Pick n Pay’s crown jewel continues to sparkle – but there is a catch

Boxer has reported a strong increase in its turnover for the first half of its 2026 financial year, with like-for-like sales experiencing slower growth.

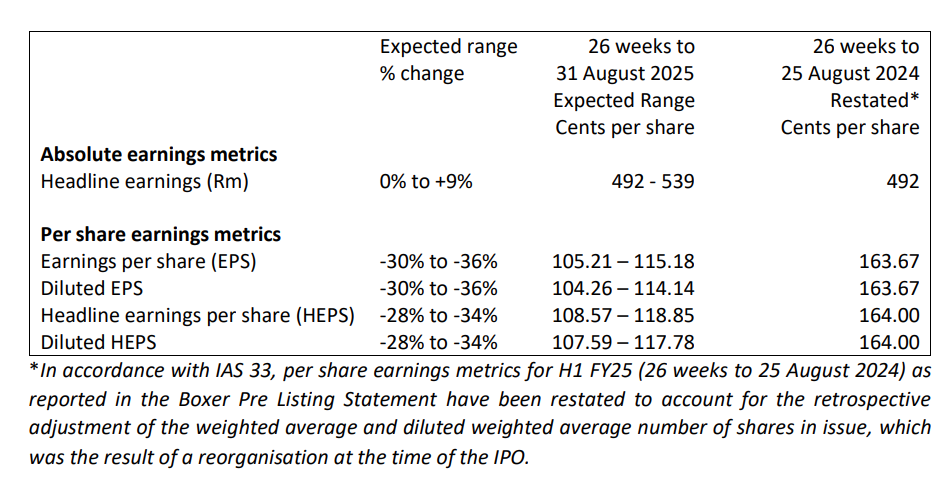

However, due to the structure of its initial public offering (IPO) on the JSE, the retailer expects a significant decline in its earnings per share and headline earnings per share.

Boxer’s listing structure resulted in its ordinary shares increasing by 51.1% from R299.99 million to R453.29 million in November 2024, affecting the per share metrics in its current financial year.

As a result, the company said that the earnings per share and headline earnings per share metrics are not reflective of its operational performance for the 2026 financial year.

Operationally, Boxer continued to perform well, with improved turnover momentum during the last two months of the first half of the 2026 financial year.

The retailer’s turnover for the period grew 13.9% year-on-year, with like-for-like sales increasing by 5.3%. Internal food inflation was -0.7% for the period.

This bodes well for Pick n Pay, which still owns over 60% of Boxer following its separate listing, which was key to the survival of the parent company.

Today, Boxer is more valuable than Pick n Pay on the JSE, with its market capitalisation of R29.2 billion being over R10 billion more than its parent’s R18.19 billion.

Boxer’s strong turnover growth was largely driven by it opening new stores throughout the first half of the year.

During the first four months of the year, the company opened seven superstores and ten liquor stores as it continues its aggressive rollout.

In its previous trading update on 12 May, Boxer said it remains confident that it will meet its guidance of low-teens turnover growth for the 2026 financial year.

“While there is always an element of uncertainty in the precise timing of store openings, current visibility suggests that Boxer remains on track to meet its previously communicated FY26 store rollout targets,” the retailer said.

“Boxer remains confident with its FY26 gross margin outlook, despite the inherent margin management challenges in a low inflation environment.”

“Boxer remains comfortable that it is on track to meet its previously guided low-teens FY26 turnover growth objective, given the like-for-like momentum and store rollout programme,” it said.

Boxer is currently finalising its results for the period, and is accordingly able to update investors that its expected first-half FY26 earnings fall within the ranges as set out in the table below.

The improvement in headline earnings is driven by a strong trading result, which was able to partially offset the previously guided incremental costs associated with being a listed entity, Boxer said.

The decline in the per share earnings metrics was due to an increase in the weighted average share count arising from the IPO, which resulted in the weighted average number of ordinary shares in issue rising to R453.29 million.

Comments