The retirement mistake that could cost you over R1 million

While it can be tempting to dip into your two-pot savings, doing so could cost you well over R1 million by the time you retire.

Ninety One Investment Marketing Manager Leone Hitge that the two-pot system, which came into effect on 1 September 2024, enables millions of South Africans to access a portion of their retirement fund savings before retirement.

“Given the country’s tough economic climate, many have seized this opportunity with urgency – tapping into their retirement savings as a financial lifeline,” Hitge said.

“So far, a staggering R43 billion two-pot withdrawals have been paid out to retirement fund members. The two-pot reform affects all retirement funds, changing the landscape for individual investors with retirement annuities (RAs) as well.”

“Before the two-pot system, RA investors had to wait until age 55 to access their retirement capital. Now, like other retirement fund members, they may withdraw a portion of their retirement capital annually – if needed.”

Hitge explained that the new system splits RA contributions into two pots – a savings component and a retirement component.

“Additionally, for those who accumulated retirement savings before 31 August 2024, there is a third vested component,” she said.

“Withdrawals are only allowed from the savings component, with a minimum withdrawal of R2,000 per tax year. The rest of the retirement capital remains preserved for retirement.”

Hitge stressed that making a two-pot withdrawal is a choice that investors do not have to make.

“Although RA investors can make early withdrawals from their retirement savings, it’s entirely optional. A common misconception is that you must withdraw early – or risk losing your funds in the Savings component.”

“In reality, early withdrawal is a choice. If you decide to leave your money in the Savings component of your RA, it will have the opportunity to grow alongside the Retirement and Vested components, resulting in a much larger nest egg at retirement.”

The impact of Savings pot withdrawals on retirement capital

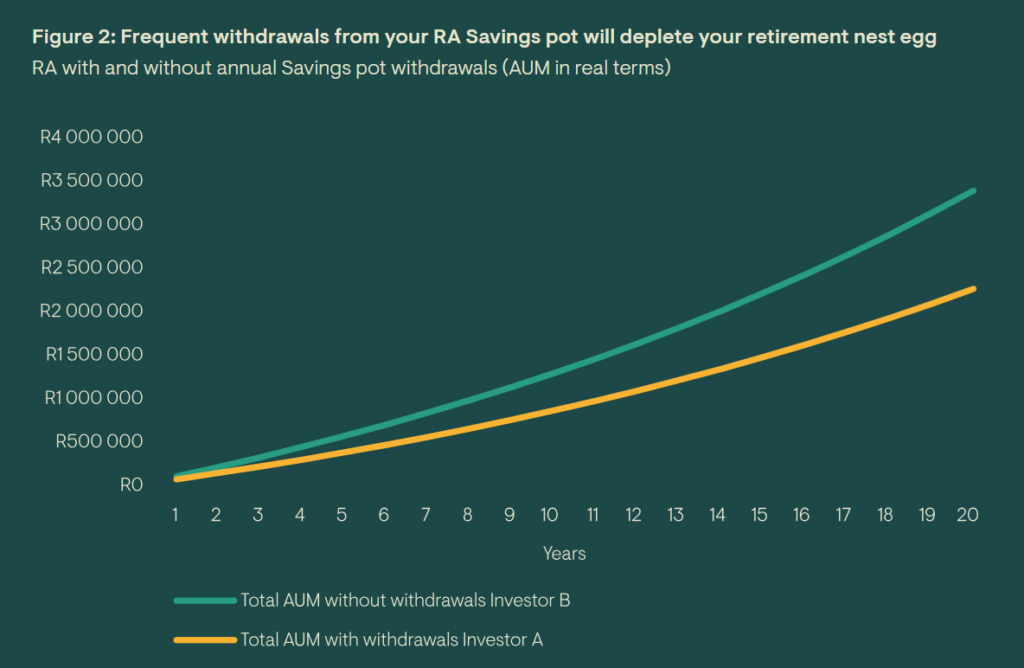

In order to illustrate just how much an early withdrawal could cost in the long term, Ninety One compared the retirement savings of two hypothetical investors.

“Let’s assume there are two RA investors, both contributing R100,000 annually to their RA over 20 years,” she said.

“Each year, one-third of their contribution goes to the Savings component, while two-thirds is allocated to the Retirement component. We assume their portfolio generates a return of 5% above CPI inflation per year.”

Over the 20-year period:

- Investor A withdraws all available funds from their Savings pot every tax year.

- Investor B leaves their Savings pot untouched, allowing it to grow along with the rest of their RA portfolio.

Hitge said the difference is striking. After 20 years, Investor A accumulated R2.26 million, while Investor B’s nest egg grew to R3.39 million.

An assumed return of CPI + 5% per year was used for illustrative purposes only and does not take into account market conditions or the costs associated with investing.

The assets under management (AUM) shown in the chart above are in real terms (i.e. in today’s money terms).

“In a nutshell, withdrawing all the funds from your Savings pot every year – which receives a third of your annual RA contribution – can reduce your total retirement portfolio by approximately a third compared to leaving it untouched,” Hitge said.

Hitge added that investors should also not forget about tax when making a two‑pot withdrawal.

“When you contribute to an RA, you benefit from valuable tax advantages. Your contributions are tax-deductible within certain limits5, and the growth on your investment is tax-free – no income tax, dividends tax or capital gains tax,” she explained.

“However, pre-retirement withdrawals from your Savings pot come at a cost. These withdrawals are taxed at your marginal rate, which means you could receive significantly less than the amount you withdraw.”

“In some cases, a withdrawal may even push you into a higher tax bracket, increasing your overall tax burden.”

Additionally, if you owe a penalty to the South African Revenue Service (SARS) under an IT88 order, this amount will be deducted from your withdrawal proceeds, Hitge said.

“As a result, after taxes and any applicable penalties, the amount you receive could be far lower than expected.”

Hitge urged people to think carefully before dipping into their savings pot and consider the long-term impact on their retirement savings.

“If you choose to make a withdrawal, we encourage you to use SARS’s two-pot retirement system calculator to estimate the tax that will be deducted – so there are no unpleasant surprises,” she suggested.

“Building an emergency fund can help you avoid pre-retirement withdrawals from your Savings pot, protecting your long-term financial security and preventing you from cashing in your future.”

Comments