Johann Rupert’s ‘stepchild’ will have over R100 billion in the bank

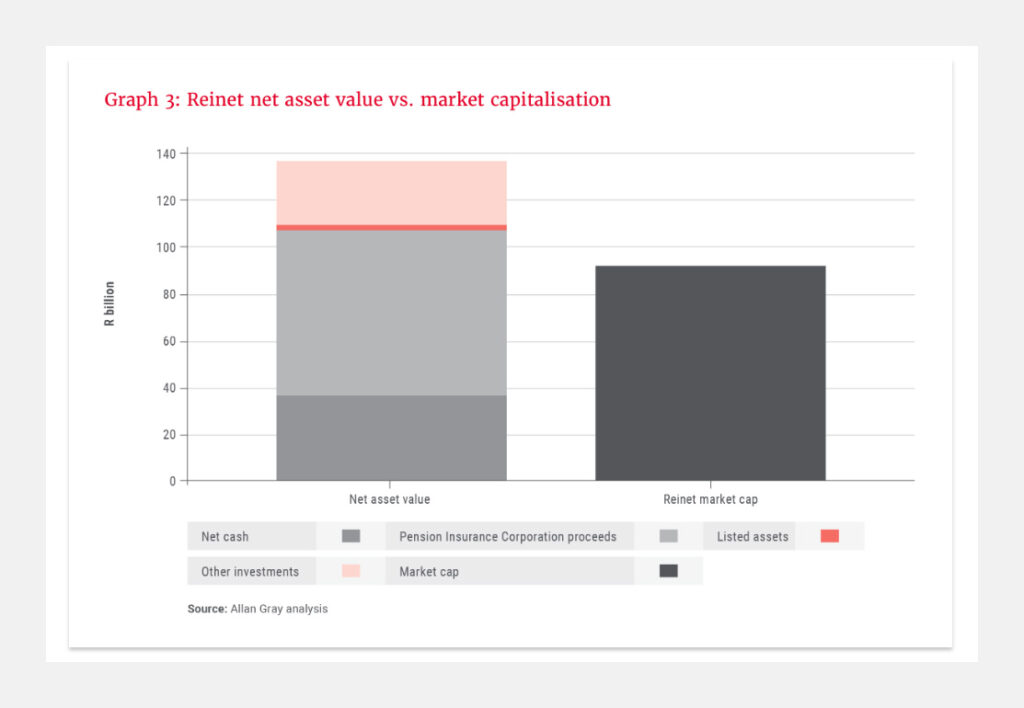

After the sale of its stake in Pension Insurance Corporation is concluded, Johann Rupert’s Reinet Investments will have more cash on its balance sheet than its market capitalisation.

This is a very unique situation for a company to find itself in and is one of the main reasons why Allan Gray finds the company an attractive investment proposition.

Having this amount of cash on hand gives Reinet the ability to make significant new investments or return billions in cash to shareholders through share buybacks or dividends.

Allan Gray analysts Jonty Fish and Malwande Nkonyane recently outlined the firm’s reasons for investing in Rupert’s investment holding companies, Remgro and Reinet.

Fish and Nkonyane explained that they are attracted to these companies due to the effective measures management is taking to close the discount at which they trade to their net asset values (NAV).

In the case of Reinet, this value unlock has come through several large deals to sell off the company’s investments in British American Tobacco (BAT) and Pension Insurance Corporation.

Reinet completely sold out of BAT in January 2025, netting itself R31.6 billion in cash, increasing the company’s liquid assets and marking a strategic pivot.

Reinet was created in 2008 after Richemont spun off its BAT stake into Luxembourg-based Reinet Investments following changes in Luxembourg tax laws.

Since then, the company has evolved into a diversified investment holding company, focused on its holdings in various listed and unlisted assets.

The sale of BAT was a long time coming, with Reinet investing heavily outside of tobacco to reduce its exposure to the industry.

Its most significant investment came in 2012 with a £400 million (around R5 billion at the time) stake in Pension Insurance Corporation, a specialist insurer focused on taking over defined benefit pension liabilities from British corporates.

The company’s clients include multinationals such as Rolls-Royce and TotalEnergies. Reinet’s investment has grown immensely over the past decade as employer sought to de-risk their defined benefit pension obligations.

By the end of 2021, Reinet had raised its stake in Pension Insurance Corporation to 49.5%, with the investment growing to accoutn for nearly half of the company’s NAV.

Fish and Nkonyane estimated the rate of return on this investment to be 13% per year in British pounds for Reinet. In comparison, the JSE All Share Index returned just 2.2% a year in pounds over the same period.

This made it a highly successful investment for Reinet, which the company is set to cash in on. It announced in the middle of 2025 that it would sell its stake in Pension Insurance Corporation for £5.9 billion (R141.3 billion at the time).

The analysts said this transaction will further boost Reinet’s balance sheet and make it a very compelling investment opportunity.

What makes it particularly compelling is that Reinet’s market capitalisation is now lower than the combination of its net cash and the potential proceeds from the Pension Insurance Corporation sale. This means the company is valued for less than its future cash balance by the market.

Challenges remain

Fish and Nkonyane explained some of the risks of investing in Reinet, despite its strong balance sheet and proven track record of solid returns.

The first issue the analysts pointed to was Reinet’s fee structure, with the company’s assets managed by its general partner, Reinet Investments Manager.

This manager charges shareholders a fixed annual management fee based on NAV and a performance fee based on total shareholder return over a one-year period.

These fees can erode shareholder value over time, particularly in periods of underperformance, the analysts said.

Another issue is Reinet’s private equity valuations, with the company having R14 billion in outstanding commitments to private equity funds as of the end of October.

Due to limited disclosure, these assets are difficult to value independently and are subject to valuation discounts by the market, Fish and Nkonyane said.

The current 33% discount to NAV already reflects investor scepticism regarding the private equity holdings. In fact, the market is effectively assigning zero value to these assets.

This also provides an opportunity for investors, with the zero value providing a margin of safety. If the private equity funds deliver returns, they could add substantial upside.

Probably the most significant issue for Fish and Nkonyane is the capital allocation uncertainty, which they referred to as the biggest unknown with regard to Reinet.

They said Reinet has multiple options through which it can pass value to shareholders. The uncertainty around which one they will eventually choose is a drawback.

Reinet’s options are as follows –

- Return capital to shareholders via buybacks or special dividends. Reinet’s management has shown a willingness to act when discounts become excessive. The current set-up, where the market capitalisation is below the value of liquid assets, creates a strong incentive for management to act again.

- Wind down the structure, distributing assets directly. Reinet may opt to wind down its structure and distribute assets directly, as the Investment Manager earns lower management fees on cash holdings and no fees on most private equity assets.

- Reinvest selectively. Reinet also has the option to invest in more transparent or liquid assets. By taking a long-term approach and identifying companies experiencing structural tailwinds, Reinet could generate value for shareholders.

Ultimately, Fish and Nkonyane said this uncertainty is a temporary factor, with Reinet having a proven track record of using shareholder capital extremely effectively.

Furthermore, the company has shown an appetite to take action to unlock the value held in the structure, indicating the future upside is likely.

For long-term investors, these discounts provide both a meaningful margin of safety and potential upside.

Comments