The cheapest way to get cash in South Africa is not from an ATM

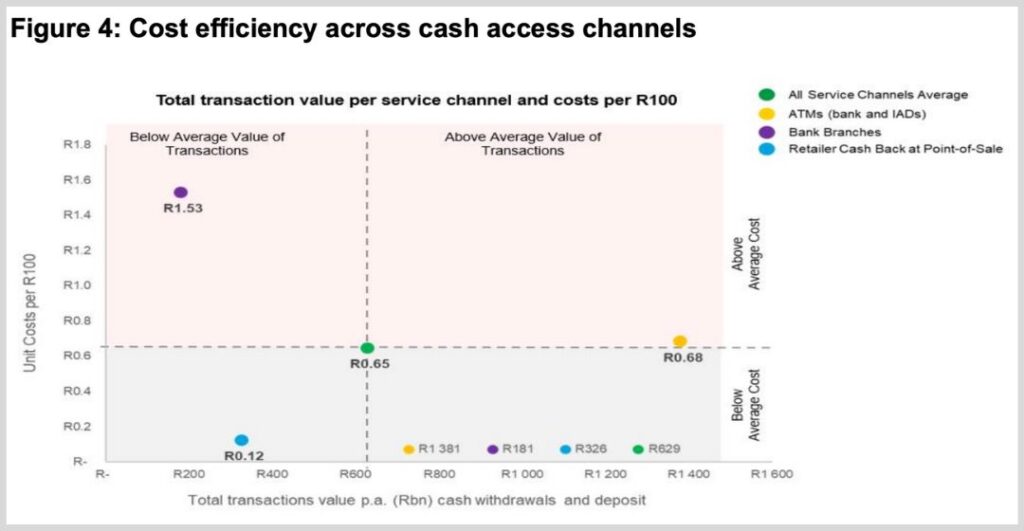

Retailer cash back at point-of-sale is the most efficient and cost-effective way for South African consumers to access cash, beating out ATMs and bank branches.

This is due to retailers being able to leverage their existing infrastructure and high transaction volumes.

This was explained by the Reserve Bank in its latest Position Paper on Cash in South Africa, which is titled ‘Towards a Cash Smart Society’.

In this paper, the South African Reserve Bank (SARB) explained that the use of cash comes with a significant price tag – around R90 billion a year, according to the bank’s estimations.

This cost is largely borne by consumers, as banks, retailers, and other cash operators pass it on to households.

While South Africa is starting to move away from using cash, with digital payments rising, cash remains essential for more than two-thirds of transactions in the country.

The use of cash remains especially prevalent in rural and lower-income areas of South Africa, making the protection of equitable access to cash an important priority for the Reserve Bank.

The SARB explained that around half of the total cost of cash is carried by consumers, both through explicit fees (35%) and indirect channels.

These channels include travelling costs incurred to access cash (14%), the time spent travelling to access cash (31%), opportunity costs of holding cash (3%), losses that include crime (13%), and the sourcing of cash from retailers (4%).

However, the actual cost consumers pay to access cash can vary depending on the source.

To determine which source was the most cost-effective, the Reserve Bank compared four cash access channels: bank branches, independent ATM deployers (IADs), bank ATMs, and retailer cash back at the point of sale.

This analysis showed that retailer cash back at point-of-sale is the most efficient way for consumers to access cash, as this channel leverages its existing infrastructure and high transaction volumes.

“Beyond the inherent advantages of the retail model, it is also noteworthy that the higher the transaction volume (as seen with ATMs), the lower the unit cost,” the Reserve Bank said.

“While bank branches are essential for high-value transactions and deposits, they are less efficient for withdrawals compared to ATMs.”

“ATMs, especially those operated by banks, are a more cost-effective channel for cash transactions, as opposed to bank branches.”

Retailers becoming banks

The SARB’s findings come as South African retailers are increasingly diversifying their offerings to include and expand financial services, with some even planning to launch their own banks.

Retailers offering financial services are not a new phenomenon – South Africans have been able to withdraw cash at retailer checkout counters since the early 2000s.

However, the past few years have seen retailers take a far more decisive step into the financial services industry.

For example, Shoprite now allows customers to transfer money in their stores and offers a fully fledged transactional bank account, which millions of South Africans are making use of.

On paper and in practice, retailers’ shift towards financial services makes sense – large retailers have immense infrastructure and a presence in nearly every town, city, and region in South Africa.

They also have millions of people using their services every day, along with brand loyalty through their existing loyalty programmes.

This has seen large retailers like Shoprite, Woolworths, SPAR, and Pick n Pay growing their financial services segments, now also offering some insurance products and loans.

Retail giant Pepkor recently took this a step further by applying for a banking license in South Africa.

With this license and through its more than 6,000 stores across the country, Pepkor will be able to establish its own fully-fledged bank.

Pepkor CCO Garth Napier said the retailer already processes about 22 million cash-in-cash-out transactions and 4 million bill payments every year, making a bank a natural next step in the retailer’s evolution.

Comments