How much money you need to retire comfortably in South Africa

As a rule of thumb, South Africans must replace at least 75% of their final income at retirement age to retire comfortably.

This goal is difficult to achieve for most households and could be put at risk by withdrawing funds through the new two-pot system.

While no specific amount applies to all South Africans, many experts have provided guidance on how much one can save to retire comfortably.

Allan Gray’s Twanji Kalula recently explained that to retire comfortably, South Africans must replace at least 75% of their final income at retirement age.

This means they should save between 12% and 17% of their income from the day they start working.

Asset manager Ninety One has also completed an in-depth study into how investors should approach retirement income provision.

The study emphasised that choosing the right starting income level is vital to investors managing their risk of running out of money.

In short, a retiree should elect a starting income level of no more than 5% of their retirement capital. This is the amount they will draw down from their retirement investments.

With this starting income level of 5% of retirement capital as your standard, you require a capital lump sum equal to 20 times your final salary to invest in an income-producing annuity on retirement.

This is the amount required to generate an income equal to 100% of your final salary post-retirement.

Drawing no more than 5% will likely provide you with an inflation-adjusted income for 30 years, ensuring a comfortable retirement.

In simpler terms, to help your money last longer, you should take out only about 5% of your savings each year.

If you want to replace your whole salary after retirement, you’ll need a large lump sum – about 20 times what you earned. This should give you enough money to live on for 30 years.

For South Africans looking for a specific figure to aim for, research done by Just South Africa showed that the average South African household needs over R7 million to retire comfortably.

This is based on an average household income of R300,000 per annum.

Very few South Africans can afford to retire comfortably. FNB’s latest Retirement Insights Survey revealed that almost 50% of respondents do not have a retirement plan.

A survey from Allan Gray revealed that the average South African retiree can replace only 31% of their income with their retirement savings.

The survey data also revealed that only 9% of retirees manage to replace 80% or more of their pre-retirement income.

To address this challenge and avoid a retirement time bomb in South Africa, the government introduced the two-pot retirement system in September this year.

This new system mandates that all future contributions to retirement funds be divided into two components –

- Two-thirds of each contribution will go into a retirement ‘pot’, which must remain untouched until retirement.

- The remaining one-third will be directed into a savings ‘pot’, which allows for one withdrawal per tax year before retirement.

A separate ‘pot’ was also created for individuals with existing retirement funds to retain the value of all contributions made before the new system’s start date of 1 September.

While the savings component is designed to be accessed as a lump sum upon retirement, members can withdraw up to 100% of their savings component once per year before retirement. The minimum withdrawal amount is currently set at R2,000.

This new system is largely seen as a positive development for the industry. It aims to improve retirement outcomes by enhancing the preservation of funds until maturity while offering some flexibility by enabling access to cash from the savings component.

However, several asset managers have warned that withdrawing from the pot can significantly harm the returns on your retirement savings and said withdrawing retirement savings should only be exercised in emergencies.

Generally, it is rarely advisable for someone to withdraw money from their retirement savings, as doing so disrupts the compounding process that allows your money to grow until retirement.

Allan Gray’s Belinda Carbutt, a specialist in the company’s savings and investments team, used the example below to illustrate just how much South Africans stand to lose if they choose to withdraw from their retirement savings.

Example

On 31 August 2024, Siphokazi Kumalo’s pension balance was R100,000. On 1 September 2024, this amount was allocated to Siphokazi’s vested component.

Siphokazi’s savings component was then seeded with R10,000 – 10% of R100,000, capped at R30,000 – from her vested component.

This amount has been available for withdrawal since 1 September – excluding tax deducted at Siphokazi’s marginal tax rate and amounts owing to the South African Revenue Service.

However, Carbutt said it is important to note that this is not a “use it or lose it” scenario: The amount can remain invested until Siphokazi retires.

The vested component will now have a balance of R90,000.

Moving forward, the savings component will receive one-third of Siphokazi’s monthly contributions, with the remainder invested in the retirement component.

If Siphokazi’s retirement contribution in September 2024 is R3,000 per month, R1,000 will go to the savings component and R2,000 into the retirement component.

Siphokazi has the option of one withdrawal per tax year of at least R2,000, up to the full amount available in her savings component.

It is important to note that if Siphokazi decides to withdraw, her withdrawal will be taxed at her marginal tax rate. This tax is deducted before the withdrawal is paid to Siphokazi.

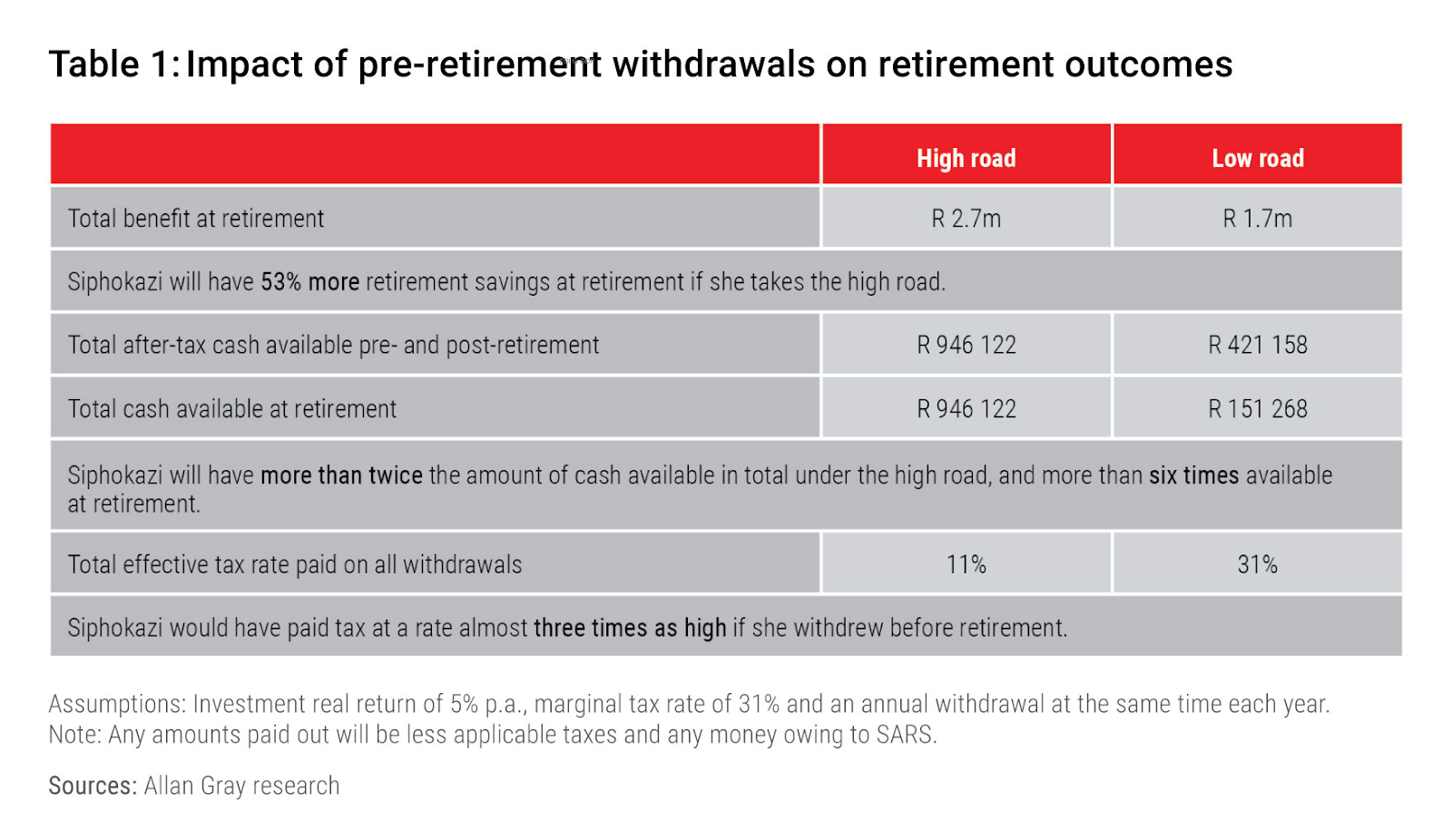

The table below, courtesy of Allan Gray, compares two different outcomes over the next 30 years until Siphokazi retires at age 55.

The high road is where Siphokazi stays focused on the long term and does not access her savings component. The low road is where she withdraws the available amount every year.

In summary, Carbutt said there are three important benefits of taking the high road:

- Compounding: Siphokazi has 53% more in retirement savings.

- Flexibility: Siphokazi has an option to take a cash portion at retirement. This will be six times greater than the amount in cash she would have received if she were to withdraw monthly before retirement.

- Tax savings: Siphokazi will have an effective tax rate of 11% by staying focused on the high road compared to 31% (her marginal tax rate) for cashing in her savings component in the low road scenario. This equates to paying a third less in tax.

“The new system gives you flexibility; however, it is this flexibility that can also undo your long-term financial strategy,” Carbutt warned.

Comments