The ANC wanted fixed investment to be 30% of GDP by 2030. Instead, it has plummeted

In the ANC’s National Development Plan (NDP), South Africa’s gross fixed capital formation (GFCF) was set to reach 30% of GDP by 2030.

Instead of reaching this target, the country’s GFCF, a proxy for fixed investment, has plummeted to less than half of the 30% target.

This is despite the government’s efforts to drive productive investment in machinery, equipment, and infrastructure in recent years. Part of this is due to government spending shifting towards consumption in the form of salaries and away from investment.

South Africa’s NDP 2030 was published in 2012 and aimed to provide a roadmap for the country’s economy over the next 18 years.

The former Minister in the Presidency of the National Planning Commission, Trevor Manuel, launched the plan during a joint sitting of both houses of Parliament.

In the plan, the commissioners noted that investment spending in South Africa fell from an average of 30% of GDP in the 1980s to 16% in the early 2000s.

“In effect, South Africa has missed a generation of capital investment in roads, rail, ports, electricity, water, sanitation, public transport, and housing,” the NDP read.

“To grow faster and in a more inclusive manner, the country needs a higher level of capital spending. Gross fixed capital formation needs to reach about 30% of GDP by 2030, with public sector investment reaching 10% of GDP.”

Reaching such a level of fixed investment would significantly accelerate South Africa’s economic growth, with experts pointing to faster growth in other emerging markets as an example.

Melville Douglas’ chief investment officer, Bernard Drotschie, estimated that substantially higher fixed investment could more than triple South Africa’s current economic growth rate of 1% per year.

Drotschie explained that fixed investment is key as the effect is tangible, giving investors hard evidence that the country is turning a corner.

He previously warned that investors may lose patience with South Africa if there is insufficient hard evidence to justify increased investment in the local economy.

“I think some investors have lost a little bit of patience with the economic momentum in this country, which has been weak,” Drotschie said.

South Africa’s NDP 2030 had the right idea in trying to increase fixed investment. However, reality has not matched these lofty expectations.

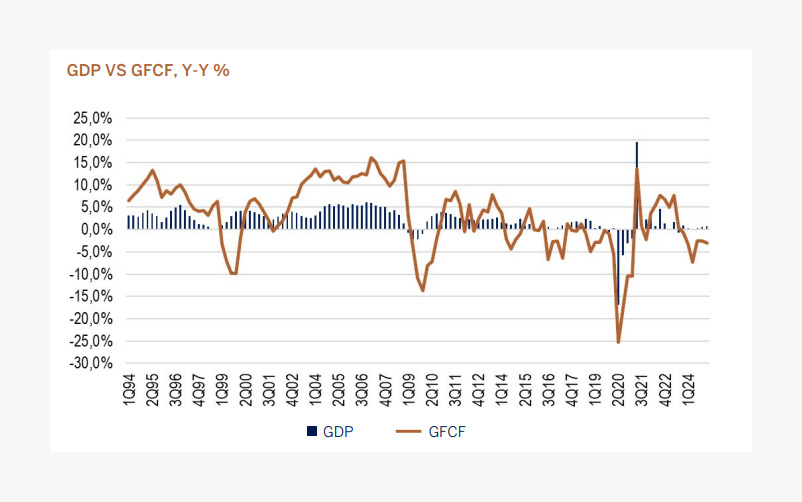

The graph below, courtesy of Melville Douglas senior equity analyst Kgosi Rahube, shows the close link between GFCF and GDP growth in South Africa.

Spectacular failure

South Africa’s GFCF as a share of GDP has declined since 2008, despite the NDP 2030, with government spending shifting towards consumption and away from investment.

The Reserve Bank noted in its latest Quarterly Bulletin that the level of GFCF as a share of GDP is currently less than half of the 30% targeted in the NDP.

For the government to reach its economic growth target of 3% per year, fixed investment would have to rise from below 15% to around 20% of GDP.

In faster-growing economies, such as the United States, fixed investment typically makes up around 25% of GDP. South Africa has not reached this level in over a decade.

Relative to other emerging market peers, such as India, Indonesia, and China, South Africa’s fixed investment rate is significantly lower.

These economies have enjoyed much faster economic growth than South Africa over the past decade, with emerging markets averaging an annual growth rate of 4.5% per year in comparison to South Africa’s 1%.

Over the same period, South Africa’s GFCF as a share of GDP has remained flat at around 13% to 15%. In other emerging markets, fixed investment is typically between 20% and 40%.

South Africa’s GFCF-to-GDP ratio has declined from around 30% in 1976 to 15% in 2024, reflecting subdued investment from private companies, utilities, and the government.

South Africa’s declining fixed investment rate is deep-rooted, with Rahube noting that both private and public investment have declined.

Over the past 15 years, South Africa’s government has preferred to spend increasing sums of money on consumption, particularly salaries, rather than infrastructure.

This has resulted in deteriorating infrastructure across the country and a myriad of crises, from load-shedding to logistics to water.

The Reserve Bank pointed out that the government is trying to shift its expenditure, with payments for capital assets projected to be the fastest-growing area of expenditure.

This is indicative of the reversal of the shift towards consumption expenditure, with the state returning to growth-enhancing investment.

However, the Reserve Bank said that for this to be successful, the state will have to crowd in the private sector due to its weak balance sheet after 15 years of financial mismanagement.

Private corporates in South Africa are sitting on over R1.8 trillion in cash, but many are hesitant to invest their money into a stagnant local economy with elevated levels of policy uncertainty.

To try to get this cash off the sidelines, the National Treasury has created various initiatives to crowd in private investment into infrastructure projects and deregulate parts of the economy.

Rahube said it is a matter of ‘when’, not ‘if’, infrastructure investment will occur in South Africa, with it being a necessity for the country’s economy to grow.

For the private sector to meaningfully participate, key reforms have to occur to deregulate parts of South Africa’s economy and improve business confidence.

“Generally, it is a confidence thing. Confidence is a leading indicator of increased investment. Without it, funds do not flow into the local economy,” Stanlib chief economist Kevin Lings said.

“We find around the world that in order to inspire more private sector investment, you must first get the confidence.”

“What we really need in South Africa is what we call expansion capex, and that tends to be a function of confidence.”

“This type of capital is unlikely to suddenly and miraculously materialise overnight, despite trillions sitting in cash. You have to have policies in place that are going to lead to that outcome.”

Comments