South Africa heading for the eye of the storm

South Africa is heading for an inflationary shock caused by surging fuel prices amid disrupted oil supply from the Middle East.

The Reserve Bank is set to navigate South Africa through this storm, which may see inflation surge outside the one percentage point tolerance band around the 3% inflation target.

This is likely to result in the end of the bank’s interest rate cutting cycle and may result in hikes if the conflict in the Middle East is prolonged.

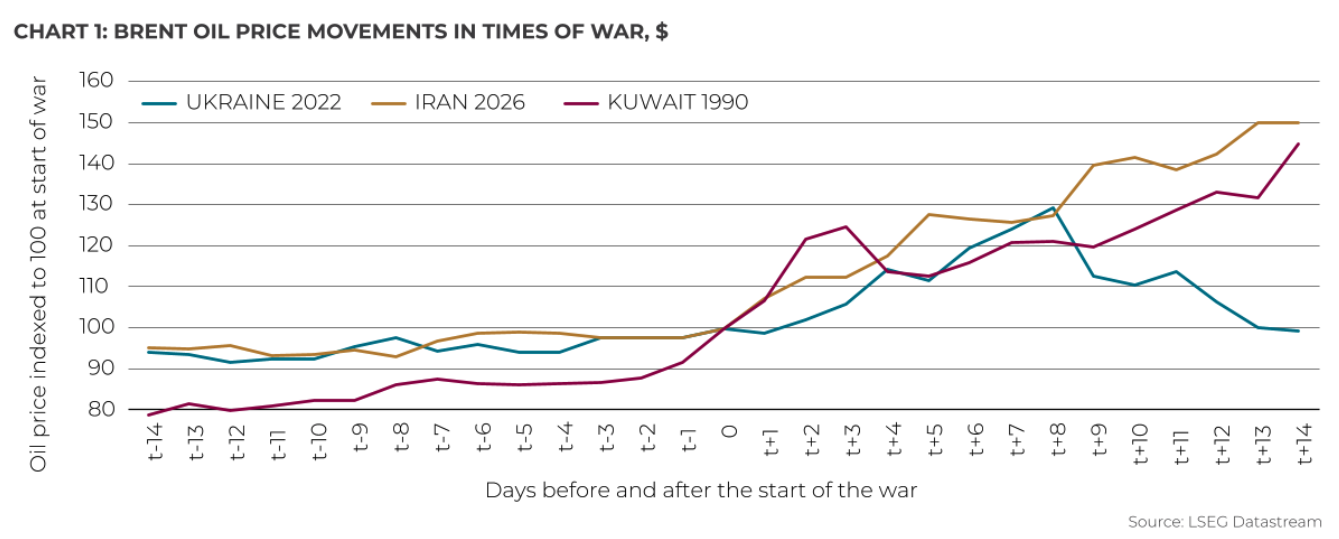

However, Symmetry chief investment strategist Izak Odendaal explained that reality is not that simple, with the shock from the Middle East conflict being nothing like historical examples.

Odendaal said the Reserve Bank has been exceptionally good at avoiding many of the pitfalls that other central banks fall into by being backwards-looking and their tendency to be scarred by past mistakes.

This leads them to treat most episodes of surging inflation in the same way, without clearly analysing what caused the surge in the first place.

For example, when inflation surged post-pandemic and the Russia-Ukraine war started, many central banks in the developed world remained focused on the prior decade of low inflation. As a result, they missed how quickly inflationary pressures were building.

After initially dismissing inflation as “transitory”, monetary policymakers were forced into catching up by hiking interest rates aggressively.

Higher interest rates sent markets crashing in 2022 and compounded the misery of the cost-of-living shock for households.

Central banks are at risk of making the same mistake today, fearing the inflationary impact of rising oil prices more than their impact on economic growth. Thus, they would raise rates.

“It would be an error, since the backdrop is different to 2022. The Middle East supplies much more oil than Russia. Therefore, the potential of the oil price shock is large, but the broader environment is different,” Odendaal explained.

South Africa’s latest inflation data predates the war in Iran. As such, petrol price inflation slowed by 10% in February and helped inflation hit the Reserve Bank’s 3% target.

However, Odendaal estimated that fuel price inflation will accelerate to around 16% in April, once the R4.80 per litre petrol price hike is reflected. Crucially, fuel prices have a relatively small weighting in the consumer price index (CPI).

Fuel’s direct weight in the CPI basket is only 3.8%, meaning that it will directly add between 0.6 and 1 percentage point to headline inflation in April, if current price hikes hold.

The eye of the storm

Odendaal explained that central banks have effective tools to respond to demand-led inflation, which make up the majority of cases when it comes to inflationary shocks.

However, supply shocks, such as the war in Iran, are a different matter, and the current episode is the worst supply shock in decades.

“Central banks can do nothing about oil supply – they don’t drill wells or build pipelines. Therefore, the textbook response to inflation caused by fuel price spikes is to focus on the behaviour of firms and consumers,” Odendaal explained.

“If companies pass on higher transport costs to consumers, inflationary pressures can broaden, known as the second-round effect. This will depend on several factors, with the main one being the duration of the oil price spike.”

Most companies will be hesitant to immediately raise prices for fear that a competitor could undercut them, but they can also only absorb price pressure for a limited time.

“When companies start raising prices, there is a risk that it becomes self-sustaining if consumers in turn start believing that higher inflation is here to stay,” Odendaal said.

“Central banks, therefore, pay attention to the long-term inflation expectations of participants in the economy. If households, businesses and workers believe that inflation will eventually settle down again, there is little to worry about.”

“However, if these expectations become unmoored, central banks are more likely to act decisively, taking away the punchbowl to prevent the party from even starting.”

In practical terms, this means the Reserve Bank will watch how “core” inflation behaves, more than headline inflation.

Core inflation excludes volatile food and fuel prices, not because they don’t matter to consumers, but because they are volatile and tell us little about underlying inflationary pressures.

Crucially, in South Africa, raising interest rates has a larger impact on the economy as bank lending plays a larger role, Odendaal said.

There is some comfort in the fact that, on the eve of this global shock hitting its shores, South Africa’s inflation picture was benign and called for further interest rate cuts.

Headline consumer inflation came in lower than expected in February, with a year-on-year reading of 3%. Core inflation was also 3%.

Comments