Warning signs for South Africans earning over R20,000 per month

South Africans earning more than R20,000 per month are seeing their debt levels skyrocket, reaching record highs.

The DebtBusters Debt Index for the first quarter of 2024 shows that high inflation and interest rates are weighing on South African consumers, eating into their disposable income.

The index showed that households now spend two-thirds of their income paying off debt.

It also found that demand for debt management increased, with debt-counselling enquiries rising by 22%. Another concerning sign is that online debt management services usage is up by 30% compared to last year.

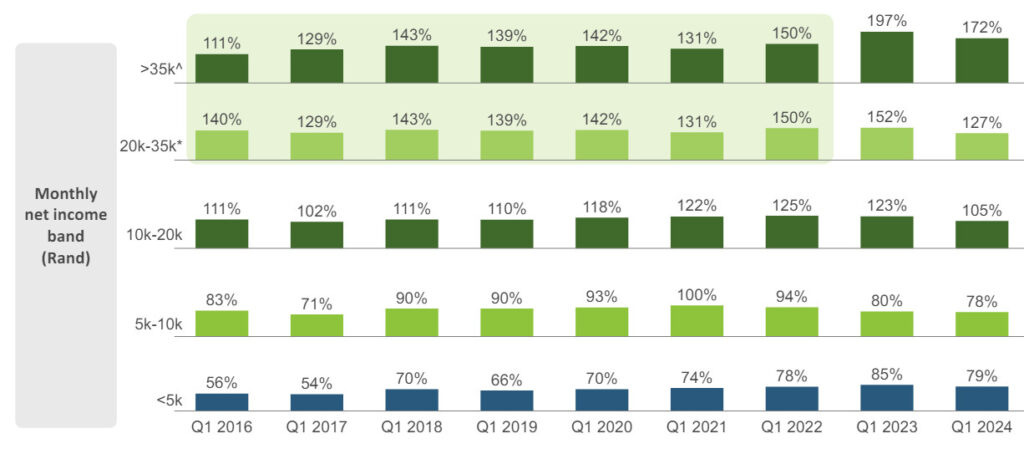

Historically, debt problems have been more pronounced in the mass market, but middle and upper-income bands have recently fallen into dangerous territory.

South Africans’ debt-service burden is now incredibly high, with households using 62% of net income to repay debt.

The debt-to-income ratio for people taking home more than R20,000 per month is 127%, while it is 172% for those earning R35,000 or more. These ratios are at or close to the highest ever.

While average unsecured debt levels are up 14% compared to 2016, top earners have unsustainably high levels of unsecured debt.

“What is concerning is that for people earning R35,000 and more, unsecured debt levels are 41% higher,” the company said.

“This is in line with inflation and indicates that without meaningful salary increases, these consumers are using debt to supplement their income.”

According to DebtBusters’ data, purchasing power in South Africa has diminished by 47%. Nominal incomes are 1% lower than in 2016, while the cumulative impact of inflation over the eight years is 48%.

“While some income groups saw real increase in incomes, on average the trend was slightly downwards,” it said.

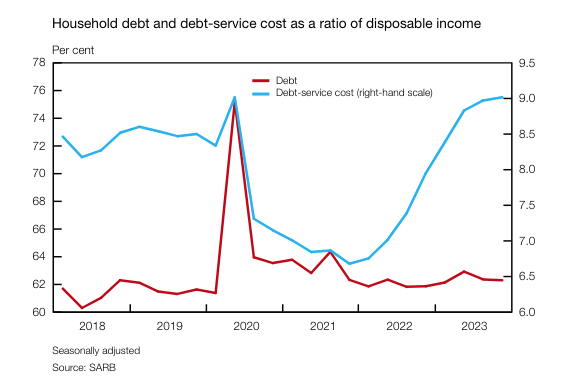

These findings were supported by the Reserve Bank’s Quarterly Bulletin for the first quarter of 2024.

The report found that South Africans spend 9% of their disposable income on debt-servicing costs, while total household debt makes up 62% of total income.

This debt burden stems partly from the significant increase in borrowing during the pandemic when debt peaked at nearly 75% of income.

Combined with rising interest rates, South Africans are now paying the highest portion of their income on debt servicing costs in the past five years.

This rise in debt can be seen in the graph below.

Nedbank economist Isaac Matshego said high interest rates have weighed on the South African consumer.

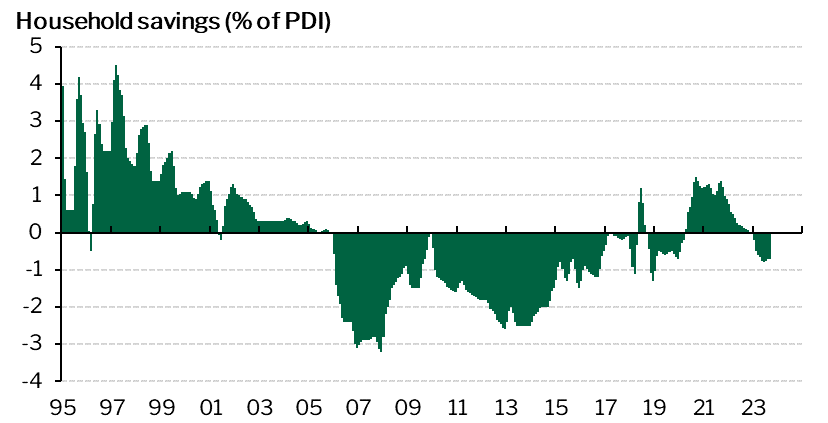

At the Nedgroup Pre-elections Treasurers’ Roundtable on 24 April 2024, he said many South African households have exhausted their savings and resorted to borrowing to make ends meet as they feel the pressure of the country’s high cost of living.

“Consumers now have exhausted their savings and are borrowing again, and at this level of interest rates, the consumer is just feeling the pressure,” Matshego said.

Household savings as a percentage of personal disposable income trended negative in 2023, as South African consumers bore the brunt of the country’s slow economic growth and high inflation and interest rates.

Matshego said this pressure could be seen in high debt defaults, which have been raised by high interest rates and subdued income growth.

He explained that this was worsened in the 2024 February Budget when the National Treasury did not adjust personal income tax brackets for inflation.

This led to a phenomenon known as “bracket creep”, where consumers pay more tax than the previous year despite being in the same tax bracket.

The problem with such high and rising debt levels and increased debt-servicing costs is that consumers’ take-home pay is not necessarily increasing at the same rate.

Investec chief economist Annabel Bishop previously explained that South Africans are getting poorer as their take-home pay cannot keep up with inflation, negatively affecting their real spending power.

Bishop said 2023 and 2022 mainly saw real remuneration fall, weakening Household Consumption Expenditure (HCE) growth in real terms and, therefore, lowering economic growth outcomes. Both 2022 and 2023 were high-inflation years.

In addition, consumers have suffered from a high interest rate, tax, and unemployment environment, all of which have weakened consumer confidence.

“Consumers are taking strain in South Africa, with financial vulnerability elevated,” Bishop said.

Comments