The end of a devastating era in South Africa

S&P Global’s recent decision to upgrade South Africa’s foreign and local currency ratings signals the end of a devastating era of economic stagnation.

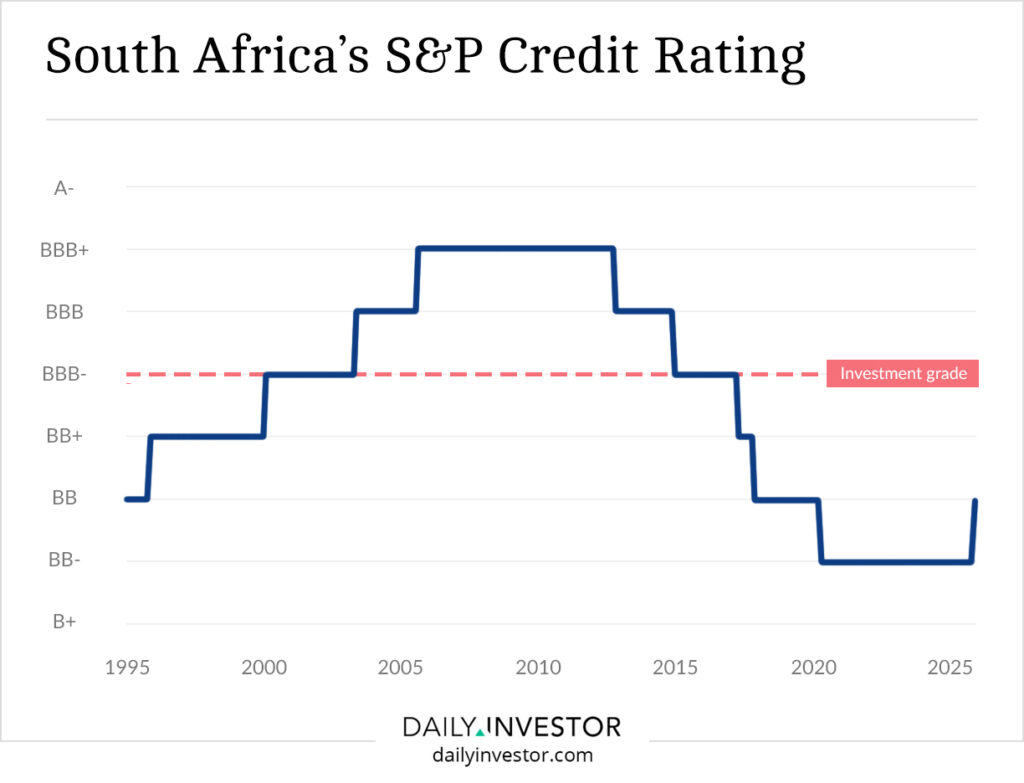

On Friday, 14 November 2025, S&P Global raised South Africa’s foreign currency rating to BB and its local currency rating to BB+, with a positive outlook.

The ratings agency said it expects South Africa’s real GDP (gross domestic product) growth to rise to 1.1% in 2025.

It further expects the country’s economic growth to average 1.5% between 2026 and 2028, as reforms to the electricity sector and other key areas support growth.

In the first half of the financial year ending March 31, 2026, South Africa’s fiscal revenue outperformed budgeted targets.

“We expect the government to post its third successive year of primary surpluses,” S&P Global said in a statement.

“Given improving tax collections and expenditure constraints, we expect fiscal consolidation to continue through to fiscal 2028.”

It added that contingent liabilities will ease as state-owned enterprises (SOEs) are likely to require less financial support in the future.

Given these factors, it upgraded South Africa’s foreign and local currency long-term sovereign credit ratings with a positive outlook.

The positive outlook reflects the potential for further improvements in fiscal metrics and stabilisation of government debt.

This positive outlook is contingent on South Africa’s coalition government continuing its fiscal consolidation.

“The outlook also reflects the possibility of stronger growth than we currently expect, despite trade- and tariff-related headwinds,” it said.

It said this growth relies on the authorities accelerating economic reforms while addressing infrastructure pressures.

The end of a devastating era in South Africa

This is the first time in two decades that S&P Global has upgraded South Africa’s foreign and local currency long-term sovereign credit ratings.

Between 1994 and 2007, the administrations of Nelson Mandela and Thabo Mbeki did an excellent job of improving the country’s financial position.

During this period, S&P Global upgraded South Africa’s credit rating numerous times from BB to BBB+.

However, under the Jacob Zuma administration, South Africa’s economic growth stalled, and the country began to run significant deficits.

In 2008/09, South Africa’s gross loan debt totalled R627 billion, equivalent to 26% of the country’s gross domestic product (GDP).

Over the next fifteen years, under Zuma and Ramaphosa, the government’s gross loan debt ballooned to R5.21 trillion, or 73.9% of GDP.

However, over the last few quarters, South Africa started to run primary surpluses, which signals more responsible spending by the state.

Finance Minister Enoch Godongwana said in his mid-term budget that South Africa’s debt-to-gross domestic product ratio will stabilise at 77.9% in the current fiscal year.

“This is the first time since the 2008 financial crisis that public debt will not grow as a percentage of GDP,” he said.

He explained that spending has consistently exceeded revenue since 2008. This drove up debt and debt-service costs.

The debt servicing costs are now so high that the government has had to cut spending on essential services, such as education and security.

However, the good news is that South Africa is turning the situation around, which will put the country on a much better trajectory.

This will bring an end to the devastating period, which started under Zuma, and which was characterised by slow economic growth and rising debt.

South Africa’s S&P Global credit rating

The chart below shows South Africa’s S&P Global credit rating from 1994 until the latest upgrade this month.

Comments