South Africa at breaking point

South Africa’s financial health is at a breaking point, with the current debt load being unsustainable even if the National Treasury manages to stabilise it at 77% of GDP.

More concerningly, with the debt load at this level, the government can no longer borrow more to finance its expenditure. If it wants to spend more, it will have to raise taxes.

The government will have to spend more, eventually, to boost economic growth to levels where unemployment can be addressed sufficiently.

It is crucial that this increased spending comes off a sound fiscal base, with a stable debt load, and not in an environment where debt is rising uncontrollably.

This is feedback from Investec’s economics unit in its preview for the Medium-Term Budget Policy Statement (MTBPS) on Wednesday, 10 November.

Investec chief economist Annabel Bishop explained that Finance Minister Enoch Godongwana’s task is made much more difficult by the historic failure of South Africa’s government to stabilise its debt.

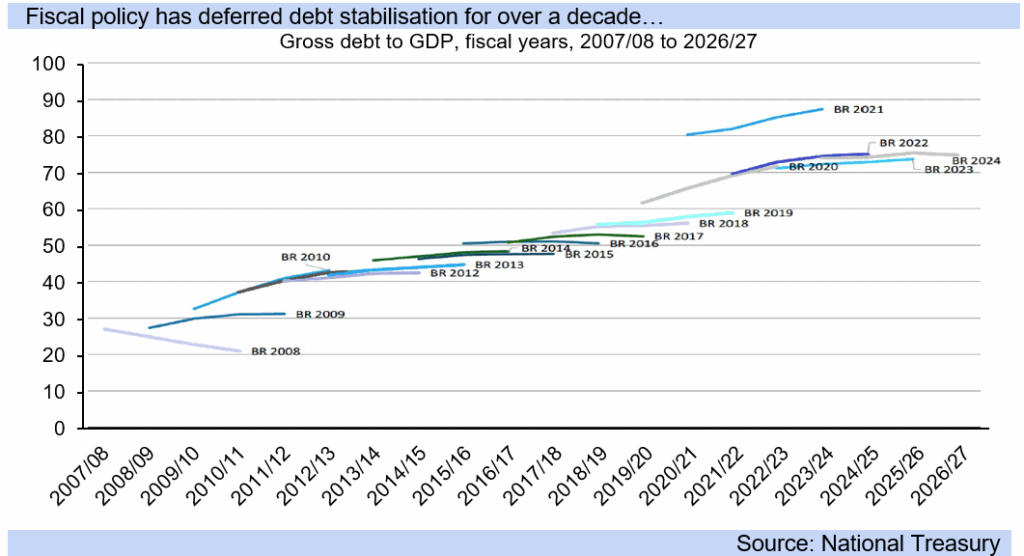

The government has repeatedly forecast a stabilisation in the debt load since 2009, which it has failed to achieve, resulting in its debt growing to unsustainable levels.

As a result, there are always questions about whether this time the National Treasury will be able to impose the limits on spending growth needed to stabilise the debt as a share of GDP.

“We have had many years of fiscal slippage. The National Treasury has repeatedly put out a certain set of projections for South Africa’s debt-to-GDP ratios, and they have not been met and have been revised higher,” Bishop said.

“This has provided an issue where there are expectations of continued fiscal slippage, with most questions surrounding differences in GDP growth forecasts.”

However, even if the government does manage to stabilise its debt burden in the current financial year, it will still be at unsustainable levels.

“Overall, at 77% of GDP, South Africa’s debt ratio is still not a sustainable ratio for an emerging market, that is broadly seen as being 60% or less,” Bishop said.

This debt ratio is even higher when the government guarantees the debt of public companies and municipalities. That debt, in time, is likely to be taken onto the government’s balance sheet, putting it in a worse financial position.

South Africa’s 15 years of fiscal slippage can be seen in the graph below, courtesy of Bishop and Investec.

Unsustainable debt repayments

What makes the debt burden particularly unsustainable for South Africa is the country’s cost of servicing these liabilities, with it spending over R1 billion a day in interest payments.

While there is much positivity surrounding South Africa’s financial position at the end of the current financial year, some have urged caution as the country’s economy is not growing fast enough to sustain the state’s debt burden.

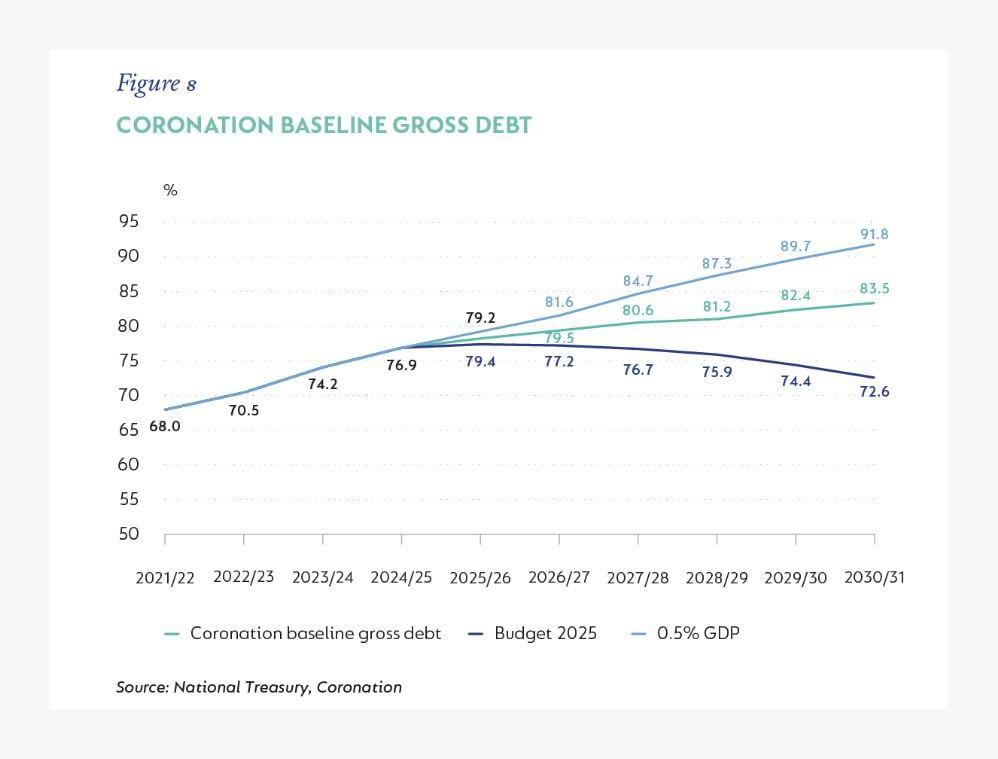

In an analysis of South Africa’s long-standing economic challenges, Coronation explained that its baseline shows the country’s debt-to-GDP ratio will continue growing into the 2030s at current economic growth rates.

This would be catastrophic for the country, with the Reserve Bank warning that even at current levels, South Africa is at risk of entering a debt trap.

South Africa is already in an unsustainable financial situation, as the interest rates owed on government debt are higher than the country’s nominal economic growth.

This means that South Africa’s debt-servicing costs are compounding at a faster rate than the country’s economy, making it unsustainable over the long run.

Debt-servicing costs already amount to over R1.2 billion a day for the government, crowding out spending in other areas of the economy, including education and healthcare.

These costs are on track to take over social grant payments in the coming three years, according to the National Treasury.

While others are positive regarding the potential to stabilise South Africa’s debt burden, Coronation is more cautious in its analysis.

“If growth remains in the painfully weak 0.5% to 1% range, current fiscal allocations, even with tough consolidation and a rising primary surplus, will not be sufficient to stabilise the debt trajectory,” it said.

“Debt continues to rise relative to GDP, crowding out investment, raising borrowing costs, and diverting resources away from social and capital spending.”

Each postponement in the stabilisation of the government’s debt burden has resulted in it accumulating at a faster rate than initially expected.

While the National Treasury remains committed to its policy of fiscal consolidation by financing new expenditure through revenue increases, there is often a crucial mismatch.

The increased expenditure tends to be recurring and fixed, implying any fall-off in growth and thus tax revenue will create a large funding shortfall.

This increases the risks of a higher debt load and results in the government taking on new expenditure projects that it cannot finance in the long run.

Comments