South African asset managers set to take big hit in September

New research revealed that almost 60% of South Africans said they would access funds from their two-pot savings component when the new system kicks in in September this year.

Sanlam has released some of the findings from its Benchmark research, which sets an annual benchmark for the nation’s financial mood.

With the two-pot system and National Health Insurance top of mind this year, the research focuses on health and wealth.

South Africa’s new two-pot retirement system allows members to access a portion of their savings for emergencies while keeping the rest locked away for retirement.

President Cyril Ramaphosa signed the Revenue Laws Amendment Bill into law at the start of June, establishing the “two-pot” retirement system.

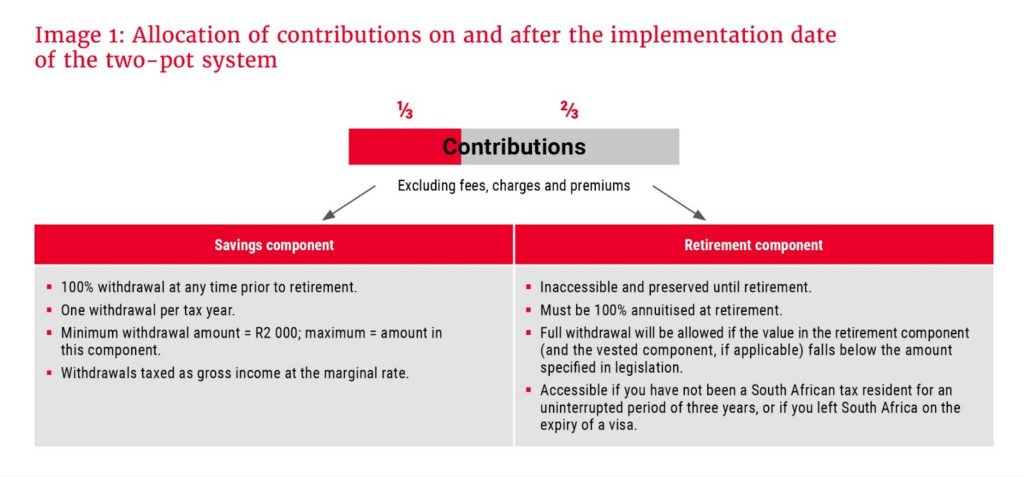

Simply put, the new two-pot retirement system changes how your retirement savings are managed – instead of one big pot, your contributions will be split into two.

One-third goes into a more accessible savings pot you can tap into once a year for emergencies. This pot gets an initial boost from a portion of your existing savings.

The remaining two-thirds go into a retirement pot that is locked away until you retire, ensuring you have a bigger nest egg for your golden years.

This system is designed to promote long-term savings while offering some flexibility to handle unexpected situations.

In 2022, Sanlam Benchmark research found just 31% of respondents said they would access funds from their two-pot savings component. In 2024, this number jumped to 59%.

“Two-pot may address the problems of the present, but in a nation where under 10% of the population can afford to retire comfortably, what will the ramifications be later?” Sanlam Corporate CEO Kanyisa Mkhize said.

Research indicates that rising financial pressures on consumers have led 50% of respondents to cash in all their retirement funds. This marks a regression from the 35% who did so in 2023.

“These findings underscore the importance of the two-pot system, which aims to encourage and maintain savings throughout an individual’s career,” she said.

“However, well-intended regulatory changes can have dire consequences down the line depending on execution. Clear communication, meticulous planning and implementation are needed to ensure that policies achieve their goals without unintended negative consequences.”

Warning for asset managers

Old Mutual CEO Iain Williamson has warned that the new two-pot retirement system will result in significant outflows from retirement funds in the short term but may benefit the industry long term.

Implementing the new two-pot retirement system on 1 September 2024 poses a risk to Old Mutual as one of the country’s largest administrators of retirement funds.

Williamson said implementing this system will inevitably result in material outflows from retirement funds in the short term.

“We expect to see material outflows from the effective date for a few months and then a gradual slow down to a steady state,” he said.

Williamson told News24 earlier this year that it expects its clients to withdraw R14.2 billion when the two-pot retirement system takes effect on 1 September.

He said the average withdrawal from funds Old Mutual manages and oversees is expected to be around R12,000.

This has the potential to significantly impact the earnings of asset managers who are heavily exposed to retirement products.

However, Williamson said the reforms will be positive for the industry in the long run, as they will encourage South Africans to invest most of their savings in retirement.

Many industry stakeholders have also critiqued the tight deadline the government set for the new two-pot system, leaving asset managers little time to prepare for the expected massive outflows.

A major risk with this tight deadline is that the system’s implementation is rushed, increasing the chances of delays, errors, and savers’ lack of understanding of the changes to the system.

Product development actuary at Coronation Rael Bloom said earlier this year that this may result in discontent among retirees and undermine confidence in the retirement industry.

However, the most significant risk lies in the rapid withdrawal of money from the system once South Africans can withdraw from their “savings pot”.

Bloom outlined what happened in the Chilean retirement market during the COVID-19 pandemic, highlighting the risks of creating an expectation for recurring lump sum withdrawals.

Before the pandemic, Chile’s pension system was generally well-regarded. However, it was decimated following a series of Covid-19-related withdrawals, with over $50 billion flowing out of the system.

In contrast, Australia also allowed emergency withdrawals from Superannuation funds during Covid, but only under very specific and limited means-tested conditions.

This protected the integrity of the Australian system, allowing it to recover once the immediate needs of the pandemic had passed.

Comments