Major international bank backs South Africa to go from zero to hero

Bank of America (BofA) analyst Tatonga Rusike believes South Africa is not only on track to receive another credit rating upgrade in 2026 but also forecasts a return to investment grade for the local currency in the next five years.

However, much will depend on the strength of ongoing reform efforts and South Africa’s upcoming 2026 Budget, with rating agencies hoping to see state debt stabilise or near stabilisation.

In addition, South Africa’s state-owned enterprises (SOEs), particularly Eskom and Transnet, must remain or become self-reliant and not depend on the state for funding.

In a recent Bank of America Securities report, Rusike explained that a sovereign ratings upturn could be on the horizon for South Africa.

This comes after S&P Global upgraded the country’s credit rating for the first time in over two decades in 2025 on the back of South Africa’s fiscal consolidation efforts and ongoing reforms.

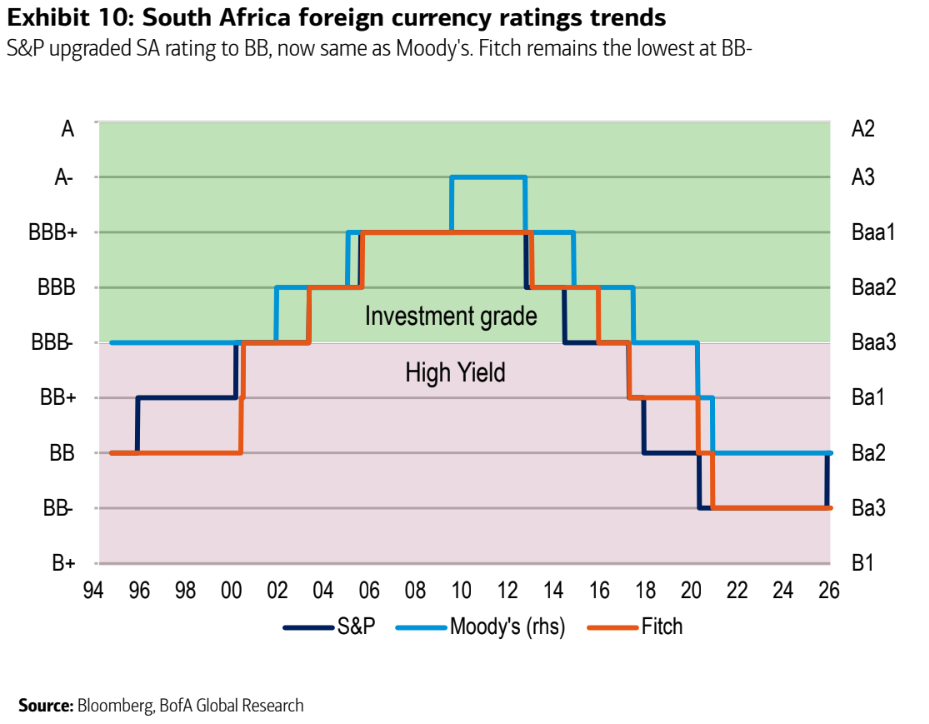

S&P upgraded South Africa to BB in November 2025 after a wave of downgrades between 2012 and 2020. While still in so-called “junk status”, this was seen as a positive affirmation of the country’s turnaround efforts.

Currently, South Africa is rated lowest by rating agency Fitch at BB-/stable, followed by Moody’s at Ba2/stable, and S&P has the highest rating of BB/positive.

Rusike said BofA’s base view expects that, by the end of 2026, South Africa’s sovereign ratings could be BB+/stable from S&P, with the local currency back at investment grade BB-.

Regarding other rating agencies, Rudike expects South Africa to attain a BB/stable rating from Fitch and a BB/positive rating from Moody’s by the end of this year.

While these ratings will keep South Africa in “junk status”, they put the country on track to return to investment grade within the next decade, if it can stay the course with current reforms.

All eyes on South Africa

Rusike attributed S&P’s rating upgrade for South Africa to several changes over the past few years, including –

- The GNU is solving South Africa’s electricity problems

- An improving economic outlook, thanks to domestic improvements

- A lower inflation target and domestic rate-cutting cycle, reducing borrowing costs

- Moderating SOE risks with Eskom turning a profit, while the utility’s bailout package from the National Treasury is almost complete

- Logistics reforms, though this is still a work in progress

- Positive global spin-offs, such as higher commodity prices, a global rate-cutting cycle, a weaker US dollar, etc. He noted that these are both cyclical and structural in nature.

“Either way, fiscal improves as tax revenues outperform, helping debt to GDP to stabilise and start a downward trend,” Rusike said.

However, he noted that all rating methodologies pull South Africa’s rating down by at least one notch due to weaknesses in its economy and/or public finances.

Therefore, South Africa’s upcoming 2026 Budget, set to be presented by Finance Minister Enoch Godongwana on 25 February 2026, will play a critical role in any potential future rating movements.

Rusike explained that this Budget will be to convincing Fitch and Moody’s whether to take positive action, potentially following in S&P’s footsteps to bring South Africa’s rating up to BB.

Luckily, he said that, given that S&P kept South Africa on a positive outlook after the rating upgrade in 2025, “we think it is likely that it will upgrade”.

It should be noted that Fitch commented positively after South Africa’s Medium-Term Budget Policy Statement was presented in November 2025, although its last rating action was in September 2025.

Despite keeping South Africa’s rating unchanged and maintaining a stable outlook, Fitch noted several improvements in the country’s economy that could tip the scales toward a future rating upgrade.

For example, the agency upped its GDP growth forecasts for South Africa to 1.4% in 2026 and 1.5% in 2027.

In addition, the firm said that while South Africa’s debt continues to rise, it is moving more slowly than in previous years.

It noted that SOE risks have also moderated, and the agency no longer assumes that Eskom’s debt will be absorbed by the government.

However, it raised the alarm about Transnet, which continues to use government guarantees to borrow.

“Getting close to debt stabilisation could trigger a positive rating action from Fitch. In our view, 2026 could be a turning point for public finances,” Rusike said.

Stabilising South Africa’s debt-to-GDP ratio will be a strong sign that fiscal reforms are bearing fruit, with Rusike saying the 2026 Budget needs to deliver on the following key elements –

- A headline main budget balance of less than 4% of GDP over 2026 to 2029, maintaining primary surpluses at close to 2% of GDP

- No material new support for SOEs that could change the fiscal framework. Eskom support needs to wind down as planned.

Overall, Rusike said South Africa’s return to investment grade looks like a remote possibility.

“In our view, returning to investment grade would be difficult in the near term. However, rating upgrades may start looking feasible next year,” he said.

“Our best-case scenario would be two-notch upgrades at Fitch and S&P and one notch at Moody’s within 3 to 4 years, taking us to the 2029 election.”

“Another smooth transition in 2029 could strengthen governance and reform momentum, laying the path for a return to investment grade.”

Comments