise support financial resilience,” he said.

South Africans can’t afford to retire comfortably

This comes amid a backdrop of severe financial strain in South Africa, with more than 80% of survey respondents saying they were experiencing financial stress.

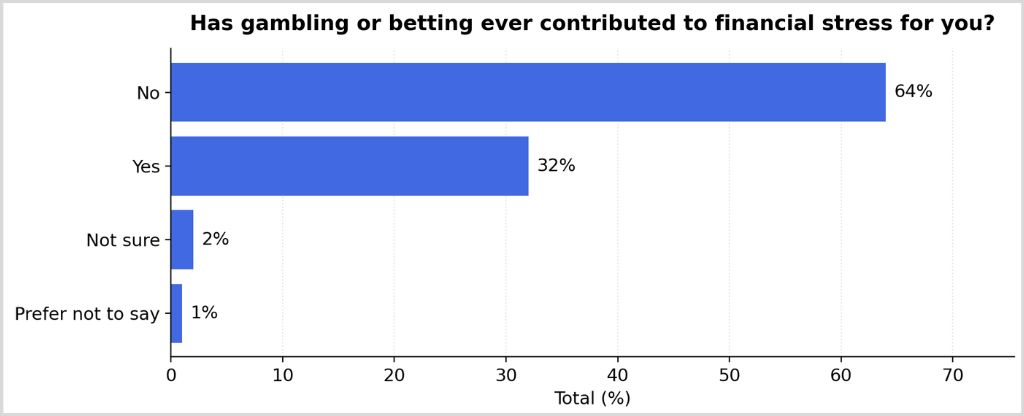

In addition, 32% of respondents said gambling has contributed to financial stress. “That is a sizeable minority, and in some cases an early warning sign of deeper financial vulnerability,” Shoniwa said.

Sanlam’s survey also found that 49% of respondents worry about not having enough income to maintain a comfortable lifestyle in retirement.

This concern is backed up by further data, with Sanlam finding that pensioners who take a cash lump sum at retirement now deplete it within an average of just 14.6 months.

This marks a significant decline from the 30 months reported between 2011 and 2016.

In addition, the survey showed that 75% of pensioners cut expenses, including groceries, home maintenance, and downgrades or cancellations of medical aid.

A further 47% report that they are still paying off debt in retirement, with only 20% of those surveyed completely debt‑free. The majority carry store accounts, credit cards, vehicle finance, or mortgages.

These financial pressures have led many South Africans to delay retirement, with only 40% of pensioners retiring at the prescribed retirement age.

Concerningly, 58% of retirees said they feel worse off than two years ago, while around half cannot maintain their pre‑retirement lifestyle four to five years into retirement.

Comments