Rising electricity prices threaten Reserve Bank interest rate cuts

Electricity and water price inflation continue to put significant upward pressure on South Africa’s inflation rate.

Since 2009, electricity prices have jumped by more than 600% and water prices have soared by over 500%, significantly more than CPI inflation over the same period.

This not only makes it far more difficult for the Reserve Bank to manage the country’s inflation but also puts pressure on its plans to lower and narrow the country’s inflation target.

In the Reserve Bank’s latest Monetary Policy Review, the central bank outlined how administered price inflation impacts the country’s overall inflation.

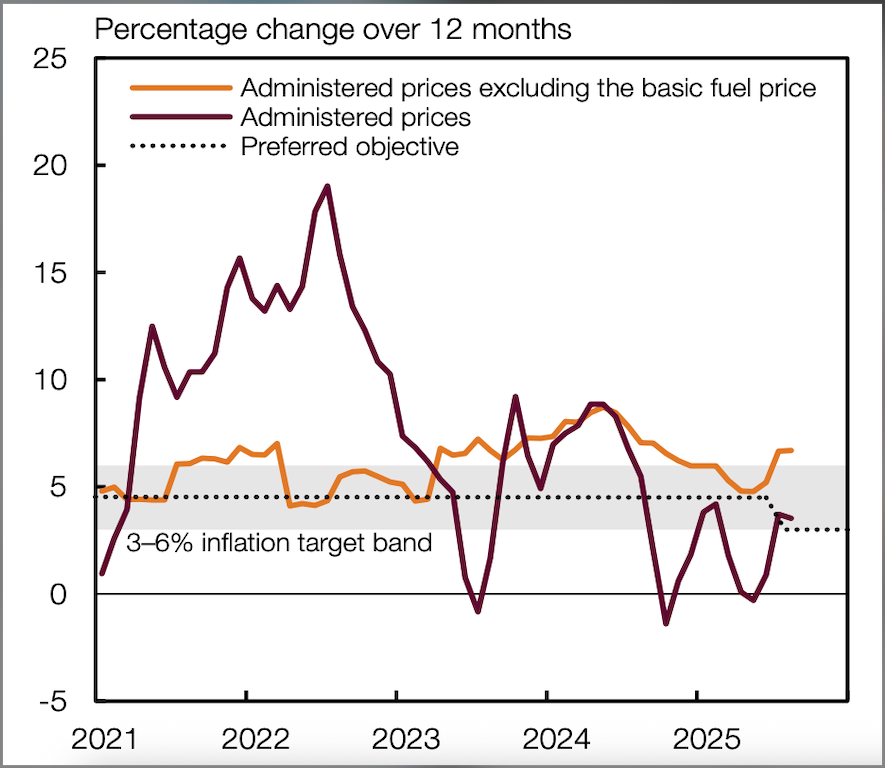

The administered price basket consists of the prices of goods and services that are set by the government and other official bodies, including fuel, electricity and water.

The fuel price differs from electricity and water prices in the sense that it is determined by factors both within and outside the government’s control, i.e. regulated and unregulated factors.

Fuel price inflation is driven by the basic fuel prices, which is based on international oil prices, and adjustments to fuel taxes and the Road Accident Fund levy, which the government determines.

The Brent crude oil price has remained relatively stable since April this year, driven by ample supply and subdued demand.

Combined with a relatively stable and strong rand in 2025 to date, South Africa’s fuel prices have been stable, with most of its movements driven by base effects.

The Reserve Bank explained that this proved positive for administered price inflation, dragging it lower to average 1.6%.

However, when excluding the basic fuel price, administered price inflation averaged 5.6% between April and October 2025.

This means that electricity and water price inflation remain the primary sources of upward pressure in the administered price basket.

The Reserve Bank pointed out that, since 2009, electricity prices have risen by more than 600% while water prices are up over 500%.

This is considerably faster than the growth seen in consumer prices, which have roughly doubled since 2009.

The impact of the far above-inflation increases in water and electricity prices on administered price inflation can be seen in the graph below.

Targeting inflation

The Reserve Bank explained that this trend is set to continue, with price increases of 10.4% for electricity and 12% for water announced in August 2025.

This means that these components will average around 10% in 2025, compared to a projected headline inflation of 3.4%.

The central bank said that with headline inflation hovering around the 3% target it is aiming for, large increases in administered prices are becoming more difficult to justify.

It said this calls for urgent policy measures to align increases in electricity and water prices with broader price trends in the economy.

“Low headline inflation also contributes to moderations in administered price inflation through partial indexation,” the Reserve Bank added.

Therefore, keeping inflation low and anchored around the Reserve Bank’s target will also benefit administered prices with components that are influenced by the headline inflation rate.

However, the Reserve Bank’s task of keeping inflation low and on target is made significantly more difficult by these exorbitant administered price increases.

In addition, if inflation strays too far from the Reserve Bank’s new preferred target of 3%, the short-term pain that is expected to come from officially lowering the inflation target becomes increasingly risky.

The Reserve Bank and National Treasury have been in talks to lower and narrow the country’s official inflation target for months.

The central bank and other proponents of a target change believe this could hold immense benefits for the country, including lower inflation and interest rates over the long term.

Lowering the target will also bring South Africa more in line with its global peers, enhancing the country’s export competitiveness, and could alleviate the government’s heavy debt servicing burden.

However, these benefits will come with some short-term pain, including impacting the country’s already weak growth and increasing pressure on households with debt.

This is because, in order for inflation to settle around the new, lower target, interest rates may need to be higher for longer.

Therefore, economists have warned that the government has a very narrow window to change the inflation target while minimising the impact of these short-term risks.

As South Africa’s inflation keeps inching higher, with CPI reaching 3.4% in the latest inflation print for September, this window is steadily closing.

Standard Bank chief economist Goolam Ballim told Daily Investor about this narrow window as early as July of this year.

“I would be inclined to argue that we have a window of opportunity that is going to close soon for lowering the inflation target without much negative impact,” Ballim said.

“If the target were lowered now, the impact of the shift of expectations towards the new target would be very, very small because of the low level of inflation.”

“If the target is calibrated to a 3% point, for instance, right now, the inflation expectations adjustment would be bearable.”

“If inflation expectations adjust quickly, it means the Reserve Bank will not need to employ a tighter monetary policy than otherwise to reach the target, thus minimising the impact on growth.”

The National Treasury, which sets South Africa’s inflation target, has yet to announce an official change, with many expecting Finance Minister Enoch Godongwana to address it in his Medium-Term Budget Policy Statement on 12 November.

Comments