R2 per litre petrol price disaster coming for South Africa

Petrol and diesel prices are set to rise sharply in South Africa on the back of an intense and prolonged conflict in the Middle East, which is disrupting supply from the region.

Around 20% of all oil supply flows through the Strait of Hormuz on a daily basis. With this body of water effectively closed, oil prices have skyrocketed.

Stanlib chief economist Kevin Lings noted that just ten days ago, a total of 137 ships went through the Strait on a daily basis, including 73 oil tankers.

On 4 March, only two ships went through the Strait. One was a container ship, and the other was a general cargo ship. The Strait is effectively closed.

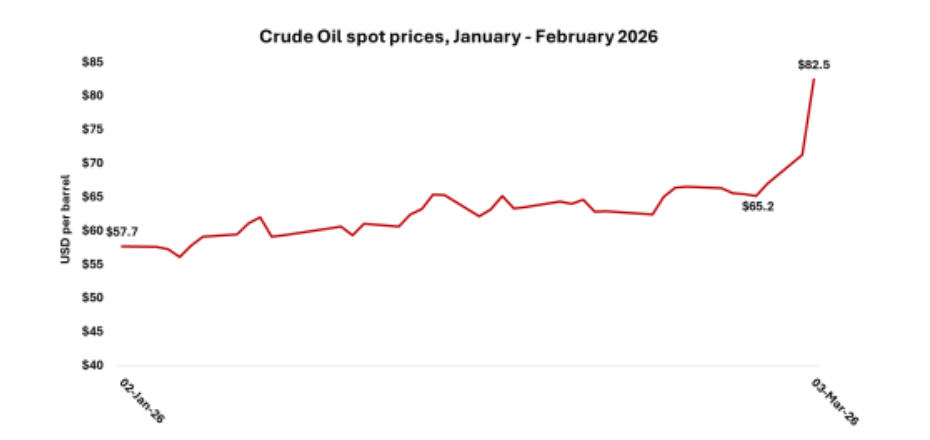

As a result, the oil price has surged by over 20% month-on-month to over $80 per barrel, and the Centre for Risk Analysis (CRA) warned that the price of oil is likely to breach $100 for the first time since the Russian invasion of Ukraine.

The CRA said this is because of the prolonged nature of the military action in the Middle East, with US President Donald Trump indicating that it could last four to five weeks. Secretary of War, Pete Hegseth, said America will go as far as it needs to go.

Retailiant from Iran hit US bases in the region and civilian infrastructure in neighbouring countries, including Bahrain, Jordan, Qatar, Kuwait, Saudi Araia, and the United Arab Emirates.

“This is likely to draw the Gulf states into the conflict. In turn, this will disrupt the reputation for stability the Gulf states have carefully cultivated – with knock-on effects on the perception that oil supplies will flow reliably,” the CRA said.

“While the US and its Gulf partners will hope for a speedy resolution to the conflict, South African businesses and consumers will feel the impact through higher fuel and fertiliser prices.”

The CRA said that the longer the conflict goes on, the worse the effect on fuel prices will be. The Strait is effectively closed and insurers are unwilling to cover the risk of sailing through it, meaning the price of oil is likely to cross $100 per barrel.

As an early indication of impacts yet to come, Saudi Arabian company Aramco has shut its Ras Tanura refinery as a precautionary measure. The facility usually produces 550,000 barrels per day.

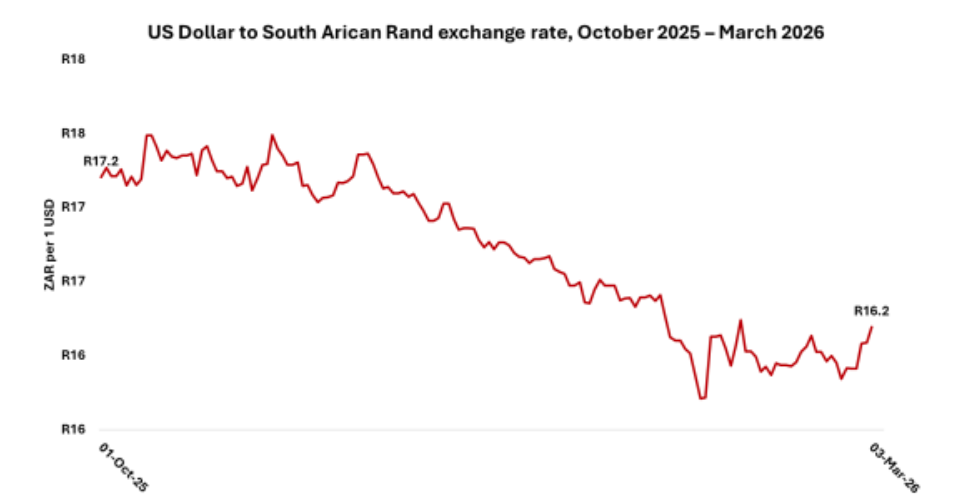

Surging oil prices have been coupled with a weakening rand, with the local currency trading at R16.60/USD after weakening by over 3% in three days.

This is largely a result of investors searching for safe-haven assets amidst times of volatility, with many turning to gold, the US dollar, and the euro and away from emerging market assets.

“South Africa is especially exposed in this scenario, given the country has only one operational refinery and is dependent on imported oil and fuel,” the CRA said.

“South Africa is a net importer of petroleum. In 2024, South Africa imported around 4 billion litres of petrol – the largest share of this came from the UAE and India.”

The UAE, India, and Oman dominated diesel imports. All these countries are affected by the current conflict.

“With the rand weakening versus the dollar to above R16/USD, and the global oil price rising, higher oil and fuel prices are firmly on the cards for South Africa,” the CRA said.

The latest effect on petrol and diesel prices, calculated by the Central Energy Fund, can be seen below –

- Petrol 93 – increase of R per litre

- Petrol 95 – increase of R2.28 per litre

- Diesel 0.05% – increase of R4.40per litre

- Diesel 0.005% – increase of R4.50 per litre

These forecasts are based on the assumption that nothing changes between now and the end of March, which is unlikely.

Inflation shock

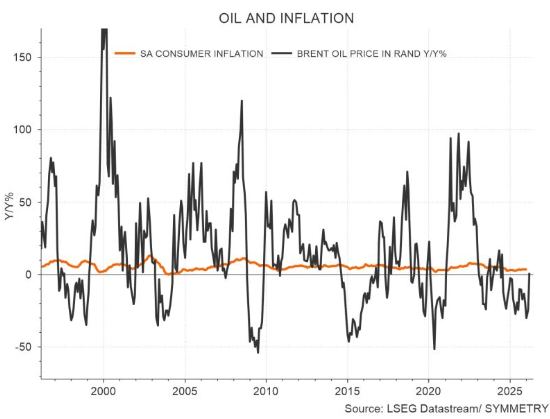

There is fear among market participants, economists, and even the Finance Minister that higher fuel costs will filter into higher transport and food costs, creating an inflationary shock on the South African economy.

“South Africa is a price taker” when it comes to fuel, Finance Minister Enoch Godongwana said in an interview on Bloomberg Television this week.

Rising prices “will have an inflationary impact for us. So the war is worrying,” especially if the war drags on for more than four weeks, he said.

Such an inflationary shock may result in the Reserve Bank having to hike interest rates to prevent a disorderly weakening of the rand and purchasing power.

This would bring to an end its cutting cycle that has resulted in lower borrowing costs for consumers and the government, boosting economic growth.

However, the assumption that sharply rising fuel prices, which can be swiftly reversed, will result in interest rate cuts requires a significant leap.

Lings has indicated that, at the present price increases to petrol and diesel, the Reserve Bank would merely halt its cutting cycle and not hike interest rates.

Chief investment strategist at Old Mutual’s Symmetry, Izak Odendaal, noted that the Reserve Bank will try and “look through” the first round effects of such a spike to see if it impacts other prices in the economy.

“There seems ot be no indication that the war will end anytime soon. This suggests the oil price will remain relevant for some time,” Odendaal said.

“This will put some downward pressure on economic growth and some upward pressure on inflation. The extent depends on how long this drags out for.”

However, Odendaal warned that it is also possible to overestimate the implications and impact of an immediate price hike.

“Oil prices have always been considerably more volatile than the consumer inflation rate. Fuel prices are but one of many components of the consumer price index, accounting for only about 5%,” Odendaal explained.

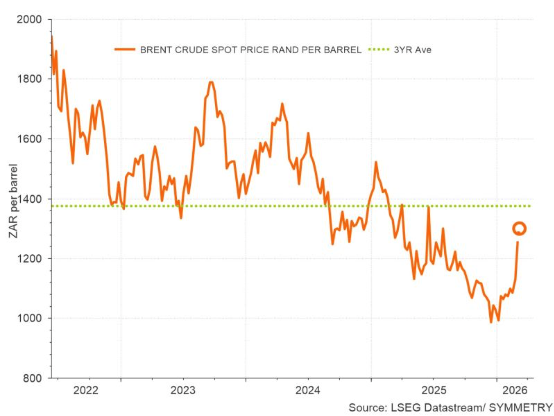

“Base effects also matter. As of 5 March, oil prices in rand terms are flat year-on-year, because oil prices were higher a year ago and the rand was weaker.”

“If things stay more or less where they are in terms of oil prices and the rand, only towards the end of 2026 will the low base lead to higher oil inflation rates.”

As a result, the Reserve Bank will typically try ot look through the direct, first-round impact of oil prices on inflation, and focus instead on second-round effects.

These second-round effects are typically whether firms pass on price increases to consumers and whether inflation expectations adjust.

“It is how businesses and consumers respond to fuel prices that matters more, in other words,” Odendaal said.

Comments