South Africa heading for financial disaster

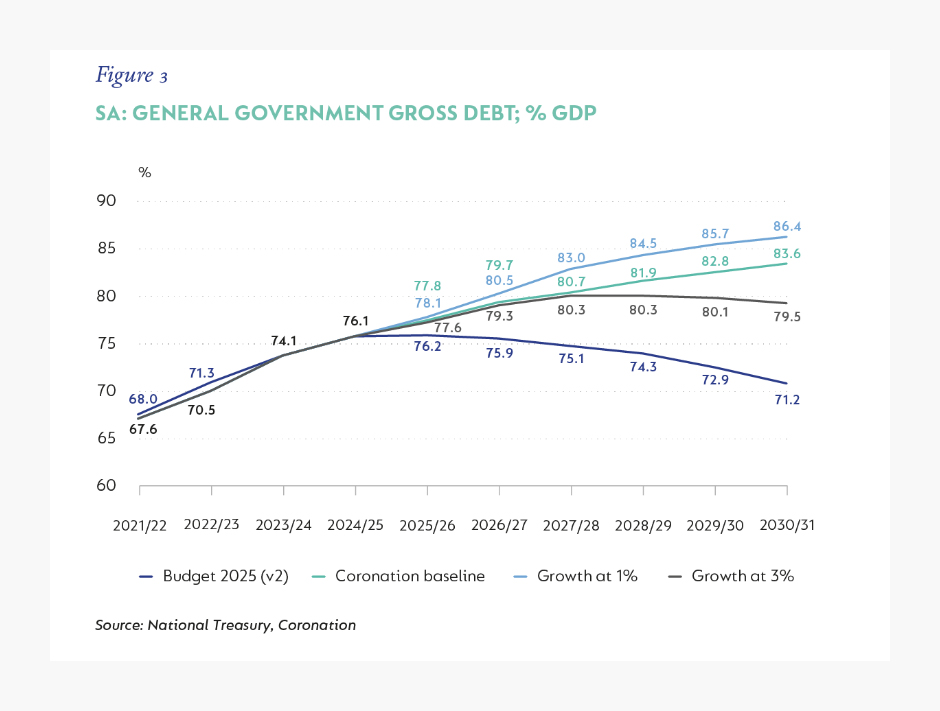

South Africa’s economy needs to grow at 3% per annum to stabilise the government’s debt load at around 80% of its GDP and gradually improve its financial health.

However, the economy has averaged an annual growth rate of 0.8% over the past decade and is expected to grow at an average of 1.5% for the next three years.

This lacklustre growth is at the core of South Africa’s financial mess, limiting tax revenue growth and exacerbating the country’s deteriorating debt-to-GDP ratio.

In a recent research note, Coronation’s head of fixed interest, Nishan Maharaj, outlined the country’s financial troubles, saying South Africa is facing a double blow from global tensions and domestic political uncertainty.

Maharaj explained that the two fundamental issues consistently constraining the performance of local bonds are the Reserve Bank’s restrictive monetary policy and precarious government finances.

The recent Budget turmoil, with the third iteration set to be presented to Parliament on 21 May, shows the difficulty of the decisions needed to resolve the government’s poor finances.

So far, the two proposed Budgets have appeared to stay on the National Treasury’s fiscal consolidation path by financing new expenditure through revenue increases.

However, the increased expenditure is recurring and fixed, implying any falloff in growth and thus tax revenue will create a larger funding shortfall, increasing the risks of a higher debt load going forward, Maharaj said.

In addition, the National Treasury accounts for its debt servicing costs on a cash basis versus traditional accrual accounting methods.

Maharaj explained that this implies that it sets up its debt accumulation forecasts for disappointment, that is, it accumulates more debt than it forecasts.

Therefore, the risks are heavily skewed towards a worse budget outcome going forward if economic growth does not recover significantly.

As shown in the graph below, the only sustainable solution is much faster economic growth, with a minimum of 3% per year needed to stabilise the government’s debt burden without severe spending cuts or tax hikes.

Impact of interest rates

A major issue with low growth in South Africa is that it has been coupled with elevated inflation and interest rates, making debt servicing more expensive.

As a result, the South African government’s interest rate on its debt is higher than the country’s economic growth, even in nominal terms.

This is unsustainable and means the country will eventually hit a fiscal cliff, where the economy will simply be unable to support the government’s debt burden.

The government borrows at an interest rate of around 9%, while nominal economic growth hovers around 5%.

Tax revenue will grow more or less in line with nominal economic growth over time, assuming a steady tax-to-GDP ratio.

This gap between interest rates and growth, sometimes expressed as r>g by economists, renders borrowing unsustainable since debt compounds faster than the income needed to service it.

This sits at the core of South Africa’s fiscal challenge, as debt-servicing costs are the fastest-growing expenditure item in the budget, with the government having to spend over R1 billion a day on interest payments.

Maharaj explained that it is not clear that the interest paid on government debt will come down meaningfully enough to alter this equation.

The combination of the likelihood of higher inflation in the coming years compared to the start of 2025 and investors likely to turn away from emerging market assets may push bond yields higher.

Real policy rates in South Africa are now at the most restrictive levels that they have been at since the early 2000s, when inflation was in double digits, growth was around 4%, and the country was only starting its inflation-targeting journey.

Inflation is now very much under control at 4.5%, but growth prospects remain in the doldrums, and it is not clear that elevated interest rates are the sole reason for this low growth.

Another major risk to the outlook is the sustainability of the Government of National Unity (GNU), which helped boost investor sentiment towards South Africa.

While we have not yet seen significant policy shifts, the presence of the DA in the coalition government was enough to halt deterioration, reduce slippage, and prioritise needed reforms, fostering an environment in which growth could accelerate towards 2%.

Maharaj said that, considering the recent developments regarding the Budget and other pieces of legislation, it seems very unlikely that the GNU will continue in its current form.

This will be a significant step back in the country’s recovery story and places the fiscal rehabilitation in great peril.

Comments