Back to the future for the South African rand

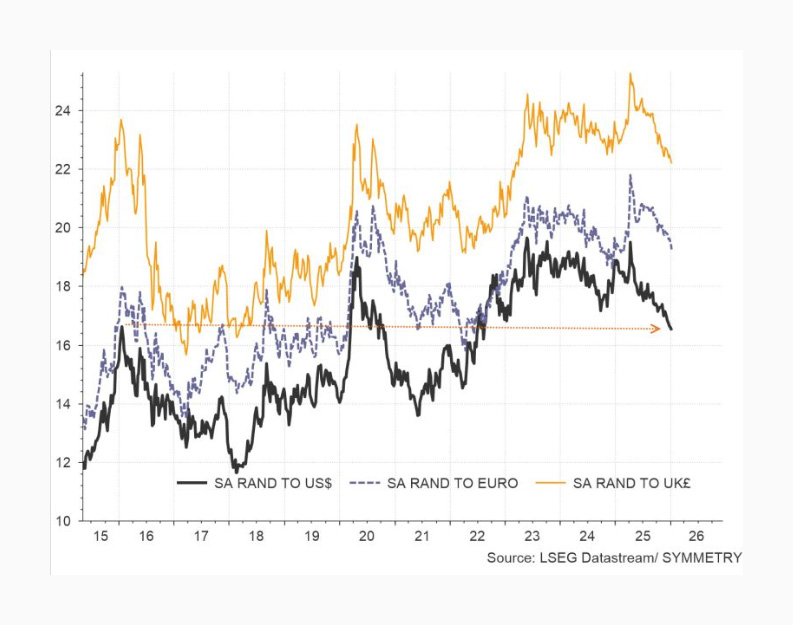

The South African rand is back to where it was ten years ago, when it also traded at around R16.40 to the US dollar.

What was then seen as a disorderly weakening of the currency due to South Africa slipping into sub-investment grade or junk status is now seen as a symbol of rand strength.

For Symmetry chief investment strategist Izak Odendaal, this shows the mistake of projecting weakness or strength indefinitely, which many have done.

A decade ago, Odendaal explained, the rand was particularly weak in the aftermath of the Global Financial Crisis, and the impact of state capture and excessive government spending was becoming apparent.

South Africa’s economy was slowing after a decade of strong growth, while government spending was ramping up.

This saw public debt surge, with credit ratings agencies taking notice and steadily downgrading South Africa to junk status. As a result, capital flowed out of the country, further stalling growth and weakening state finances.

At this point in time, Odendaal said it would have been easy to project the rand’s weakness forward forever. This was expected to occur at a steady rate of around 5% per annum versus the dollar.

Odendaal said that such projections were commonplace, with South Africa appearing to be on a path to financial and economic ruin.

While the country’s fortunes have not completely reversed, there are positive signs that the tide is beginning to turn with regard to public finances and economic growth.

The government’s debt burden is expected to peak as a share of GDP in the current financial year and steadily decline, with fixed investment set to rise and drive growth higher.

While this has bolstered the rand, the currency’s appreciation has largely been a result of dollar weakness and surging commodity prices.

In particular, precious metals prices have surged as investors search for safety amid heightened volatility. As these are South Africa’s most valuable exports, this has widened the country’s trade surplus and boosted the rand.

This is a common trend for the rand, with the currency’s rises and falls historically aligned to commodity prices. It is also a proxy for sentiment towards emerging markets due to the country’s relatively deep capital markets for a developing economy.

The graph below shows the performance of the rand versus the dollar, euro, and pound over the past decade, with the local currency effectively being back where it was.

Dollar weakness

The main story of 2025 with regard to the rand was the dollar’s sustained weakness, despite economists and analysts predicting a surge in the greenback’s strength.

President Trump’s America First policies were broadly expected to boost the dollar as they had in his first stint in the Oval Office.

However, the combination of the beginnings of a boom in key commodities and concerns about the United States’ financial health and Trump’s unconventional trade policy saw capital flow elsewhere.

The dollar has suffered periods of weakness in the past, typically driven by short-term cyclical factors such as a commodity boom and momentary interest rate differentials.

However, this time around, the dollar’s weakness appears to have been driven by large-scale currency hedging, as investors have not sold out of US assets in meaningful amounts, Odendaal explained.

This suggests that the dollar’s weakness may be more fundamental, with 2025 marking the start of a decline for the greenback that will unfold over several decades.

Trump’s policies were largely expected to result in higher interest rates in the US and thus, a stronger dollar.

The policies of reshoring manufacturing, elevated tariffs, and renewed tax cuts resulted in economists predicting elevated inflation in the world’s largest economy.

While some of these policies have only come into effect as of 1 January 2026, inflation has not only moderated in the US but also declined towards the end of 2025, contributing to the Federal Reserve cutting interest rates throughout 2025.

This has been coupled with increased investor uncertainty regarding the financial health of the United States government, with its debt continuing to soar.

As a result, 2025 was one of the worst years for the trade-weighted dollar index in the last five decades, Odendaal said.

This was not because global investors sold out of US assets, with significant capital still being poured into American equities amid optimism regarding artificial intelligence.

Rather, Odendaal explained, it appears that for the first time in 15 years, large-scale currency hedging drove the dollar lower.

This indicates a shift in investors’ perception of the security of capital in the United States, with many thinking that inflation will be higher for longer in the future to inflate away the country’s debt.

Odendaal said interest rate differentials will probably play a bigger role in the future, with investors hunting for yield and security.

Trump’s repeated attacks on the Federal Reserve and its chairman, Jerome Powell, have only heightened investor caution and accelerated the search for safe-haven assets.

The graphic below, courtesy of Old Mutual Investment Group, shows the various factors underpinning US exceptionalism and a strong dollar. These factors are being steadily eroded.

Comments