Allan Gray’s four rules to make your retirement savings last

Most South Africans cannot afford to retire comfortably, so careful financial planning is crucial in ensuring you do not run out of your retirement savings.

The average South African retiree can replace only 31% of their income with their retirement savings.

This means that most South Africans will be forced to live on less than a third of their preretirement income or risk outliving their retirement savings.

Additionally, only 9% of retirees manage to replace 80% or more of their pre-retirement income.

These numbers are supported by anecdotal feedback from independent financial advisers who say that 90% of their clients cannot retire comfortably.

On top of this, many retirees are living longer today than in previous generations, but while their lifespans are improving, their health spans are not improving at the same rate.

In other words, people’s retirement savings need to last longer, but their expenses are going up simultaneously.

Living beyond anticipated years can significantly affect an individual’s replacement ratio and the amount of money they have access to in retirement.

“If a client lives five years longer than expected, their replacement ratio can fall below 50%, creating a serious challenge to maintaining their lifestyle in retirement,” Discovery Invest CEO Kenny Rabson explained.

With this in mind, it becomes even more important for South Africans to carefully manage their finances to ensure that they do not run out of their retirement savings.

“Retirees who primarily rely on their living annuity investments to provide them with a steady stream of income are often haunted by the question: How do I make my income last throughout retirement?”

This was explained by Shaun Duddy, head of retail product development at Allan Gray, who said that there are four golden rules that are essential long-term drivers of success for living annuity investors.

If applied appropriately, these rules can help make your retirement savings last, Duddy noted.

Rule 1: Plan for a reasonable number of years in retirement

A crucial first step in preserving your retirement savings is planning for an appropriate number of years in retirement.

Many retirees underestimate how long their savings will need to last, which increases the risk of depleting their funds prematurely.

“The number of years you need to plan for essentially comes down to how certain you want to be that you have planned for enough,” Duddy said.

“To give yourself a 90% chance that you have planned for enough years and will not outlive your planning horizon, research suggests that living annuitants should plan for approximately 40 years at age 55, through to 10 to 15 years at age 85.”

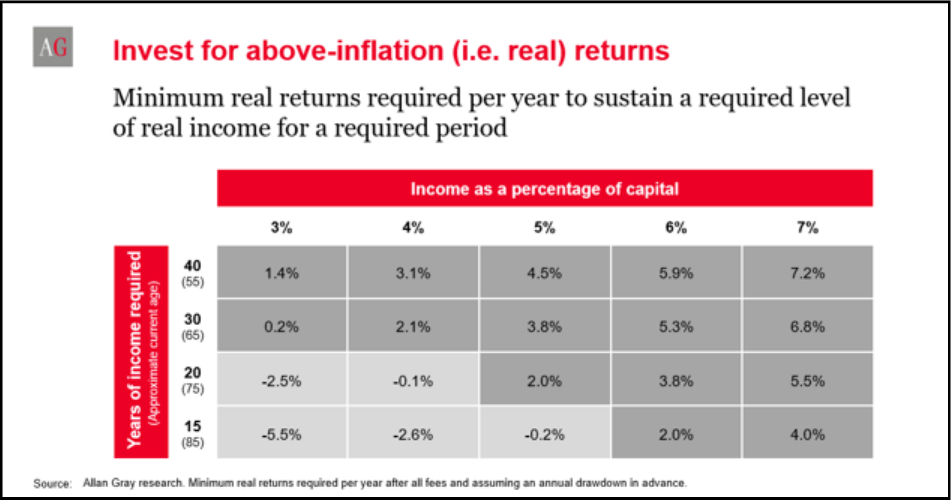

Rule 2: Invest for above-inflation (real) returns

“Whenever you invest, you are looking to get the best possible returns, while accounting for the risk you are able to tolerate,” Duddy said.

“For a living annuitant this is even more important because you need to understand what level of real returns are required to sustain your required level of income for the duration of your retirement.

For example, consider a retiree planning for 30 years of retirement, drawing 4% of their capital annually and adjusting this amount for inflation each year. To meet this goal, they would need a real return of 2.1% per year.

“In this scenario, if inflation is 6.1% per year, then you would need a return of about 8.2% per year in each of the 30 years. These numbers are even higher once you add in volatility.”

“However, this picture changes significantly if you increase the drawdown rate and/or the number of years in retirement.”

To achieve these returns, Duddy explained that it is essential to invest in growth assets like equities, which historically have delivered strong real returns over the long term.

“Long-term data shows that growth assets like equities are essential for real returns. You would need a minimum of 50% exposure to growth assets and, depending on your risk tolerance, there has been value in going up to 60 – 70%.”

Rule 3: Manage volatility but not at the expense of real returns

While growth assets are essential, managing the volatility associated with them is equally important, Duddy explained.

Large fluctuations in your portfolio’s value can increase the risk of running out of money, especially if you withdraw income during market downturns.

However, reducing volatility should not come at the expense of real returns, as lower returns may undermine the sustainability of your income. A balanced approach is needed.

Research demonstrates that adding an appropriate level of offshore exposure has been a good way to do this but be cautious against diving in headfirst.

“It has been most appropriate to have at least 50% exposure to growth assets, and then to manage volatility through an appropriate amount of offshore diversification, historically in the region of 30 – 50%, and through good quality active management.”

Rule 4: Draw a reasonable level of income

The rate at which you draw income from your living annuity is one of the most significant factors affecting how long your savings will last.

For retirees planning for a 30-year horizon, starting with a drawdown rate of 4–4.5% provides a high probability of success – up to 90% or more if the other rules are followed.

However, higher drawdown rates increase the risk of running out of money.

If you need to withdraw more than 4.5%, you have two options, Duddy said.

First, you can reduce your annual income increases to below the inflation rate. This allows you to start with a higher income but offsets the long-term impact by limiting future increases.

Second, you can consider transferring some or all of your funds to a guaranteed annuity.

“A guaranteed annuity offers annuitants a guaranteed income for life, regardless of how long their retirement is, and it typically offers a higher starting income than what may be considered sustainable in a living annuity,” he added.

“These benefits come at the cost of reduced flexibility and lower or no capital legacy on death.”

Comments