Good news about interest rate cuts in South Africa

Finance Minister Enoch Godongwana’s decision to lower South Africa’s inflation target spells good news for upcoming interest rate decisions.

The Reserve Bank’s Monetary Policy Committee (MPC) is meeting again on Wednesday, 19 November, where a decision to cut interest rates is looking increasingly likely.

The Bureau for Economic Research’s (BER) Lisette IJssel de Schepper explained that, prior to the Medium-Term Budget Policy Statement (MTBPS), the firm did not expect changes to interest rates.

When presenting the MTBPS on Wednesday, 12 October, Godongwana also announced that South Africa’s inflation target would be lowered to 3%.

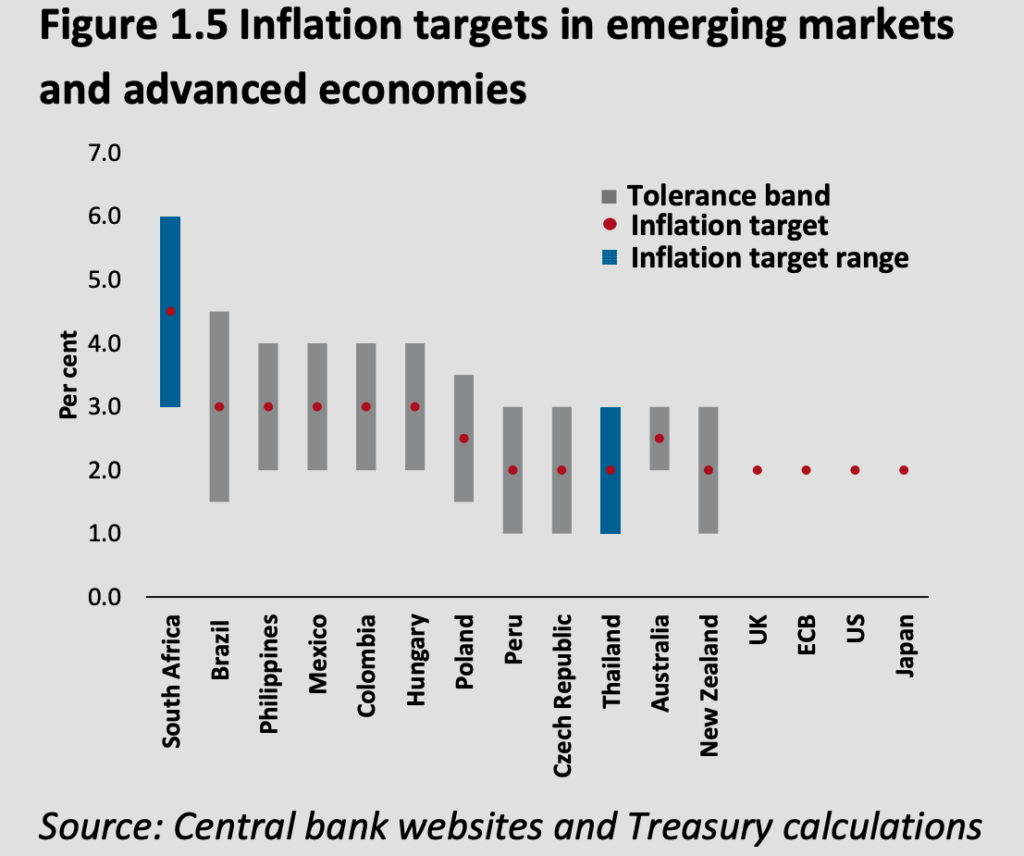

This came after months of discussions between the Reserve Bank and the National Treasury, and will see South Africa’s inflation target change from a range of 3% to 6% to the lower, more narrow target of 3%.

Prior to this official change, the Reserve Bank announced in its July meeting that it would now prefer a 3% target, and was setting monetary policy to achieve this goal.

Therefore, Ijssel de Schepper explained that the official announcement of a lower target brings the Treasury in lockstep with the SARB.

She said this would make it easier for the Reserve Bank to guide the economy toward the new 3% target over the next two years, reducing transition costs and enhancing the fiscal and economic benefits that will accrue over time.

The Reserve Bank has been a staunch advocate of lowering the country’s inflation target, saying it would not only bring South Africa more in line with its global peers but also lead to lower inflation and interest rates in the long term.

Before the official target change, the BER expected that there would be a split among MPC members at its upcoming November meeting, with the majority leaning towards keeping rates on hold.

However, following the announcement in the MTBPS that South Africa’s inflation target will be lowered, the BER believes the majority will now vote in favour of a cut.

“If anything, the possibility of a 50bps rate cut will now be discussed, although that will not be implemented,” Ijssel de Schepper said.

“Importantly, if the SARB does cut next week, it does not mean we will see consecutive interest rate declines in the next couple of meetings.”

“The SARB is likely to keep a close eye on inflation expectations, its CPI forecast and will fine-tune policy as risks emerge and subside.”

Benefits abound

The decision to lower South Africa’s inflation target has been years in the making, with a National Treasury review published in 2022 recommending a target change.

The Reserve Bank has been targeting the 3% to 6% range since 2000, and has been aiming to anchor inflation around the mid-point of this range, 4.5%, since around 2017.

In 2025, talks to officially change the target began in earnest, with the National Treasury and the Reserve Bank conducting joint research on the impact of a lower inflation target on the economy and the fiscal framework.

This research found that South Africa’s average inflation rate is higher than trading partners and emerging market peers.

The Treasury said in the MTBPS that this inflation differential erodes the country’s competitiveness and causes the rand exchange rate to depreciate.

“Higher inflation also increases the cost of living to the detriment of households – particularly the poorest and most vulnerable,” it said.

“In the short term, reducing the inflation target to 3% will result in more cuts in interest rates than would be the case under a 4.5% target.”

“Over time, a lower target will decrease inflation and inflation expectations, creating the space for permanently lower interest rates, which will support household spending and investment – boosting economic growth and job creation.”

The Treasury said a lower target also aligns South Africa with international best practice and makes the cost of borrowing cheaper by reducing the inflation risk premium that investors demand to lend to South Africa.

However, the Treasury warned that this would not be without some short-term pain, as lower inflation will also initially slow nominal GDP growth and revenue growth, given that tax receipts are linked to nominal GDP.

“This will reduce fiscal space, while the real value of public debt will decline more slowly,” it said.

Ultimately, the Treasury decided that the benefits of a lower target outweigh these costs, and given South Africa’s more positive fiscal trajectory, a stronger economy should be able to mitigate the risks.

Comments