South Africa running out of time

The government’s efforts to halt the decline of its financial health are running into an immovable obstacle – the South African economy. Without faster growth, these efforts are unlikely to succeed.

National Treasury’s policy of fiscal consolidation has begun to bear fruit, with South Africa running consecutive primary budget surpluses.

However, this alone will not resolve South Africa’s fiscal challenges and will take years to stabilise the government’s debt – something which has been promised for over a decade.

That said, South Africa is one of the few countries that is trying to get its fiscal house in order, chief investment strategist at Old Mutual’s Symmetry, Izak Odendaal, said.

Efforts to tighten belts have just led to the collapse of France’s government, and the appointment of the fourth prime minister in 12 months.

In the US, fiscal discipline has gone out the window, though tariffs are bringing in additional tax revenue. If tariffs are partially blocked by the Supreme Court, it will bring relief to businesses and consumers but further widen the deficit.

At the same time, fiscal consolidation cannot rely on cost-cutting or tax rate hikes alone, since both are politically unpopular and weigh on the economy, Odendaal said.

Improved efficiency at SARS will also only go so far. Faster economic growth is needed to raise tax revenues organically and painlessly.

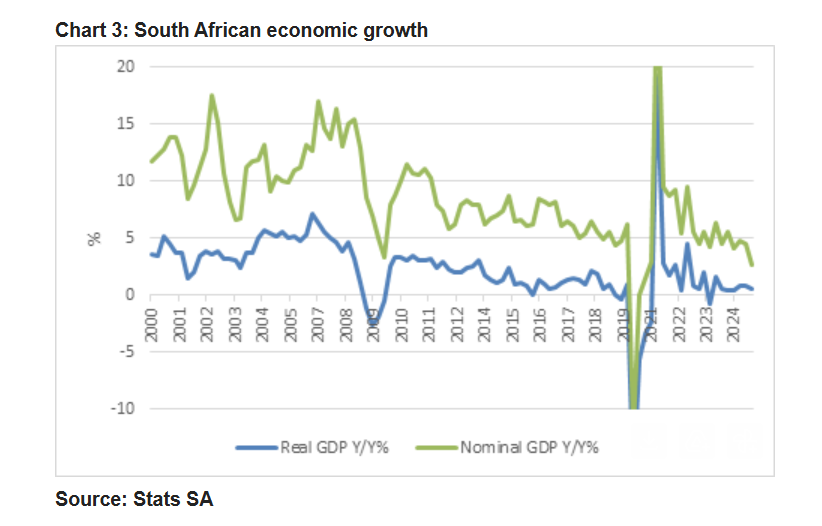

The news on this score is mixed. After basically flatlining in the first quarter, real gross domestic product growth picked up to 0.8% in the second quarter.

This is better, but not good. In real terms, the economy was only 0.6% larger compared to a year ago in the second quarter.

Notably, from the government’s point of view, nominal growth – i.e., adding back inflation – was only 2.5% year-on-year.

This is essentially broad income growth in the economy that the government taxes, and this number must rise for tax revenues to grow organically.

South Africa’s nominal GDP growth rate is currently below the interest rate it pays on government debt, which is just below 10%.

This means the country is still on an unsustainable debt path, with it likely to hit a fiscal cliff if it does not increase economic growth.

South Africa’s nominal and real GDP growth can be seen in the graph below, courtesy of Odendaal.

South Africa’s problems run deep

South Africa’s economic challenges are different to what is typically seen in a modern economy, with its problems lying clearly on the supply side of the economy rather than demand.

The country’s GDP deflator – a broad inflation measure that cuts producers and consumers – was only 1.4% year-on-year in the second quarter, the lowest rate since the 1970s.

While probably a cyclical low point, it suggests that maintaining a 3% inflation target is not that far-fetched, Odendaal said.

Nonetheless, the Reserve Bank will not cut rates further until it is confident that inflation and inflation expectations will hover around 3%. Several commentators have argued that it should rather be cutting rates aggressively now to boost the economy.

Odendaal explained that it would make sense if the biggest problem were a lack of demand, instead of supply-side challenges.

However, demand seems to be improving modestly already. Consumer spending rose almost 3% year-on-year in the second quarter in real terms.

Furthermore, credit growth seems to have bottomed, suggesting that interest rates, while elevated, are not crushing consumer demand.

A large mortgage originator recently noted that they are seeing double-digit increases in applications, again, not a sign of depressed demand. New car sales growth is also strong.

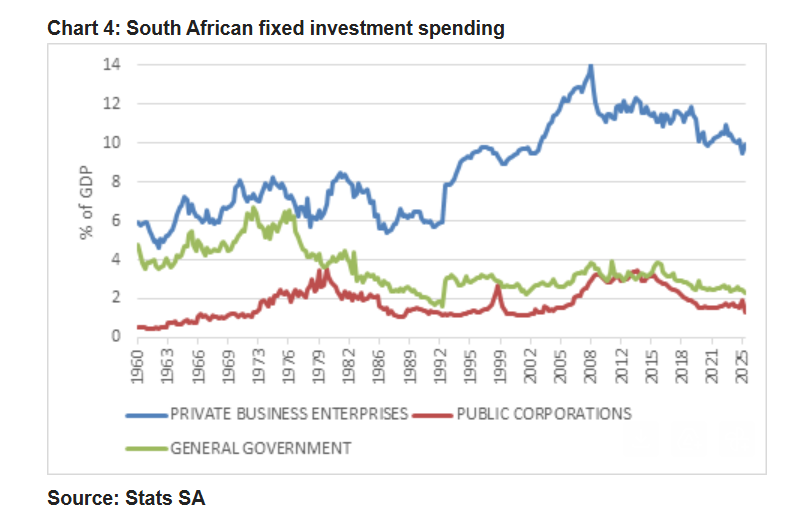

Where demand is weak is in terms of fixed investment. It remains below pre-pandemic levels in real terms, and as expressed as a percentage of GDP, is about half the 30% rule of thumb, where it sustains rapid economic growth.

Interest rates are a factor in fixed investment decisions, but the biggest consideration is probably the size of the opportunity.

Confidence in the future also matters a lot, particularly confidence that the regulatory and political environment will be stable.

This includes the state of US import barriers, which are still up in the air and will constrain opportunities for some firms. Companies also require confidence in the rule of law, protection of property rights and the safety of staff and suppliers.

South Africa’s poor fixed investment rate can be seen in the graph below.

Comments