South Africa’s most valuable company enters a new era

Over two decades ago, Naspers, through its subsidiary Prosus, acquired a stake in a tiny Chinese technology company – a decision that transformed it from a local player to an international giant.

However, over the past few years, Naspers and Prosus have undergone a fundamental shift in how the market values their non-Tencent businesses.

Simply put, the group no longer wants to be defined by its 2001 investment in Tencent, instead preferring for shareholders and analysts to consider the business as a whole.

As CEO Fabricio Bloisi put it in Prosus/Naspers’ latest annual results presentation, the company has gone from “Tencent Minus to Prosus +”.

To understand this transformation, it is important to go back to 2001, when Naspers made what is arguably the single greatest venture capital decision in South African corporate history.

From 1997 to 2001, Naspers was a traditional media and print conglomerate based in South Africa, run by its then-CEO Koos Bekker.

At the time, Naspers was looking to diversify beyond its traditional media companies, with a specific focus on digital businesses.

That’s when Naspers came across Tencent, an obscure Chinese internet startup founded in 1998. Its primary product was an instant messaging service called OICQ.

OICQ already had millions of customers, yet the company was struggling to translate this popularity into profit and was burning through cash to stave off bankruptcy.

In comes Naspers, whose investment team had, by chance, learned about Tencent in Shenzhen internet cafés when they noticed how many young people were using OICQ.

The team had been sent there to find internet investments in mainland China that would take Naspers to the next level and bring its business into the modern age, which is exactly what they did.

Naspers took a leap, striking a deal to acquire a notable 46.5% stake in Tencent for around $32 million (today, R525.23 billion).

This decision – along with Naspers’ choice to hold its Tencent stake for nearly 20 years – was arguably the most successful venture capital investment in South African corporate history.

Prosus is Naspers’ subsidiary company listed in the Netherlands, though it shares the same underlying investments.

The two companies’ combined structures are highly complex and intertwined. For this article, Naspers and Prosus are treated as the same company.

Value creation

Naspers’ investment in Tencent more than paid off – by 2004, the Chinese tech company was listed on the Hong Kong Stock Exchange and saw its share price quadruple in just two years.

While Naspers’ shareholding in Tencent was diluted as time went on, particularly when the company went public, it benefited immensely from this growth.

Today, Naspers/Prosus holds roughly 23% of Tencent, or around 2.1 billion shares, which is worth an eye-watering $110.9 billion (R1.82 trillion).

It is this investment in Tencent that allowed Naspers to become a giant both locally and globally. Today, it is still the most valuable company on the JSE, with a market cap of R639.5 billion.

However, the success of this investment came at a cost, which Naspers and Prosus are now looking to reverse.

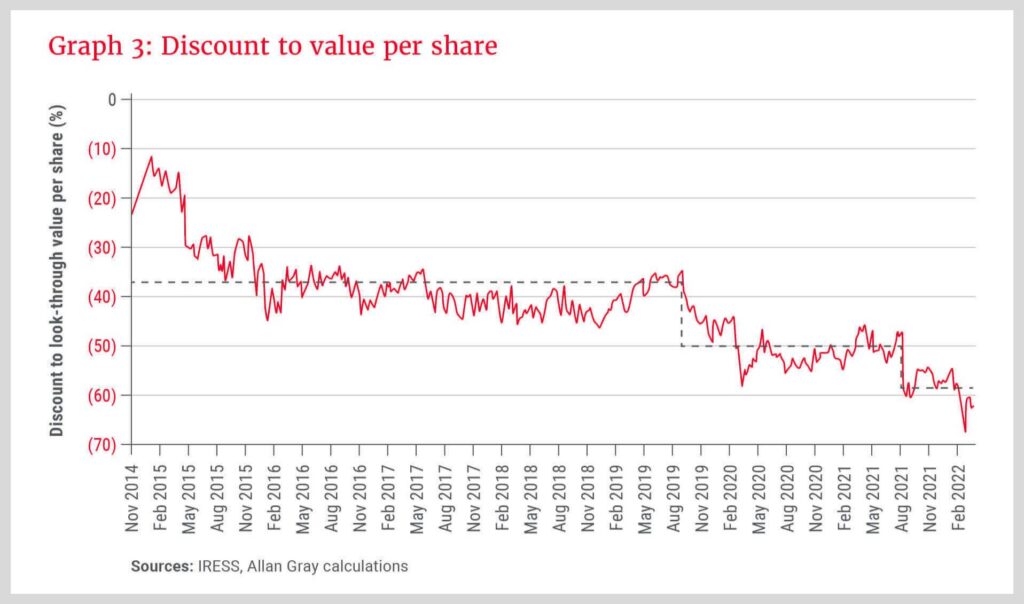

Allan Gray equity analyst Tim Acker previously explained that the success of Naspers’ Tencent investment has been so extraordinary that it has overshadowed all other parts of the business.

For years, investors and analysts have viewed Naspers/Prosus as “Tencent minus a massive discount” since their valuations are significantly lower than the value of their stake in Tencent, creating a holding company discount.

This was not helped by the companies’ struggling e-commerce investments over the past decade, which were loss-making for a long time.

Essentially, this means the market assigned Naspers/Prosus a negative value, and many investors bought their shares purely as a way to get Tencent at a discount.

This view of Naspers/Prosus came back to bite the company in 2022, when its share price declined by nearly 50% from its peak the year before.

Acker attributed this to Tencent’s share price taking a beating, due to declining valuations for tech businesses, rising regulatory headwinds in China, a slowing Chinese economy, and pressure from the United States.

While Tencent was and still is a strong company, this made Naspers/Prosus realise that it was time for a change.

It had already sold a small part of its Tencent stake in 2018, selling 2% for around $9.8 billion (today, R160.96 billion). This was the first time Naspers had sold Tencent shares since first investing in the company in 2001.

A second sale followed in 2021, when Prosus sold another 2% for $14.7 billion (R241.51 billion), bringing its Tencent shareholding down to just under 30%.

Then, Naspers/Prosus got to work, wanting to move the company beyond its “Tencent minus” reputation.

Prosus Plus

The first part of Naspers’/Prosus’ strategy involved an ongoing, open-ended repurchase programme – whereby the companies used the holding company discount to their advantage.

In June 2022, the companies launched a permanent, programmatic sell-down whereby Prosus sells small numbers of Tencent shares on the open market daily, then uses the proceeds to buy back its own shares.

This strategy has proved highly successful, as it allows Prosus to sell its Tencent shares at full market value while buying back its own stock at a discount due to its significant holding company discount.

At the same time, the net asset value per share for remaining Naspers/Prosus shareholders increases automatically, as the shares the company bought back are cancelled and its shares in issue decrease.

Essentially, this means Naspers/Prosus have been able to transfer billions of dollars of value directly to its remaining shareholders every time they sell Tencent shares and buy back their own.

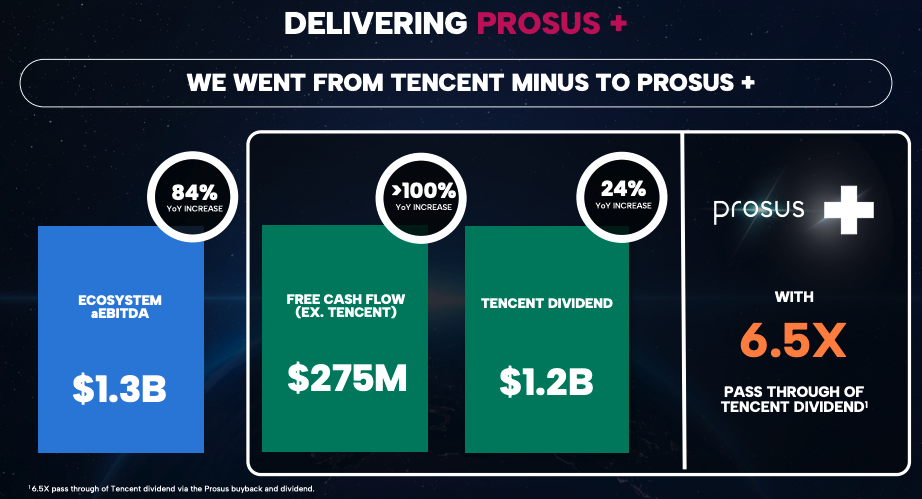

Alongside this repurchase programme, Naspers/Prosus have been investing more heavily in their non-Tencent businesses, with strong results.

In the companies’ latest results for the year through March 2026, they revealed that their free cash flow excluding Tencent had more than doubled year-on-year to reach $275 million (R4.52 billion).

In addition, Naspers’/Prosus’ adjusted EBITDA from its Ecosystem (e-commerce) businesses grew by 84% to $1.3 billion (R21.38 billion).

Notably, this is more than the $1.2 billion (R19.74 billion) in dividends Naspers/Prosus received from its Tencent holding.

For Bloisi, this serves as proof that the company has gone from “Tencent minus to Prosus +”, as he explained in the results presentation.

“I’m excited about how we increased our free cash flow and our EBITDA. We built Prosus Plus,” he said. “We have an amazing leader in China, and Tencent is delivering better every day, in their results and also in AI.”

“We are very confident about the future of Tencent, but Prosus is much more than that.”

Comments