Avoid running out of money when you retire

New actuarial research shows that most retirees need to consider higher equity exposure and lower drawdown rates to avoid running out of money.

Fellow of the Actuarial Society of South Africa (ASSA), Joao Frasco, analysed the performance of various retirement products over the past 20 years to compare which kind of investment is least likely to result in a retiree running out of money.

Frasco compared the performance of the JSE All Share Index (ALSI), an unnamed South African multi-asset (MA) high equity fund, a South African multi-asset (MA) low equity fund, and a local interest-bearing (IB) short-term fund which has no exposure to equity.

These four investment options were chosen to show the results along the investment risk spectrum available to South African investors.

Returns simulated for the unit trust funds are net of manager fees but do not reflect adviser or platform costs.

To account for fees and taxes, investors should increase the withdrawal rate by the corresponding percentage

This research aimed to investigate the possibility of a retiree running out of money with withdrawal rates ranging from 2.5% to 17.5% using different investment products.

The aim was to understand which combination of withdrawal rate and investment product was most likely to result in successful capital preservation over various time horizons for retirees.

Chances of retirees running out of money

Frasco’s research covered periods up to 35 years to make it useful for people at the start of their retirement and periods as low as five years for the elderly.

While withdrawal rates of 10% are generally unsustainable for most retirees irrespective of the investment strategy, this is not true for someone in their 80s and in poor health.

Frasco found that only retirees with a five-year investment horizon could avoid market volatility completely by opting for an interest-bearing fund.

However, this situation only applies to an investor with a very short life expectancy.

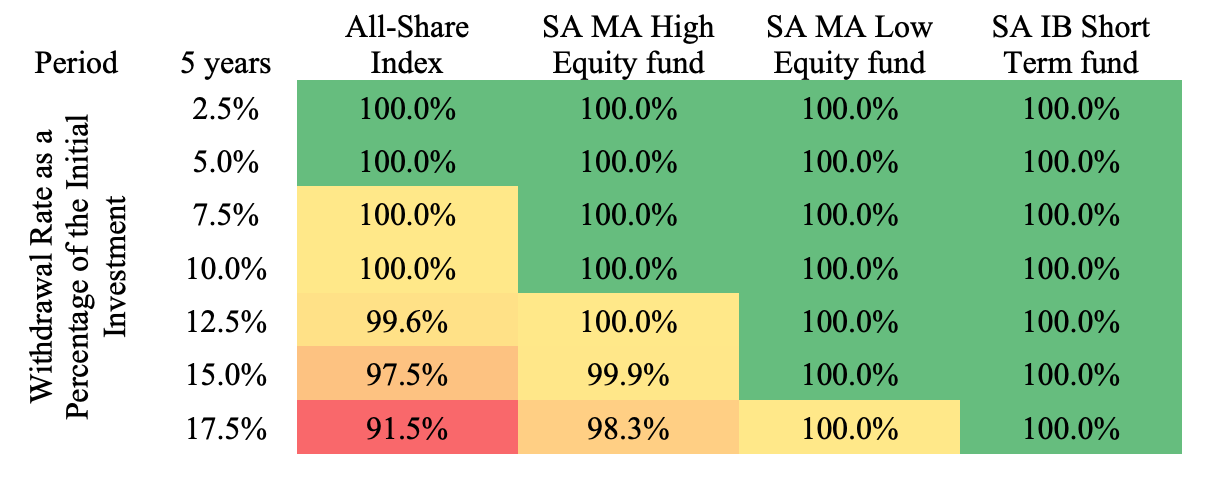

Over 5 years

Irrespective of the withdrawal rate selected, a living annuity invested in an SA interest-bearing fund will not run out of money over a five-year period.

The table below shows the probabilities of a retiree preserving their capital over five years with varying withdrawal rates.

For example, a retiree would preserve their capital 100% of the time, regardless of the withdrawal rate, if their capital was invested in a local interest-bearing fund.

On the other hand, if invested in a JSE All-Share index tracking fund, the retiree will only preserve their capital 91.5% of the time with a withdrawal rate of 17.5%.

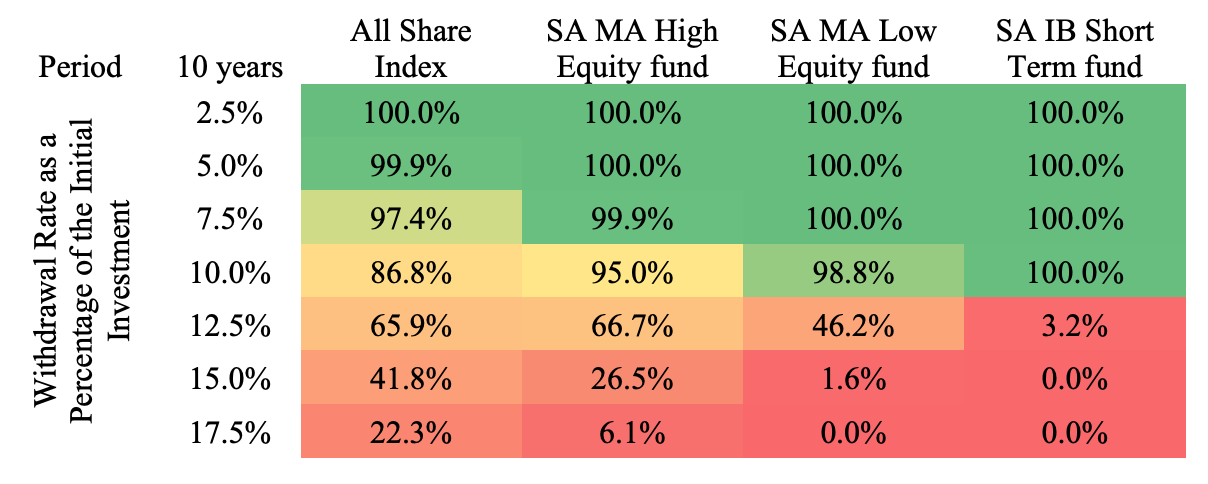

Over 10 years

Frasco’s research shows the outcomes change significantly if the investment period is extended to 10 years.

While the local interest-bearing fund has a 100% probability of success for withdrawal rates up to 10%, the success rate drops rapidly to only 3.2% for a withdrawal rate of 12.5%.

A high-equity investment, on the other hand, is likely to deliver a much higher probability of success.

At a withdrawal rate of 12.5%, a high equity investment has a probability of success of between 86.8% and 95%.

Frasco warned that investors would have to stomach a fair amount of volatility if their investment was highly exposed to equity.

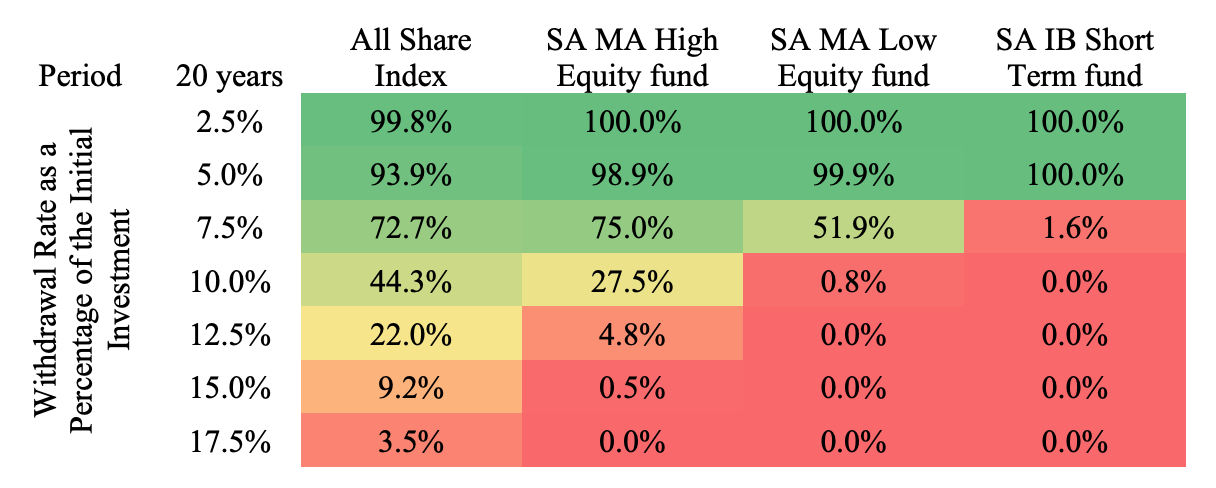

Over 20 years

Frasco explained that over 20 years, a withdrawal rate of up to 5% is unlikely to erode the living annuity capital, irrespective of the investment approach.

He says this is why withdrawal rates below 5% are usually considered sustainable.

However, if the withdrawal rate is increased to 7.5%, the likely success rate drops to a mere 1.6% if the capital is invested only in an interest-bearing fund, while a high equity exposure comes with a 75% probability of success.

This indicates the need for equity exposure for most investors looking to draw income at rates above 5%, said Frasco.

Over 25 years to 35 years

Frasco says periods up to 35 years were modelled for investors considering retiring and investing their capital in a living annuity at younger ages.

He adds that the younger the investor, the more important the investment strategy because younger people have a longer life expectancy.

The highest probability of not running out of money for a living annuity investor with a time horizon of 25 to 35 years would be maintaining a drawdown rate below 5%, with an equity exposure of up to 75%.

Comments