SPAR under siege – but it has an ace up its sleeve

SPAR’s Irish business has emerged as a diamond in the rough amid its local operations’ continued struggles, making the retailer an interesting investment case.

One local investor – Camissa Asset Management – backs the Irish business’s strength and is betting on SPAR, while many other investors are turning away.

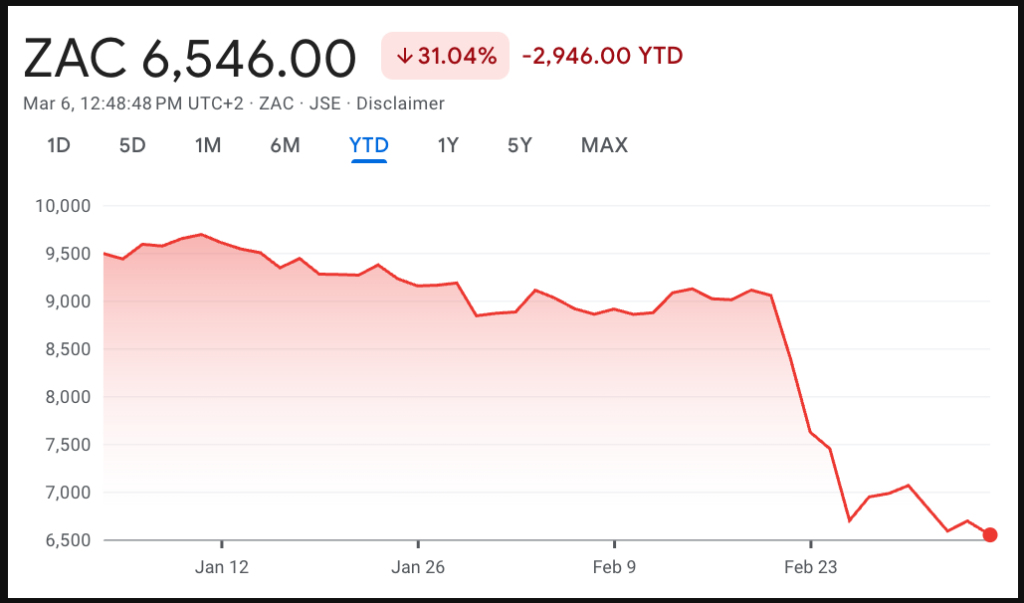

2026 has not been a good year for SPAR so far. In the first two months of the year, the retailer has been served with a multi-million-rand lawsuit, its CEO has resigned, and a disappointing trading statement saw SPAR’s share price fall to a 16-year low.

This trading statement revealed that SPAR expects its turnover to grow by a modest 2.1%, and projected a decline in its gross profit margin for the first half of the retailer’s 2026 financial year.

SPAR attributed this to a highly competitive market, with low food inflation and deflation across several key categories, noting that its internal selling price inflation averaged 2.6% over the period.

This is below the official 4.3% food inflation rate, suggesting the retailer is not fully passing on cost increases to consumers, or that it is operating in a highly deflationary environment for key categories.

To add insult to injury, the retailer also faces a rising cost base, as SPAR’s bungled SAP system rollout continues to haunt it through heavy IT infrastructure investment.

On the day this trading statement was released, SPAR’s share price plunged by as much as 10%, and continued to decline in the days after.

Year-to-date, SPAR’s share price is down over 30%, reaching levels last seen in 2010.

SPAR is aware of its challenges and has been implementing a turnaround plan to streamline operations and cut costs.

This has led to some success so far, with the retailer having reduced its debt levels and exited a few of its struggling European operations.

SPAR has also optimised its distribution network and implemented key operating margin initiatives, such as centralising non-trade procurement, improving credit discipline, and enhancing pricing and logistics productivity.

However, based on the retailer’s recent share price decline, it is unclear whether many investors are ready to buy into SPAR’s turnaround – with one notable exception.

SPAR’s pot of gold

On 27 February 2026, four days after SPAR’s disappointing trading statement was released, it notified shareholders that Camissa Asset Management had acquired a beneficial interest in the company.

Following this acquisition, Camissa now holds 5.04% of SPAR’s total issued ordinary share capital.

This signifies a bet placed on a retailer that many investors seem to be turning away from. Daily Investor asked Camissa about its investment rationale for this acquisition.

Camissa investment analyst Mohamed Mitha told Daily Investor that the asset manager shares some shareholders’ concerns regarding the competitive dynamics facing SPAR franchisees at the retail level.

In addition, he said there are some concerns regarding the company’s operational challenges at the wholesale level.

However, despite this, he said Camissa believes SPAR’s shares are being mispriced.

“A key component of our investment thesis is the Irish business, which continues to perform well and deliver solid results despite a challenging trading environment that has persisted for several years,” he explained.

SPAR’s Ireland business often goes overlooked amid its larger operations in Southern Africa, its home market.

However, the company has a long history in the European nation, with SPAR Ireland having been established in 1963.

With a presence across the Republic of Ireland, SPAR is one of the country’s largest convenience retail groups, where it operates three of the four SPAR formats – SPAR, EUROSPAR, and SPAR Express.

SPAR’s operations in Ireland are run by a leading wholesale and retail company, BWG Foods, a subsidiary of SPAR Group Southern Africa.

The company has 1,161 stores, 25 distribution depots, and over 2,100 employees in Ireland.

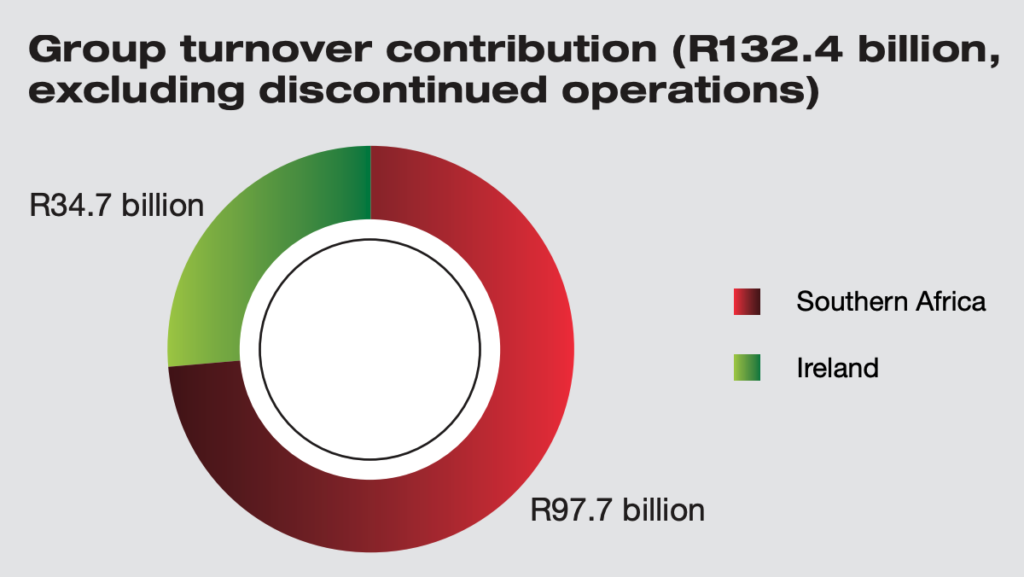

In the retailer’s latest annual results for its 2025 financial year, Ireland contributed over 26% of the group’s turnover, constituting R34.7 billion of the total R132.4 billion generated from continuing operations.

This is less than half the R97.68 billion generated by SPAR’s Southern Africa business.

However, the Irish business made an operating profit of R1.14 billion, far more than the Southern African business’s R893.1 million.

In addition, SPAR is also optimistic about Ireland’s economic prospects. It said Ireland’s economy remains strong, with GDP projected to grow by 9% in 2025.

“Inflation is expected to average around 2% in 2025 and 2026, helped by easing energy costs and a tight labour market,” the retailer said.

This stands in stark contrast to South Africa, where GDP growth, while improving, is expected to reach 1.4% in 2025 and 1.6% in 2026. Most food retailers in South Africa have also reported a low-inflation or disinflationary environment alongside rising input costs.

“At the current share price and after accounting for our valuation of the Irish operations, the implied valuation of the South African business appears excessively punitive,” Mitha explained.

“We have therefore taken what we consider to be an appropriate risk-adjusted position.”

Comments