South Africa going from junk to jewel

Global rating agencies appear increasingly likely to reward South Africa’s reform efforts and improving fiscal metrics in the coming years.

While some agencies are still withholding credit rating upgrades in anticipation of clearer signs of improvement, South Africa is on the right track to eventually escape junk status.

In a recent economic outlook, Momentum Investments economists Sanisha Packirisamy and Tshiamo Masike identified economic trends in South Africa.

One trend they identified was that rating agencies are likely to reward South Africa’s reform efforts and fiscal prudence.

“Rating agencies appear increasingly inclined to acknowledge South Africa’s steadier fiscal footing and the gradual, even if uneven, advance of reforms,” they said.

One rating agency, S&P Global, has already rewarded South Africa’s efforts. In November 2025, S&P gave South Africa its first credit rating upgrade in over two decades.

S&P upgraded South Africa’s foreign-currency long-term rating to BB and the local-currency rating to BB+.

While a BB rating still leaves South Africa in so-called “junk status” territory, this marked the first upgrade the country has seen in 25 years.

In addition, S&P maintained a positive outlook for South Africa, signalling confidence in the incremental gains the country has made in terms of fiscal prudence and economic growth.

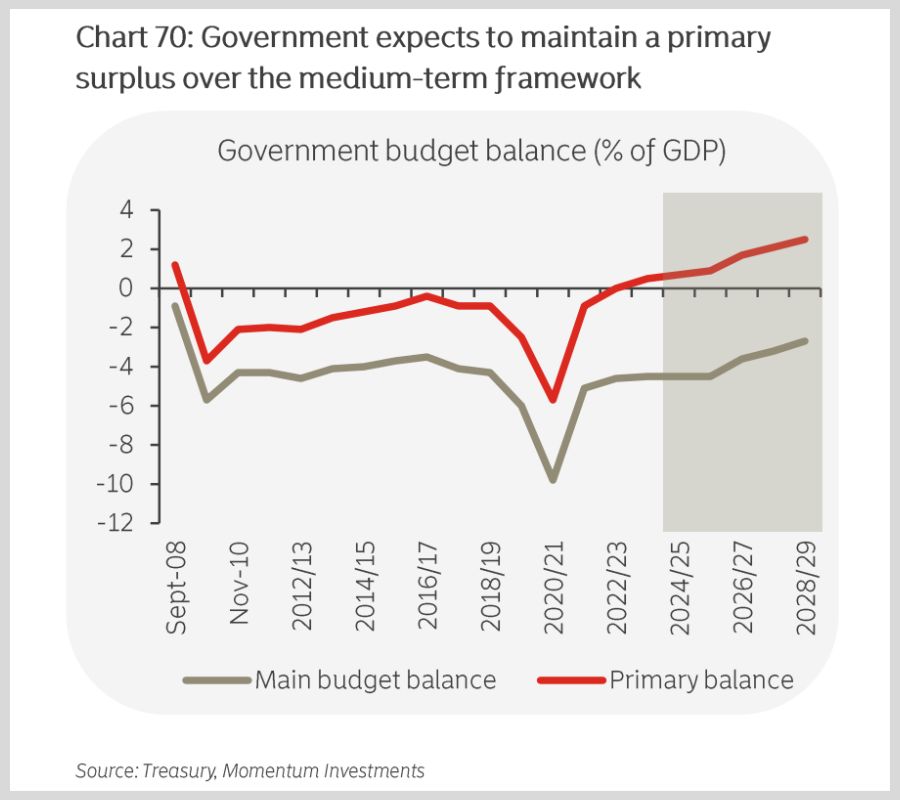

In its review, the ratings agency pointed to improvements at Eskom and the government’s consecutive primary fiscal surpluses, with the country on track to post its third in a row for the 2025/26 fiscal year.

“The positive outlook reflects the potential for further improvements in fiscal metrics and government debt stabilisation if the coalition government continues its fiscal consolidation,” the agency said.

“The outlook also reflects the possibility of stronger growth than we currently expect, despite trade- and tariff-related headwinds, if the authorities accelerate economic reforms while addressing infrastructure pressures.”

S&P said it expects South Africa’s real GDP growth to rise to 1.1% in 2025, slightly below the National Treasury’s expectation for 1.2%, and projects that growth will average 1.5% over 2026 and 2028.

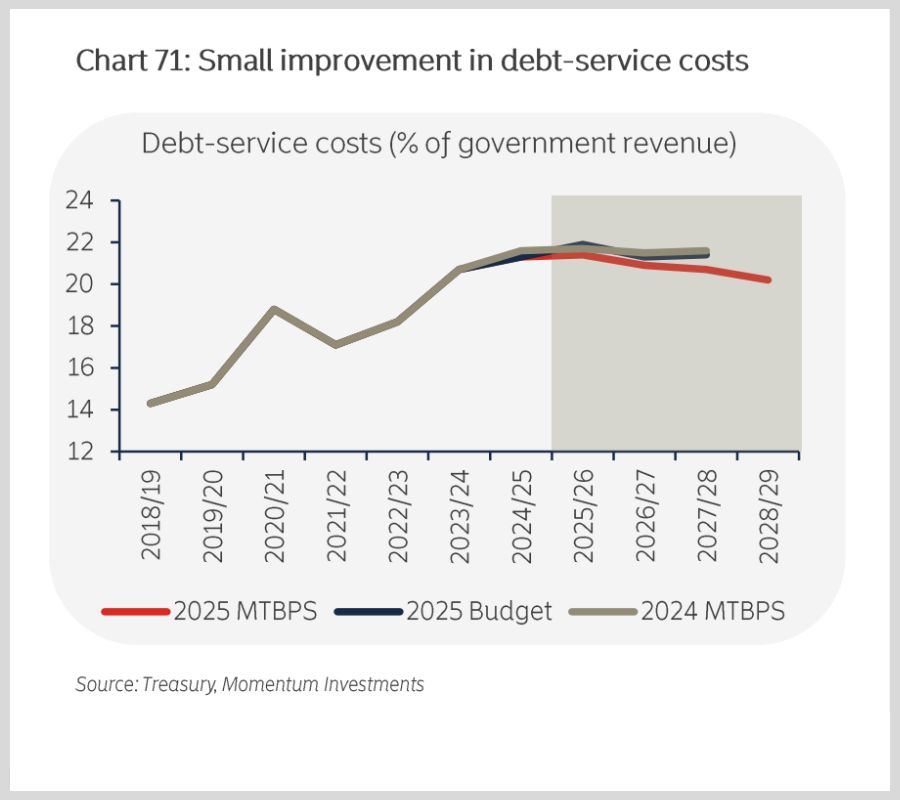

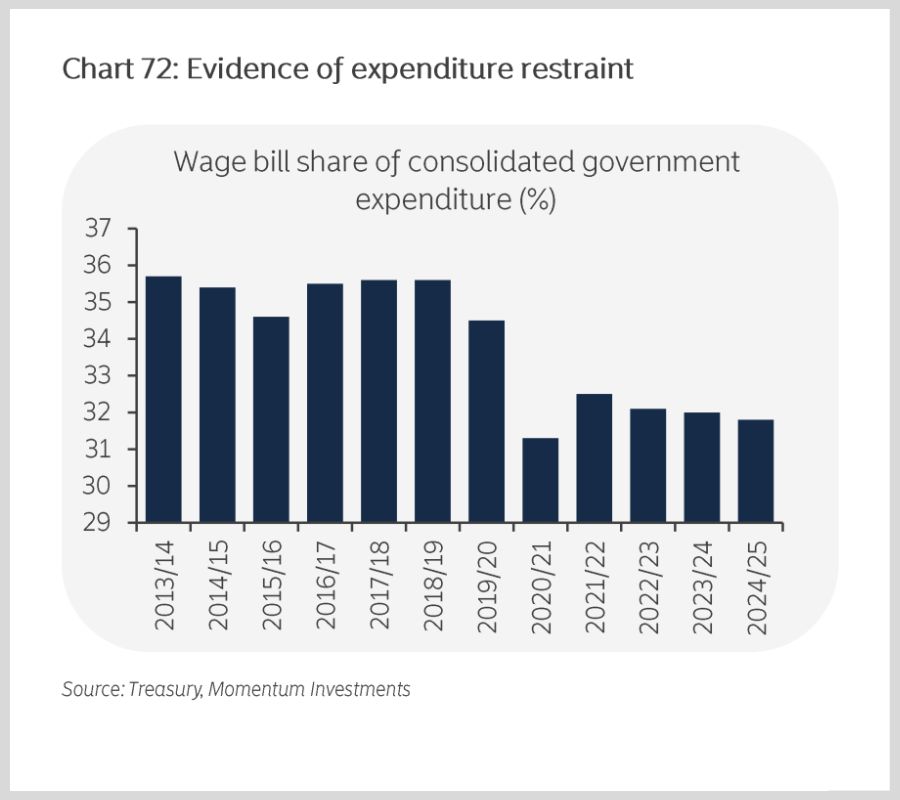

The graphs below, courtesy of Momentum Investments, show three factors counting in South Africa’s favour, including projected primary surpluses, lower expected debt service costs, and evidence of improved expenditure control in the government.

Not out of the woods yet

Packirisamy and Masike pointed out that credit rating agency Moody’s exercised a higher level of caution than S&P, showing that not every agency is buying into South Africa’s reform efforts as yet.

In its latest review, Moody’s acknowledged South Africa’s economic resilience and reform progress, but remained wary of the country’s structural hurdles.

Moody’s explained in a report on emerging markets in Africa, released in September 2025, that South Africa risks a negative spiral where high interest rates and subdued economic growth limit domestic investment and further harm the country’s economy.

“Without improvements, South Africa risks continuing a negative spiral in which high interest rates aimed at attracting inflows amid subdued growth limit domestic investment and further hinder economic prospects,” the agency warned.

However, Packirisamy and Masike said markets have taken note of firmer expenditure control and revenue outcomes that have held up better than expected in South Africa.

They said both of these factors are beginning to ease pressure on the state’s hefty interest bill. South Africa’s government currently spends around R1.2 billion a day to service its debt.

The economists added that further expected evidence of fiscal consolidation and improvements in energy and logistics in South Africa have left market participants cautiously optimistic over a favourable move in ratings in 2026.

“Debt levels remain elevated, and refinancing demands are still sizeable, but the trajectory is looking less precarious than in recent years,” they said.

“In this context, agencies have more grounds to indicate a shift in their outlooks, reflecting the view that improved policy execution is slowly reducing sovereign risk.”

Comments