Hidden threat to South Africa’s crown jewel

South Africa’s financial sector is large in relation to the size of its economy compared to peers, making its high levels of concentration a substantial risk to broader stability.

A high level of concentration in the financial sector is a tricky balancing act for regulators, in this case the Reserve Bank and its subsidiary bodies.

Higher levels of concentration makes it easier for regulators to keep a close eye on a handful of major players, or systemically-important institutions.

However, it also makes the broader system more vulnerable to external shocks and instability as it can lead to widespread contagion of distress events.

This is feedback from the Reserve Bank, who outlined the various risks to the financial sector in its second Financial Stability Review of 2025.

A new risk added to its list is concentration in South Africa’s financial system, with a handful of players being dominant in the banking sector and, to a lesser extent, in the insurance industry.

South Africa has a very well-regulated financial system that is highly sophisticated and is the envy of many emerging markets.

The financial sector has also been a major driver of growth and employment in an otherwise stagnant economy over the past 15 years.

This has resulted in the sector being large in relation to the size of South Africa’s economy, making it an increasingly important player.

A high level of concentration in the financial sector is generally regarded as a source of vulnerability, with it contributing to ‘too-big-to-fail’ risk, the Reserve Bank said.

It is working to mitigate this risk by putting in place mechanisms to and resolutions to enable systemically-important institutions to continue providing critical services under distressed conditions.

A second risk is that concentration can lead to rapid and widespread contagion of distress events throughout the financial system.

The acknowledgement of the Reserve Bank of these risks is substantial, marking the first time it has indicated the dominance of a few large player can pose problems for South Africa.

Dominance by few

South Africa’s banking sector is the best example of concentration in the financial sector, with it being dominated by a handful of players.

Traditionally, the sector was dominated by the Big Four of Absa, Nedbank, Standard Bank, and FirstRand. Capitec has recently joined these ranks to make it the Big Five. Investec can also be added as a smaller, but major player.

These banks are crucial to the functioning of the financial system, and their small number makes them fairly easy to regulate.

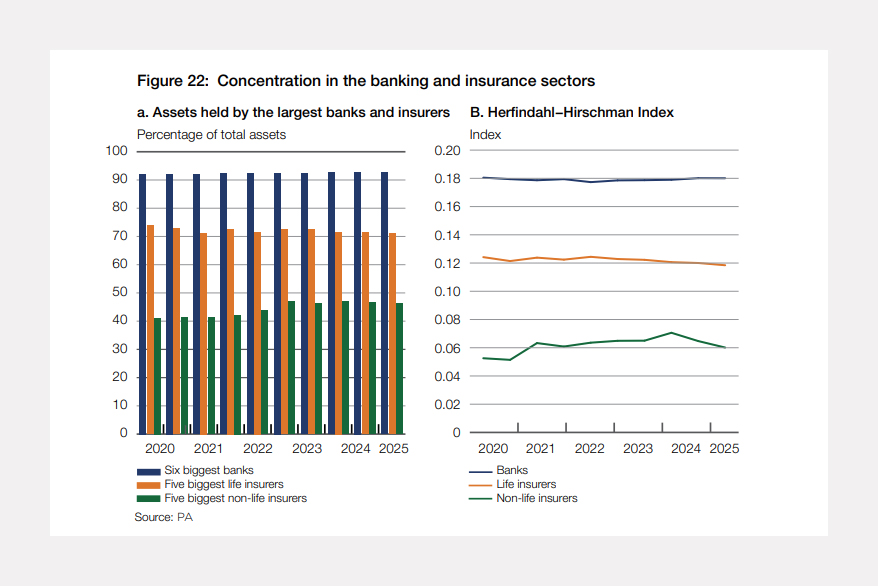

The Reserve Bank noted that the banking sector is highly concentrated in South Africa, with the six largest banks accounting for more than 90% of banking sector assets in the past decade.

To better understand the levels of concentration in financial industries, the Reserve Bank uses the Herfindahl-Hirschman Index (HHI).

This index is a standard measure of market concentration, with an HHI value of more than 0.2 reflecting very high levels of concentration.

Values between 0.15 and 0.2 indicate high concentration; between 0.1 and 0.15, moderate concentration; and below 0.1, low concentration.

The HHI for South Africa’s banking sector, with a value above 0.18, confirms the high concentration in the banking sector.

Compared to the banking sector, the insurance sector is relatively less concentrated, with the five largest life and non-life insurers respectively accounting for over 70% and 40% during the same period.

This is due to the insurance sector’s ability to accommodate a wider variety of business models, which has encouraged the entry of smaller players and contributed to a more competitive landscape.

The life insurance sector is less concentrated, with its HHI declining gradually from 0.125 to 0.119 over the past decade, while the non-life insurance sector consistently reflects the lowest level of concentration.

This is important for broader financial stability, with the Reserve Bank noting the sector’s ability to stabilise or amplify external shocks.

Comments