Hidden reason for elevated interest rates in South Africa

South Africa’s significant policy and fiscal risk is a major reason why the country’s interest rates remain relatively high, as the Reserve Bank has to compensate for this risk in protecting the value of the rand.

The risk premium attached to investing in South Africa means that interest rates have to be more than 2% higher to compensate.

This gap has also widened in recent years, with the country’s risk premium growing as the government’s financial health deteriorates and its credit rating declines.

However, there are signs that it is beginning to improve, with the risk premium easing slightly due to the National Treasury’s policy of fiscal consolidation and a reduction in structural constrains on growth.

This is feedback from Old Mutual Investment Group portfolio manager Jason Swartz, who outlined the asset manager’s views on a lower inflation target for the Reserve Bank.

Swartz said the Reserve Bank has built up significant credibility since inflation targeting was first introduced in 2000, keeping price increases largely within its 3% to 6% target range.

It plans to use this credibility to push inflation expectations lower amid talk of a lower inflation target of 3%. A slow adjustment in expectations is likely to result in economic pain for South Africa in the short term.

Swartz explained that a lower inflation target could see the Reserve Bank’s steady state for the repo rate decline to 5.5% from 7%, significantly boosting the local economy.

However, the Reserve Bank has consistently warned that elevated administered price increases and the country’s heightened risk premium prevent lower interest rates.

These factors may also threaten the move to a lower inflation target, with them largely being out of the control of the Reserve Bank.

Swartz said South Africa’s heightened risk premium is one of the major drivers behind the country’s relatively elevated interest rates.

The Reserve Bank has to compensate for this risk premium to attract capital to the country and support the value of the rand.

As the risk premium grows, interest rates have to compensate further by being relatively higher. This limits economic growth by keeping lending subdued.

The graph below shows the significant impact of the risk premium on interest rates in South Africa, with it growing from 1.5% in 2010 to nearly 2.5% in 2025.

Improved state finances are key

Swartz explained that the growing risk premium is largely a result of the state’s declining financial health over the past 15 years.

Since the 2007/08 financial year, when the government last ran a full budget surplus, it has posted successive deficits.

Government spending increased substantially, with little to show for it in terms of economic growth and improved tax revenue.

As a result, the deficits added up to create a significant debt burden, which crossed 75% of GDP in the 2023/24 financial year.

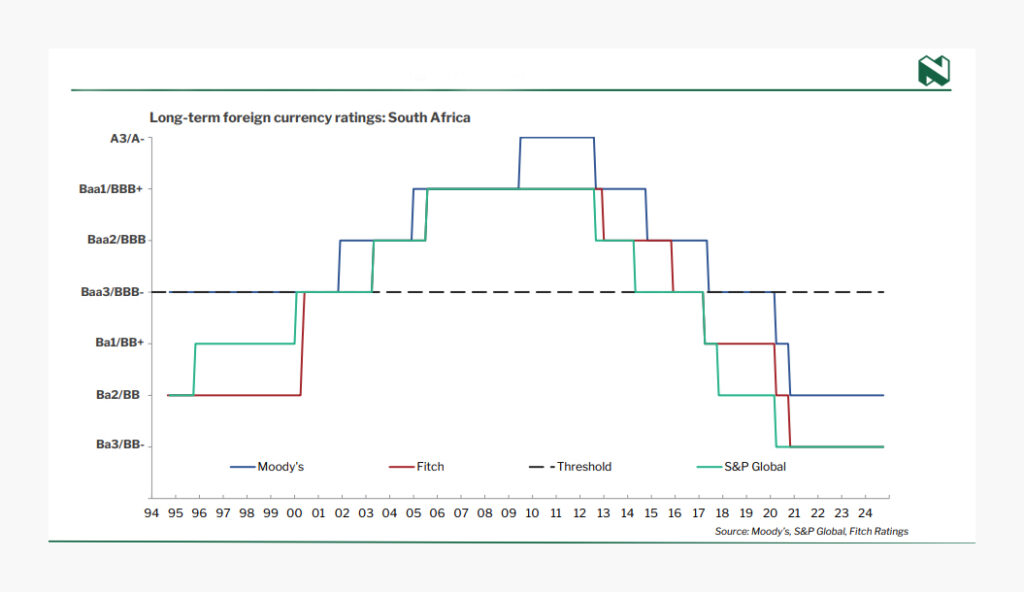

The deterioration of the state’s finances did not go unnoticed by ratings agencies, with all three downgrading South Africa steadily into sub-investment grade or ‘junk’ status.

Moody’s dropped South Africa two notches below investment grade, while Fitch and S&P rated the country three notches below investment grade.

Being placed into junk status prohibits many global pension funds and investment schemes from investing in South African assets, as they are considered ‘below investment grade’.

This resulted in significant outflows from South African assets over the past few years, significantly weakening the rand and further limiting economic growth.

However, there are signs that things are beginning to improve, with the National Treasury’s policy of fiscal consolidation paying off, albeit slowly.

With lacklustre growth, the National Treasury has taken to limiting increases in government spending to below inflation to generate a primary budget surplus.

A primary budget surplus means the state is bringing in more money in the form of tax revenue than it is spending, excluding debt-servicing costs.

This should result in the debt burden stabilising and gradually reducing as the state will not need to add to its debt burden and can use the surplus to begin paying down the principal amount.

As growth picks up, all other things being equal, the government’s debt-to-GDP ratio should decline. Furthermore, tax revenue should pick up and enable the state to pay down its debt.

This will reduce its debt-servicing costs, freeing up additional capital to invest in growing the economy or paying down its debt further.

South Africa is on track to kickstart this virtuous cycle, with the government on track to meet its target of a wider primary budget surplus.

If this trend continues, it is possible for South Africa’s credit rating to improve by two notches in the next three years.

Rating agencies will begin by shifting their outlook for the country from neutral to positive in either May or November 2025, with the first upgrade in 2026.

This is highly dependent on improved economic growth and the National Treasury keeping a tight lid on spending, particularly with regard to public sector wages and a potential basic income grant.

Comments