Absa loses R14 billion in one day

Absa shaved off more than R14 billion from its market cap on Tuesday, 30 June, when its share price plunged by more than 6% following the release of a disappointing trading update.

This comes as new Absa CEO Kenny Fihla, a former Standard Bank bigwig, is attempting to turn the bank around and restore its competitiveness.

On the morning of Tuesday, 30 June, Absa released a voluntary trading update informing shareholders of its expected performance over the six months through June 2026.

In this update, the bank said it expects its revenue to grow by low to mid-single digits, with non-interest income growing faster than net interest income.

It noted that its net interest income growth remains modest, growing by low single digits, which the bank attributed to margin compression stemming from lower policy rates in its Africa regions.

Absa also informed shareholders that its net customer loans and customer deposits are expected to grow by mid-single digits.

The bank’s Personal and Private Banking (PPB) segment is expected to see its net customer loans grow by mid-single digits.

In PPB South Africa, Absa said solid growth in the Vehicle and Asset Finance division should offset more modest growth in the Home Loans and unsecured lending segments.

Absa’s Corporate and Investment Banking (CIB) and Business Banking (BB) segments are expected to see their net customer loans grow by high single digits.

On the non-interest income side, Absa expects mid-single-digit growth, with fee, commission, and insurance income in South Africa expected to be solid.

At the same time, Absa expects its operating expenses to grow in the low- to mid-single digits, resulting in a slightly negative JAWS and a slightly higher cost-to-income ratio, with low-single-digit pre-provision profit growth.

Absa said its credit impairments should remain flat, and it expects to report an improved credit loss ratio.

Overall, the bank expects its headline earnings to grow by mid- to high-single digits in the first half of its 2026 financial year.

This will consist of broadly flat CIB earnings, solid growth from Investment Banking and Global Markets, and lower earnings from the Transactional Banking segments.

The group’s PPB business is expected to report low double-digit headline earnings growth, with modest BB segment earnings growth expected, with solid growth in South Africa, while the Africa Regions segment declines.

It also projects an RoE of around 15% for the 2026 financial year, primarily due to net interest income being weaker than the bank originally anticipated.

Absa explained that its operating environment remained challenging and uncertain over the six-month period, largely because of the Middle East conflict.

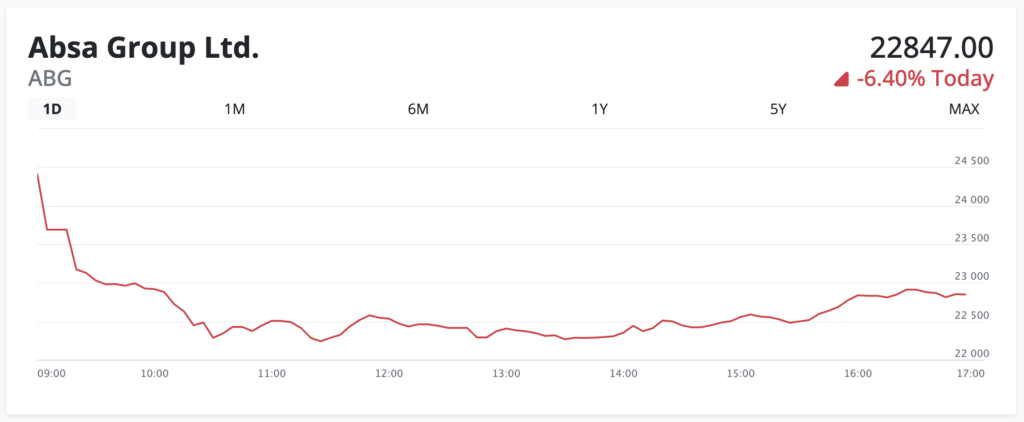

Absa’s share price decline on 30 June can be seen in the graph below, captured after the close of market.

Shareholders respond

Following the release of this trading update, Absa’s share price plunged by as much as 6.4%, shaving an estimated R14 billion off the bank’s market cap.

The bank now has a market cap of R225.46 billion with a share price of R228.47, having ended Monday at R244.10 per share.

This comes as expectations are high that Fihla will usher in a new era for Absa, which has struggled for years.

Absa has struggled to remain competitive in recent years, largely due to instability at the C-suite level.

After former CEO Mario Ramos’ departure in 2019, Absa’s top job became a revolving door, with the bank having had seven CEOs in seven years, including Fihla.

While Absa had not been performing terribly – it still made a profit and experienced consistent earnings growth – it has not managed to keep pace with its banking peers.

Absa has experienced modest growth, while its competitors have boomed, widening the divide between the Red Bank and giants like Standard Bank and Capitec.

Since taking over as CEO in mid-2025, Fihla has vowed to turn this around and help Absa regain its competitiveness.

Fihla has spent the majority of his first nine months in the top job building out the group’s executive committee and filling key positions within the bank’s leadership structure.

To this end, he has brought in key players from Standard Bank to replicate his team and ensure there are individuals in place who can execute his strategy effectively.

Based on the reaction to Absa’s latest trading update, it appears as though Fihla’s turnaround is not taking shape as quickly as some shareholders may have hoped.

PSG equity analyst Marnus Pienaar recently recommended Absa as a stock to hold, saying the bank is set to benefit from a diversified earnings base across its retail, business, corporate, and investment banking operations in South Africa.

Many analysts are betting on Fihla to replicate his success at Standard Bank’s CIB unit at Absa and to use his experience with markets outside South Africa to expand Absa’s reach across the wider continent.

Therefore, the trading update’s projections that Absa’s earnings from its Africa regions and CIB unit would decline and remain flat, respectively, may have been a disappointment.

Comments