Foreigners dump South African stocks

Foreign investors have sold JSE-listed shares worth R113.3 billion so far in 2024, with the selling trend continuing despite renewed optimism in the country’s economy.

This presents a growing threat to South Africa’s financial stability and security, with the country’s capital markets slowly drying up.

Furthermore, it puts increased pressure on local asset managers, particularly banks, to pick up the slack and increase their exposure to South African assets.

This is not necessarily a problem. However, coupled with growing government debt issuance, banks are increasingly exposed to a single common risk.

The Reserve Bank has repeatedly warned that this increases the likelihood of financial volatility and instability.

In its latest Financial Stability Review (FSR), the bank explained that the more liquid, deeper and diversified financial markets are, the larger the shock they can absorb without becoming dysfunctional.

In financial markets that are shallow and illiquid, smaller shocks are amplified and can have a disproportionate disruptive effect on the wider system.

This increases the likelihood of a single external shock disrupting the stability of South Africa’s financial system, which would have negative effects on the broader economy.

The June 2024 edition of the FSR noted a significant decline in market depth and liquidity caused by capital outflows, the dominance of government bonds in the debt market and the buy-and-hold strategies favoured by investors.

Post-election optimism with the formation of the Government of National Unity (GNU) has supported demand for local assets and reduced the financial system’s vulnerability to an extent.

In particular, demand for South African government bonds has been strong since the end of May as the GNU reaffirmed its commitment to fiscal consolidation.

By contrast, equity flows continued to decline despite the positive sentiment, with foreign investors looking for more sustained economic reforms. Non-residents were net sellers of JSE-listed shares worth R113.3 billion.

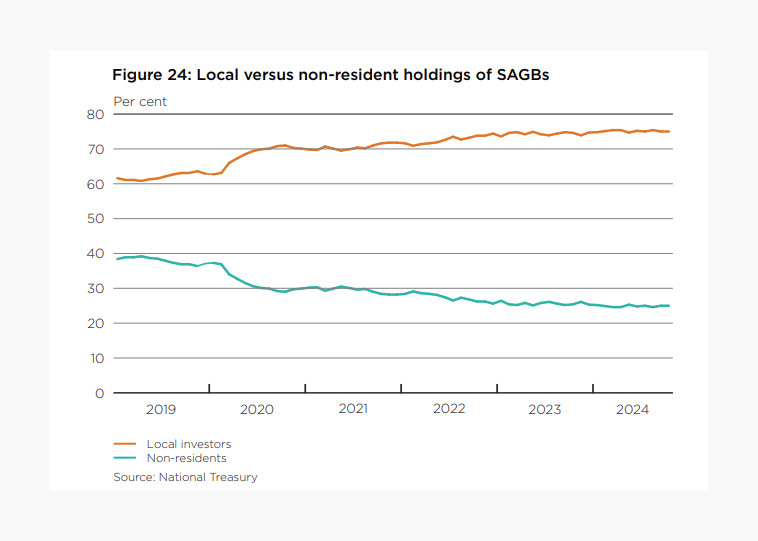

This is shown in the graph below.

Conversely, foreign investors have pumped R25.3 billion into government bonds so far in 2024, which has been seen as a vote of confidence in the new government.

Non-resident holdings of SAGBs increased marginally to 25% at the end of October 2024, up from 24.6% in April.

While non-residents have been net buyers of government bonds this year, their demand has lagged the pace of new debt issuance.

The government has had to increase its issuance of local debt to fund its deficit and also refinance existing debt as it comes due.

The structural decline in foreign participation in the government bond market is consistent with South Africa’s steadily declining share in major EM bond indices, such as the JPMorgan Government Bond Index for Emerging Markets.

South Africa has also been excluded from other major indices, including the WGBI in 2017.

So far in 2024, South African bonds have outperformed their global peers, delivering double-digit returns.

Investors are flocking to local-currency bonds as the domestic outlook improves and the US Federal Reserve cuts interest rates, setting the stage for even greater returns.

Yields on debt have also declined from 12.5% to around 10%, signalling increased confidence in the government’s efforts to rein in spending and limit the growth of its debt pile.

Stanlib’s head of fixed-income investments, Victor Mphaphuli, said there are still concerns about whether this is a false dawn and whether optimism can be sustained.

The key is economic growth. The entire investment landscape will change if the country can hit 3% of GDP growth per annum.

Mphaphuli went as far to say that yields on South African government bonds could hit single digits, if things go perfectly to plan.

“When a government borrows, it has to use that money for industrialisation and infrastructure to stimulate economic growth, create much-needed jobs and generate revenue to repay that debt,” he said.

“Instead, it spent its borrowings on building a patronage economy, with ANC support bolstered by expanding social grants and wage increases for a ballooning public service, including SOE employees. As a result, SA’s debt-to-GDP soared.”

“The only positive throughout this mounting crisis has been the discipline and stability of the Finance Ministry, which fought back to win back its credibility. The markets are starting to reward them for that,” Mphaphuli said.

Comments