Eleven reasons Dawie Roodt is optimistic about South Africa

Economist Dawie Roodt said that while there is still a lot of work to be done, it seems as though South Africa is staging a turnaround, with several factors working in the country’s favour.

At the Efficient Group’s 2026 Budget Highlights event held on Wednesday, 25 February, Roodt outlined his views on South Africa’s latest national budget.

Tabled on the same day, the 2026 Budget has been relatively well-received among economists and financial experts, who have applauded Finance Minister Enoch Godongwana’s fiscal consolidation efforts.

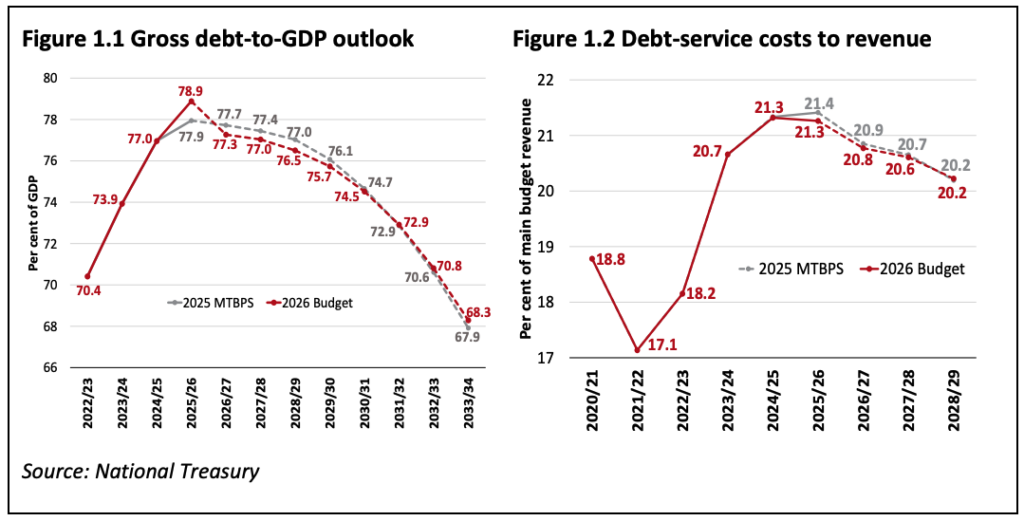

Considered one of South Africa’s most positive budgets in years, the 2026 Budget showed that the state’s gross debt-to-GDP ratio will stabilise in the 2025/26 fiscal year at 78.9%, and is expected to decline in the coming years.

In addition, a commodity boom, which upped corporate income tax, and the South African Revenue Service’s (SARS) collection efforts significantly provided a much-needed revenue boost.

This meant the National Treasury could avoid hiking the country’s major taxes, like value-added tax (VAT), providing relief to South Africa’s overburdened tax base.

Various other relief measures were also introduced, including raising the annual limit for tax-free investment, increasing the VAT registration threshold for businesses, and adjusting personal income tax brackets for inflation.

On top of this, the government managed to rein in its spending in the 2025/26 fiscal year and will continue to do so in the Medium-Term Expenditure Framework, as fiscal consolidation efforts continue.

All of this has put South Africa on a far healthier fiscal trajectory than just a few years ago, and has given many economists, including Roodt, reason to believe that the country has turned the corner.

Dawie Roodt’s 11 reasons

Revenue overrun

The first reason Roodt listed was South Africa’s expected revenue overrun of over R20 billion.

Godongwana announced in his Budget Speech that gross tax revenue for 2025/26 is expected to reach R2.01 trillion, which is R21.3 billion above the 2025 Budget estimates.

Roodt said he actually believes the overrun could be higher, attributing the surplus to a “very aggressive SARS and the commodity boom that boosted the government’s corporate income tax take.

“So, there is more money available to the Minister of Finance and, may I say, I think he used this extra money quite wisely,” he said.

Weak, but better growth

Roodt’s second reason was that South Africa appears to be on a stronger economic growth path, though he noted that GDP growth remains weak.

Godongwana projected GDP growth of 1.6% for 2026, which Roodt described as a “shame”, saying South Africa should be aiming for much higher growth.

However, he said it is positive that South Africa is set to achieve growth above 1%, after being stuck at sub-1% for the past few years.

He explained that above 1% growth means the economy is growing as roughly the same rate as the population, “which means we’re probably not going to get poorer but certainly won’t be getting richer”.

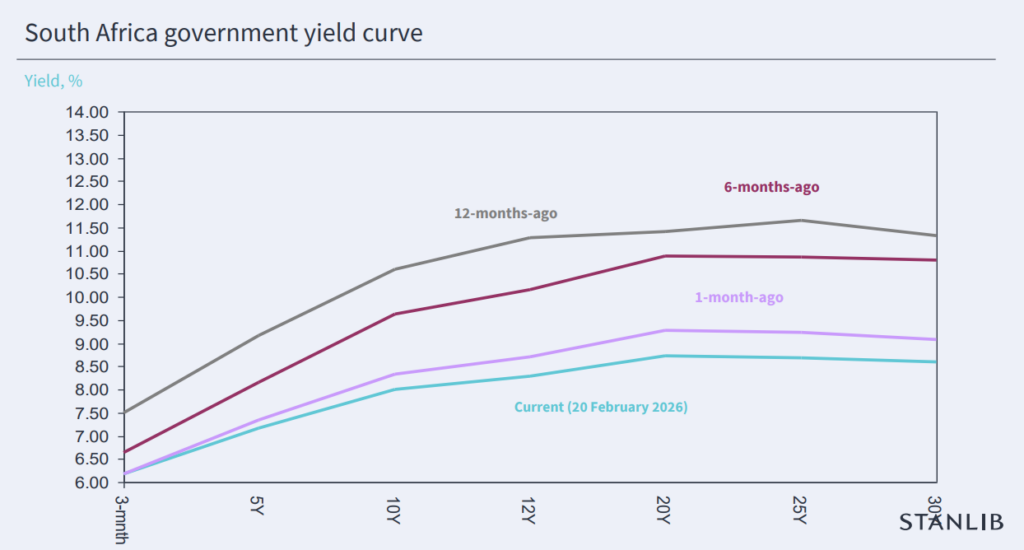

Much lower bond yields

Roodt pointed out that South African bond yields came down a lot in 2025, which he attributed largely to the country’s lower inflation target.

In November 2025, Godongwana agreed to lower the Reserve Bank’s inflation target to 3%, with a one percentage point tolerance band.

This is both lower and narrower than the previous target range of 3% to 6%, bringing South Africa more in line with its global peers.

While Roodt explained that Godongwana was “forced” to change the target, he said the outcome is positive, as it removes much of the risk from investing in South Africa.

He said this lower risk perception has led to foreign investors buying more of the country’s bonds and equities, which has also boosted the rand and created an opportunity for the Reserve Bank to cut interest rates.

However, he noted that the full impact of lower bond yields will only be felt in future years, as interest rates are already locked in for debt that was incurred in previous years.

“But now, as we go ahead and the Minister of Finance borrows new money in the market, that will be funded at lower interest rates,” he said.

Equities rally

Roodt explained that the lower risk associated with investing in South Africa also encouraged investors to buy local equities.

This, along with the commodity boom that boosted JSE-listed mining stocks, saw the JSE ALSI rise by nearly 40% in 2025.

Mining companies benefited the most from stronger inflows, with gold and platinum group metal prices having surged to record highs.

Much stronger rand

South Africa’s rand had one of its best years on record in 2025, driven by a weaker US dollar and a commodity rally.

Positively, this strength has continued into 2026, with the rand currently holding strong at below R16/USD.

The currency has also become less volatile over the past year, with Reserve Bank Governor Lesetja Kganyago previously describing this as the currency having entered a more “mature” stage of life.

A stronger rand has improved South Africa’s terms of trade and given the Reserve Bank room to cut the country’s interest rates.

Lower interest rates

The Reserve Bank continued its cutting cycle in 2025, delivering 100 basis points worth of cuts. This brought cumulative cuts in the current cycle to 150 basis points.

It also brought the repo rate down to 6.75%, the lowest it has been since 2022, bringing meaningful relief to South Africans with debt.

The cutting cycle is expected to continue in 2026, with around 75 basis points of cuts projected.

Deficit narrows

Roodt also pointed to South Africa’s lower deficit as a reason to make him cautiously optimistic about the country’s trajectory.

South Africa’s consolidated budget deficit is expected to narrow from 4.5% of GDP in 2025/26 to 3.1% of GDP in 2028/29.

In addition, the Treasury is on track to achieve its third consecutive primary budget surplus, i.e. excluding debt servicing costs, for the 2025/26 fiscal year.

Roodt attributed the lower deficit to the Treasury’s better-than-expected revenue.

Lower debt service costs

South Africa’s primary budget surplus is what has allowed it to stabilise its debt in the 2025/26 fiscal year, which also translates into lower debt service costs.

While still the highest expenditure item in the national Budget, debt service costs are expected to stabilise and then fall over the next three years.

This is considered a major win for the state and taxpayers, as South Africa currently spends around R1.2 billion a day to service the state’s debt.

Since 2008/09, debt-service costs have risen from 8.8% of revenue to 21.3% in 2025/26, crowding out other spending.

“It has taken a large-scale consolidation effort to rein in debt for the benefit of all South Africans,” Godongwana said.

Reducing these costs will free up funds for more productive line items in the Budget, such as education and healthcare.

Removed from the greylist

Roodt also highlighted South Africa’s removal from the Financial Action Task Force’s (FATF) so-called ‘greylist’ in October 2025.

Originally placed on the list for weaknesses in its anti-money laundering and terrorism financing procedures, South Africa has now implemented all of the required reforms the FATF suggested.

South Africa’s removal from the list will go a long way in boosting investor confidence in the country and making it easier for local companies to do business with foreign companies, easing cross-border transactions.

Credit rating upgrade

Around the same time that South Africa was removed from the greylist, the country also received its first credit rating upgrade in over a decade.

Rating agency S&P Global upgraded South Africa’s rating from BB- to BB. While still in so-called “junk status” territory, this was seen as a move in the right direction.

Roodt believes more rating upgrades could follow in the coming months, with Moody’s and Fitch still rating the country at Ba2 and BB-, respectively.

New inflation target

Lastly, Roodt explained that South Africa’s lower inflation target will have a far-reaching positive impact on the country.

South Africa’s lower target not only reduces the risk associated with investing in South Africa, attracting foreign capital, but also results in lower debt-servicing costs for the state and individuals.

The Reserve Bank has long been a proponent of a lower inflation target, saying it could bring immense benefits to the economy, including lower inflation and interest rates over the long term.

Comments