The calm before the storm in South Africa

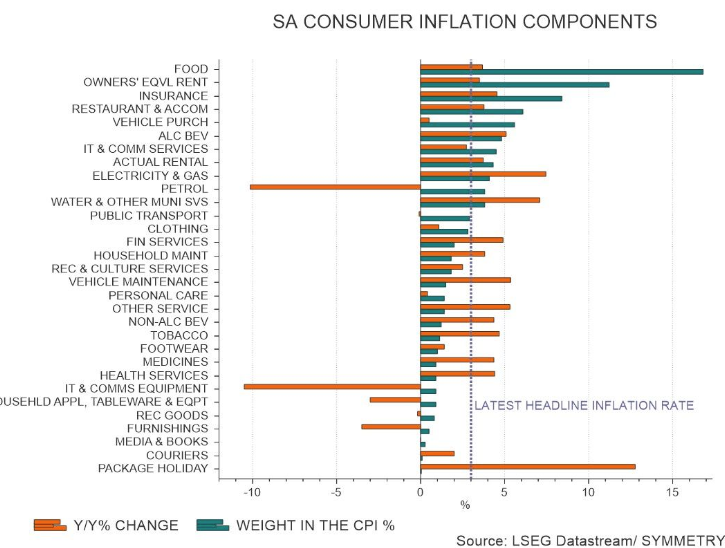

South Africa’s latest inflation reading came in lower than expectations, with a year-on-year reading of 3% for February.

However, this is the calm before the storm that is coming from the war in the Middle East, which is set to see petrol and diesel prices rise by around 20%.

The key question is whether this will translate into significant price increases in the rest of the South African economy, making an otherwise temporary shock into a prolonged period of elevated inflation.

Even the outside chance of this is enough for the Reserve Bank’s Monetary Policy Committee to hold interest rates where they are at its upcoming meeting at the end of March.

The bank will wait to see how long the war and the disruptions to oil supply from the Middle East will last, and whether the rise in fuel prices results in increases across the economy.

This is feedback from Symmetry chief investment strategist Izak Odendaal, who explained that the second-round effect is significantly more important than the initial shock.

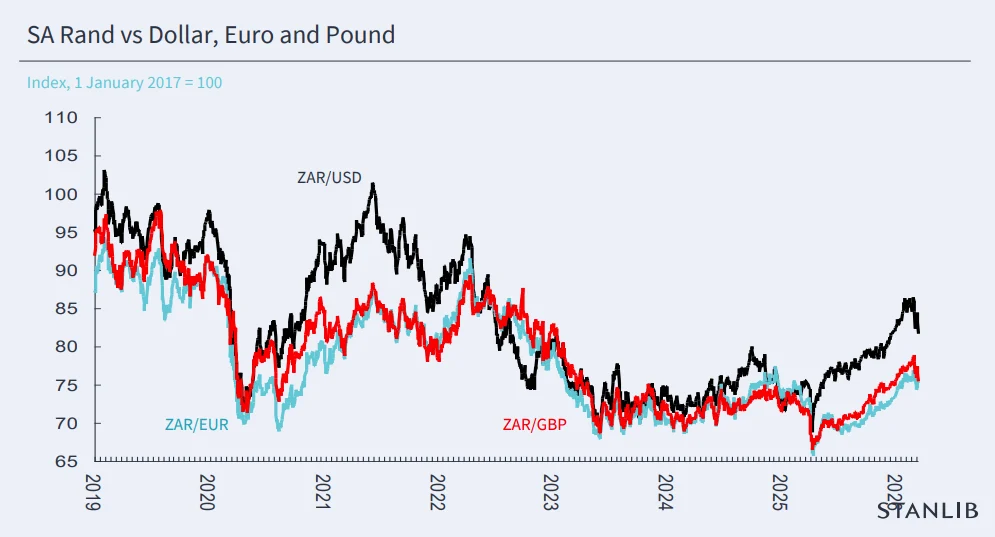

Since the US-Israeli strikes on Iran and subsequent retaliation, the price of oil has risen by nearly 50%, and the rand has weakened by around 5%.

This combination is enough to send fuel price projections soaring in South Africa, with the Central Energy Fund forecasting record increases for all grades of petrol and diesel.

These rising prices, which are almost inevitable, will have significant implications for inflation in South Africa, with some concerned that the Reserve Bank may even hike interest rates to limit the effect.

Odendaal said hikes are unlikely, with the Reserve Bank set to ‘look through’ the initial increase from rising fuel prices and watch for signs that other prices are rising in the economy.

South Africa’s latest inflation data predates the war in Iran. As such, petrol price inflation slowed by 10% in February and helped inflation hit the Reserve Bank’s 3% target.

However, Odendaal estimated that fuel price inflation will accelerate to around 16% in April, once the R4.80 per litre petrol price hike reflects. Crucially, fuel prices have a relatively small weighting in the Consumer Price Index (CPI).

Fuel’s direct weight in the CPI basket is only 3.8%, meaning that it will directly add between 0.6 and 1 percentage point to headline inflation in April, if current price hikes hold.

The other 96%

The key issue for the Reserve Bank will be about what happens with the other 96% of the CPI basket, with fuel inflation proving highly volatile and unlikely to stick.

Stanlib chief economist Kevin Lings has done an analysis of the history of fuel inflation in South Africa, with it proving to be extremely volatile.

Since 2005, South Africa’s annual rate of petrol inflation has ranged between a low of -26.7% to a high of 53.8%. It has also only been between 0% and 10% for 67 months.

This means that, over the past 21 years, South Africa’s fuel inflation rate has either been in deflation or above 10% for 73% of the time.

In other words, it is unusual for fuel inflation to be between 0% and 10%, and incredibly rare for it to be between 3% and 6%.

This indicates that elevated fuel inflation is unlikely to stick and justifies the Reserve Bank’s preference to look through to second-round effects that are stickier.

“The South African economy has experienced numerous fuel price shocks over the past 21 years. While the size of the shock is important, the duration of the shock has a much more pronounced impact on the economy,” Lings said.

The longer fuel prices remain elevated and, crucially, keep rising, the more likely and severe second-round effects become.

“Companies are unlikely to immediately raise prices, but will struggle to hold out for more than six months or so,” Odendaal explained.

The rand’s behaviour is also important to the Reserve Bank, as it has a much broader impact on prices, affecting all imported goods, not just fuel.

The rand is the third-worst-performing emerging market currency in March, while others are enjoying a resurgence on the back of elevated oil prices.

Countries like Nigeria and Angola are expected to benefit from elevated oil prices and disruption in supply from the Middle East, boosting their state finances and currencies.

However, Odendaal said the good news is that, on the eve of this global shock hitting our shores, the South African inflation picture was benign, calling for further interest rate cuts.

Once the storm passes, Odendaal is hopeful that South Africa can return to this status quo.

Comments