Alarm bells ringing for the rand

While the rand has recovered somewhat after an apparent de-escalation in the Middle East conflict, uncertainty and risk-off sentiment in financial markets remain.

This has put emerging market currencies like the rand at a disadvantage, particularly as the US dollar continues to act as a safe-haven asset amid the turmoil.

Investec chief economist Annabel Bishop explained that the rand has depreciated over the past month due to market concerns over the war in the Middle East.

In particular, financial markets have been rattled by the length of interruption to shipping in the Strait of Hormuz, a key shipping corridor through which around 20% of the world’s oil supply is transported.

These concerns have led to sky-high oil prices and supply concerns, as well as a risk-off sentiment in global financial markets.

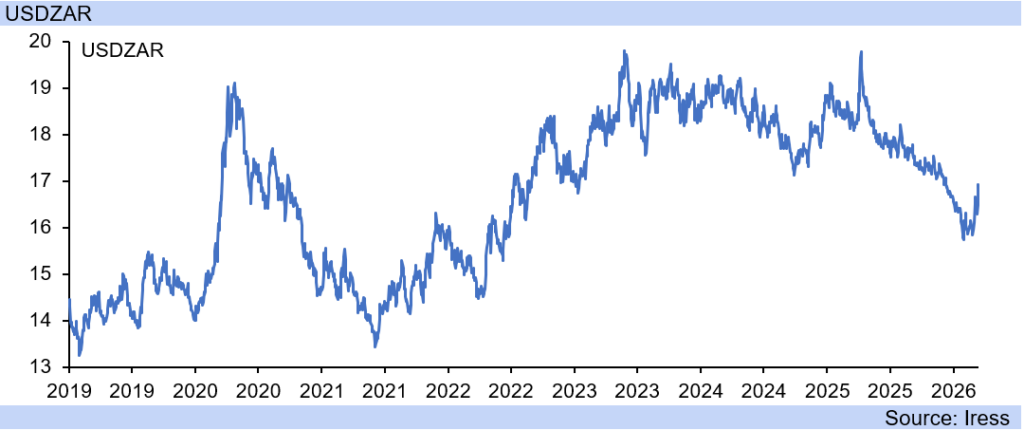

The rand has taken a hit from this risk-averse sentiment, weakening to levels last seen in November 2025.

This is also partly due to the US dollar emerging as a safe-haven asset during the conflict, which has put pressure on the rand.

The local currency rose to R17.25/USD on Monday, 23 March, but recovered slightly to under R17/USD later in the day after United States President Donald Trump announced that he would postpone threatened strikes in Iran following “constructive conversations”.

It should be noted that Iran later denied that these conversations took place, which saw prices rise again slightly.

Regardless, Bishop said the rand will remain vulnerable to shifts in global financial market sentiment, with the intensification of the Middle East war worsening risk-off sentiment.

This, she said, has effectively caused the rand to weaken further by close to 5.0% since the start of the war.

A stronger dollar and risk-off sentiment have been compounded by changing interest rate expectations, with the Reserve Bank set to hold its next meeting on Thursday, 26 March.

Bishop explained that markets are currently looking for hikes, not cuts, in interest rate cycles, which is also weakening the rand.

Inflation concerns

Bishop said the Middle East conflict is also expected to impact inflation in South Africa, particularly due to the Strait of Hormuz.

The Strait’s effective closure has seen global oil prices rise significantly, which severely affects South Africa’s economic cost base.

Bishop explained that economies are energy-intensive, and South Africa’s supply chain, in particular, is heavily diesel-intensive.

Aside from diesel and other fuels, a large percentage of the country’s fertiliser supply is also transported through the Strait of Hormuz.

She pointed out that fertiliser costs have already risen, and considering South Africa imports around 80% of its fertiliser, this has far-reaching consequences for the entire economy.

The Southern Africa Agri Initiative has explained that fertiliser typically accounts for 35% to 50% of production costs for grain and other key crops.

Therefore, a shortage of fertiliser or higher prices could lead to reduced application rates, lower yields on fertiliser-intensive crops like maize, as well as elevated food prices for consumers.

These implications have, in turn, elevated concerns about South Africa’s inflation, with food inflation being a major contributor to the country’s consumer price index.

In recent months, red meat inflation has soared amid a foot-and-mouth disease outbreak among South African cattle, but this has been offset by low field crop prices.

Now, meat prices have eased slightly, though they remain high, and swine fever is affecting pork prices. Along with concerns for grains and other fertiliser-intensive crops, food inflation could accelerate significantly in the coming months.

These risks to the inflation outlook, along with high oil prices and a weak rand, have dashed many economists’ hopes for an interest rate cut in March, with some even expecting a hike.

In Bishop’s base case for interest rates, she sees the repo rate remaining unchanged in the second quarter of 2026, with a 25-basis-point cut in the third quarter of the year.

Comments