It could be worse – Lesetja Kganyago

South African Reserve Bank Governor Lesetja Kganyago explained that, while the country now faces elevated uncertainty and a potential inflation shock, it could be worse.

This is because, prior to the outbreak of the Iran war, South Africa was on a broadly positive trajectory.

The inflation rate was at the new target, the rand was strong, and the Reserve Bank was taking a cautious and credible approach to monetary policy.

Therefore, South Africa can now afford to look through the first-round effects of the Middle East conflict and react to any second-round effects as they come up.

However, Kganyago said this does not mean South Africa is immune to the impact of the conflict, with some pain inevitable.

“There is nothing South Africa did to create this problem. At the same time, it is our problem to deal with,” he said.

“As a small open economy, and as an oil importer, we are going to get hurt. Our job as policymakers is to minimise the pain, keeping focused on our long-run objectives.”

Crucially, Kganyago explained that the war will impact South Africa’s transition to its new, lower inflation target.

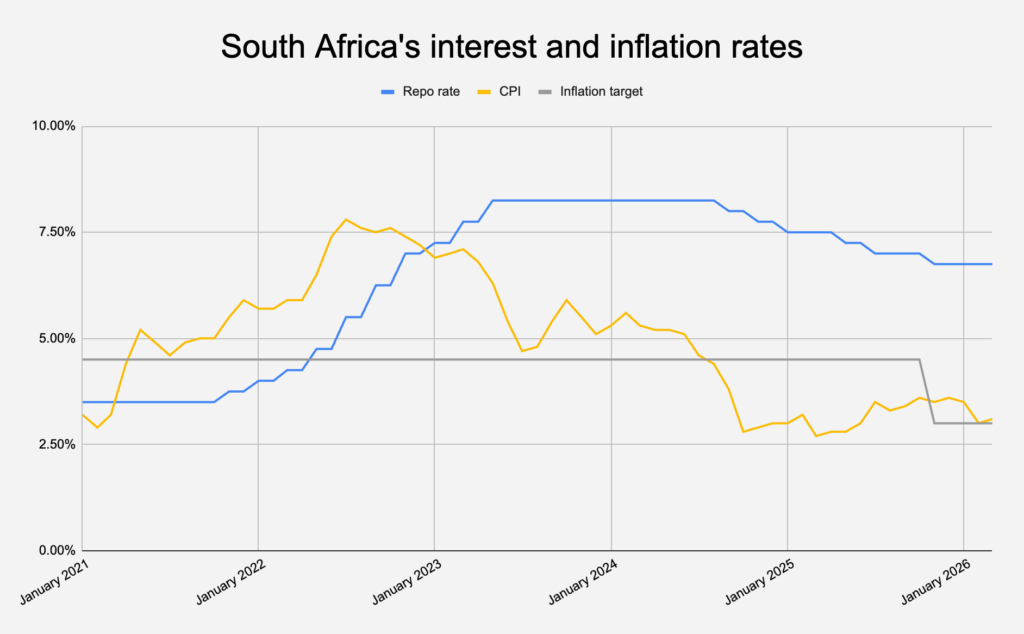

In November 2025, the National Treasury officially lowered its inflation target from a range of 3% to 6% to a lower, more narrow target of 3%, with a one percentage point tolerance band.

Kganyago said that, prior to the US/Israel invasion of Iran, South Africa’s transition to the new target was going “about as smoothly as we could have hoped”.

The CPI inflation rate peaked at 3.6% in December, and moved down to 3.5% in January and even lower to 3% in February.

Inflation expectations were not yet firmly anchored at 3%, though they were trending downward.

“The new target is less than a year old. We have made good progress in that time, building credibility at 3%, but we have not completed the journey,” Kganyago said.

“Overall, it is not the ideal starting point, but it could be worse.”

Interest rates

Kganyago said the South African Reserve Bank’s approach to monetary policy over the past year should help the country better navigate the impact of the Middle East war.

“This crisis is finding us with policy moderately restrictive and with inflation at target. Real rates may be falling as inflation rises, but we also have tighter financial conditions,” he said.

He explained that, while setting the country’s monetary policy over the past year and as it started the transition to a new inflation target, the Reserve Bank has kept potential risks top of mind.

“We did not know exactly what was going to go wrong, but there seemed to be too many things that could go wrong,” he said.

The awareness of potential risks made the Reserve Bank take a cautious approach to monetary policy, including not cutting rates at every meeting and, when it did, sticking to smaller 25 basis point cuts.

“This meant our policy stance was not immediately rendered obsolete when trouble did come with the conflict in the Middle East and the closure of the Strait of Hormuz,” the governor said.

“We had inflation at exactly 3%, with core also at 3%, in line with our new target. This was a reasonably good starting point for confronting a severe shock.”

This cautious approach not only put South Africa in a stronger position from an inflation perspective, but also improved the Reserve Bank’s credibility, which is critical when trying to navigate a crisis of this kind.

“Credibility”, in this context, essentially means that everyone trusts inflation will revert to target soon.

However, Kganyago emphasised that monetary policy is never simple, and there are many potential pitfalls lying ahead.

For example, he pointed out that “shocks have a bad habit of travelling in groups”, meaning the decision to look through one shock could come back to bite if more shocks were to follow.

“It is unfortunate that this shock is hitting during the transition to the new, lower inflation target. Until now, that transition was going about as smoothly as we could have hoped,” he said.

“It seemed we were going to complete the disinflation soon, perhaps this year. Now this process will take longer.”

However, he said it is still a “big plus” that this shock comes at a time when South Africa is seeing record-low inflation expectations and monetary policy credibility is as strong as it has ever been.

“These gains are valuable, and we do not intend to lose them,” he said. “If we do have to raise rates, it will be to sustain low and stable inflation, and all the benefits that brings.”

“The lower target helped give us lower borrowing costs and a stronger rand. Some of those gains were reversed with the shock, but not fully and not for long.”

Comments