Standard Bank branches going cashless across South Africa

Standard Bank is rolling out cashless branches across South Africa as it looks to shift the handling of cash transactions to ATMs.

This, in turn, enables the bank to shrink its branch footprint and change the employee mix at its branches to provide more diverse services to clients.

It crucially makes Standard Bank’s physical infrastructure more efficient by allowing it to maintain its points of presence at a smaller cost.

The bank’s CFO, Arno Daehnke, explained this effort to closely control its operating expenses during its interim results presentation for the six months ending December 2025.

The bank produced a strong set of results, with headline earnings per share up 10% to R24 billion and an improved return on equity of 19.1%.

This return on equity is the highest the bank has recorded under the current, more stringent regulatory framework governing banks.

One of the main reasons the bank has significantly improved its return on equity in recent years is its management of cost growth.

A key part of this has been optimising its physical infrastructure to better serve client needs as transactions shift outside of branches and ATMs to digital channels.

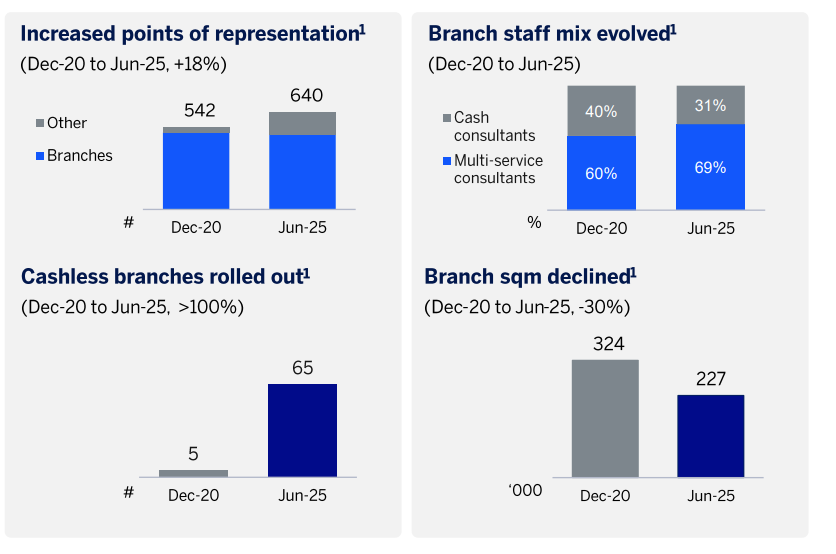

However, the bank has maintained a significant physical presence in South Africa, with its points of presence increasing slightly.

It has done this in a more efficient manner by shifting the transactions still conducted in cash to ATMs and out of branches.

Nearly 90% of the bank’s cash deposits were received via non-branch channels, with 97% of withdrawals being made outside its branch network.

This has enabled it to roll out more cashless branches in South Africa, with 65 currently in operation out of 640 points of presence in the country. This number has increased from a mere five branches in 2020.

Simultaneously, the bank has shrunk its branches by over 30% since 2020 as cash transactions are now conducted elsewhere.

This has resulted in Standard Bank being able to change its staff mix at branches and employ more multi-service consultants and fewer cash consultants.

The graphs below from Standard Bank’s interim results presentation show the ongoing changes to its branch network.

Banks shrinking branches

Standard Bank is not alone in shrinking branches in South Africa, with some of its largest competitors also looking to enhance the efficiency of their infrastructure.

Nedbank CFO Michael Davis told Daily Investor after the bank’s interim results that Nedbank continuously reviews its physical presence to enhance its offering and make it more efficient.

“In South Africa, as a bank, you will always need a physical footprint that your clients can engage with, particularly if you want to offer a complete range of financial services,” Davis said.

He also said that despite the rise in digital transactions, a significant number of transactions still take place within a branch or at ATMs.

“Having said that, what you have seen Nedbank do is retain its points of presence, but reduce the size of its footprint.”

“If you go back over the years, you will see that every branch and every point of presence was roughly the same size and offered the same services,” Davis said.

“What you will see now is that through our relationship with Boxer and the rationalisation of certain points of presence, we still exist in the same places, but the type of facility has changed.”

Davis explained that this comes with different offerings at different facilities and branches, depending on location and customer demand.

“If we have a point of presence with a retailer like Boxer, it is manned by Nedbank staff, but it is very simple in terms of its value offering or proposition,” he said.

“On the other hand, if you go into Sandton City, you will see a huge branch offering everything from transactional banking to stockbroking, asset management, lending, and deposit-taking.”

Davis expects banks to continue rationalising their physical presence to reduce costs and improve their efficiency in serving clients.

Coupled with this is a drive from the bank to improve the capabilities of its ATMs, enabling them to perform more functions than a traditional branch would and serve more clients.

“So, I think big commercial banks in South Africa will continue to require physical points of presence, but these will evolve to become more efficient by leveraging technology,” Davis said.

This will ultimately enable banks to reduce the costs of operating these physical points of presence, taking costs out of occupation, staffing, and real estate.

Comments